Fiscal anxiety has pushed yields far but fundamentals still point to a 2.0% yield for the 10Y bond in Japan.

There has been a lot of concern around Japan’s bond market, centred around the impact of Prime Minister Sanae Takaichi’s fiscal package. These concerns overlook some of the fundamental shifts in the Japanese economy that will allow the government to sustain greater spending.

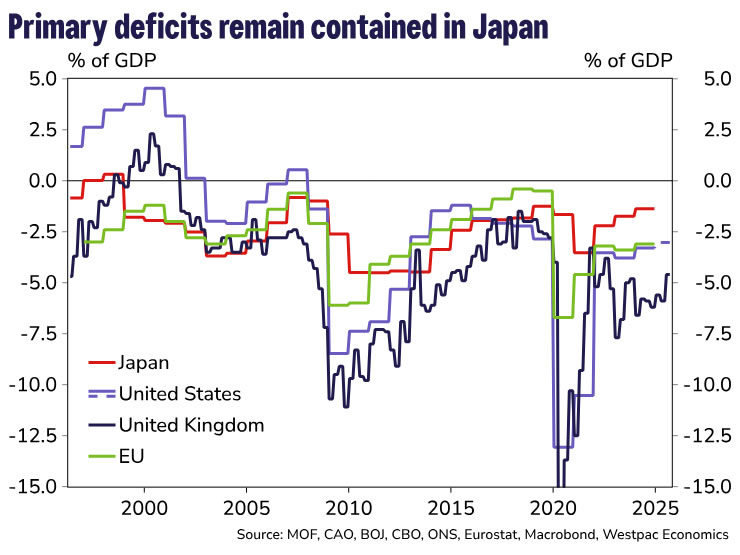

To start, it is worth putting the JPY17.1tril package (~10% of GDP) into context. Japan’s primary deficit as a percentage of its GDP of 1.4% is far lower than that of its peers like the US of around 3%. Japan has also made more progress reducing its debt-to-GDP ratio since the pandemic than other major economies and in contrast to the US where, despite a strongly growing economy, this ratio has increased. Compared to its peers, Japan has managed its fiscal position well. With inflation sustaining a 2.0%+ pace, nominal debt will also now be deflated for the first time in decades.

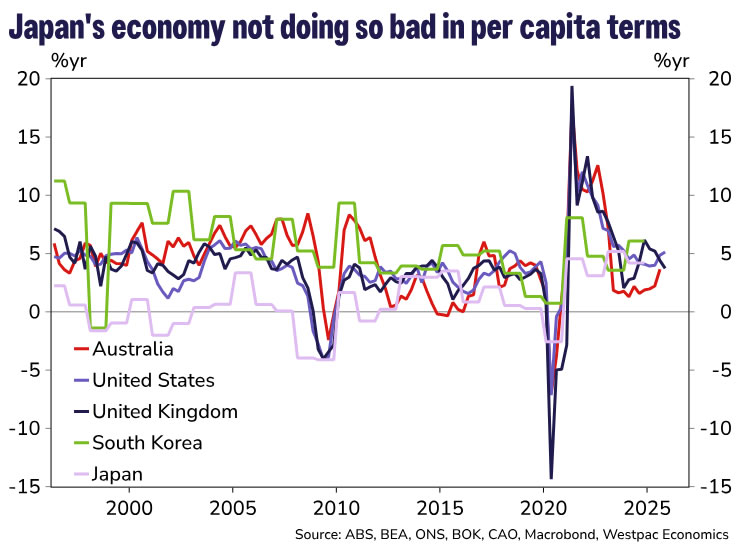

Some may point to Japan’s 1.0% real GDP growth as evidence that it cannot grow out of debt, but this overlooks the drag from a declining population. Adjusting for demographics, per‑capita GDP grew by 4.2% in 2024, broadly in line with the US, UK, South Korea and Australia. With government spending largely tied to population growth rather than headline GDP, modest aggregate growth need not imply deteriorating fiscal dynamics. While population ageing will place upward pressure on social spending, this is likely to be partly offset by arising participation.

Crucially, debt dynamics also benefit from low interest costs. Interest payments remain around 1.0% of GDP, while nominal GDP growth – what matters for debt sustainability – has averaged around 4.0% over the past two years. In this environment, debt‑to‑GDP can stabilise even with modest fiscal deficits, provided per‑capita growth remains robust.

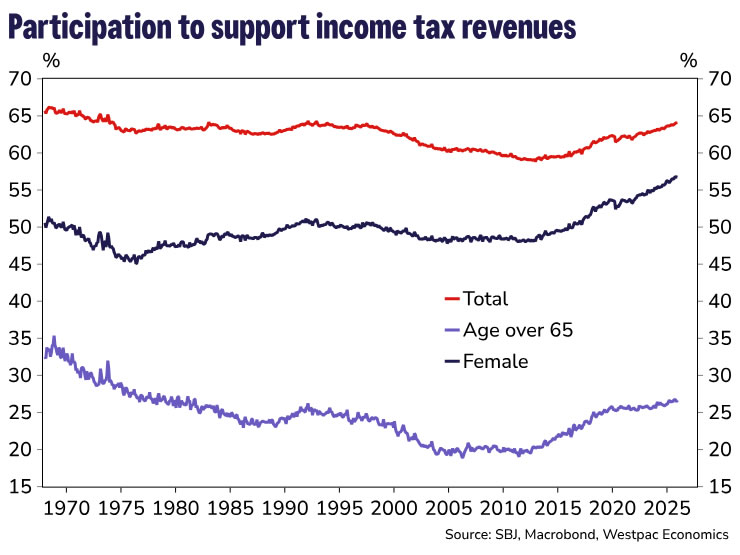

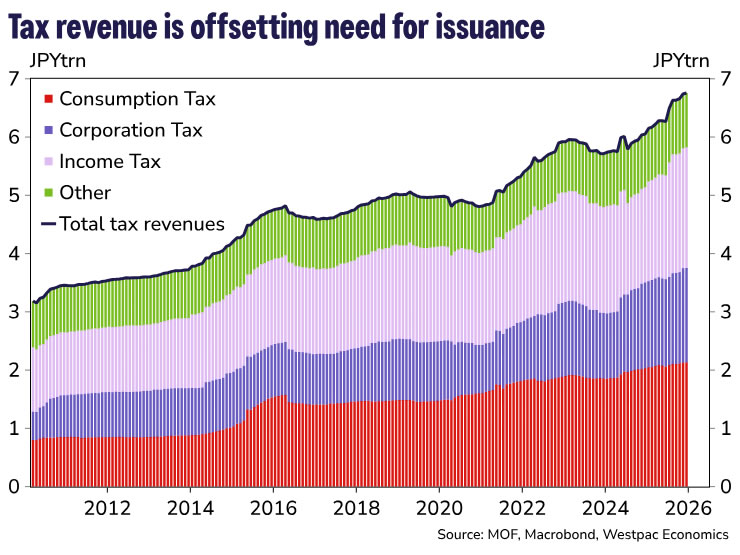

There is also upside for revenue going forward. The labour market is tight as ever, with labour force participation hitting 64.1%, the highest since December 1992, supported by an increase in participation of women and seniors—female labour force participation is at a record high of 56.7%. As we have previously discussed, this trend is unlikely dissipate with Japan’s population continuing to age and shrink. A larger labour force alongside greater nominal wage increases should help support income tax revenues.

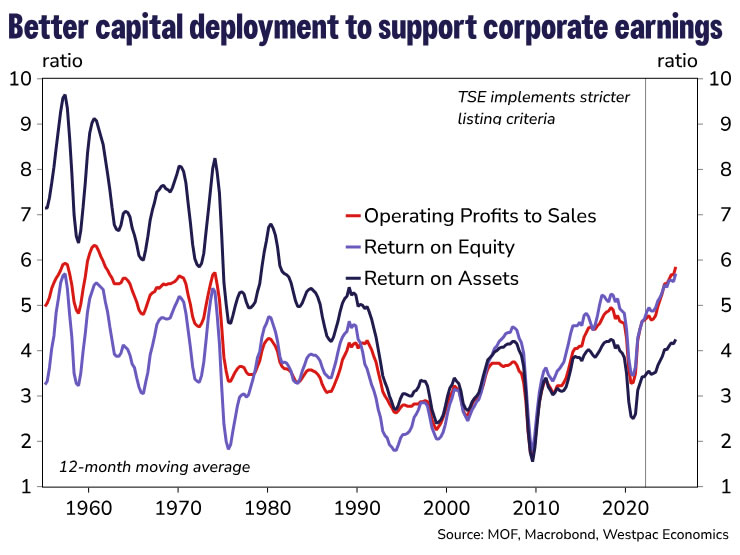

Also assisting revenue growth, will be the impact corporate governance reforms have had on profitability. Over the last three years, the Tokyo Stock Exchange requirements have forced firms to unwind their cross-shareholdings and improve capital efficiency which has seen the return on equity climb to an average of 5.5 in the year to September 2025, compared to an average of 3.4 over 1990–2019 and 4.0 over 1960–90. Combined with a shift in price-setting behaviour and strong export earnings, corporate profits have reached levels unseen since before the Lost Decades. The benefits of these corporate reforms are likely to support profitability and hence corporate tax revenue going ahead.

While external risks are significant, particularly China’s competitive position in autos and semiconductor manufacturing, these reforms will also help enhance adaptability. Firms are now allocating capital to research and development versus maintaining inefficient conglomerates.

Alongside serviceability concerns, investors have expressed concerns around excess supply of Japanese Government Bonds (JGBs) as the Bank of Japan slows its purchases of bonds. However, these concerns are overstated. For one, the BoJ has been vocal about reducing its holdings in a way that “avoid[s] inducing destabilizing effects on the financial markets”. This isn’t just rhetoric. The BoJ tapered its pace of purchases in July 2025 from JPY400bn to JPY200bn and have, on numerous occasions, affirmed that “In the case of a rapid rise in long-term interest rates, it will make nimble responses by, for example, increasing the amount of JGB purchases…”. Note as well, their current purchase pace is not insignificant at around JPYs2.9tril a month (which annualises to around JPY36tril a year) against the Ministry of Finance’s (MoF) planned JPY190tril of issuance through FY2025 (ending in March 2026). The MoF also has flexibility on the duration of issuance, offering another way to contain market volatility and an unwanted tightening of financial conditions.

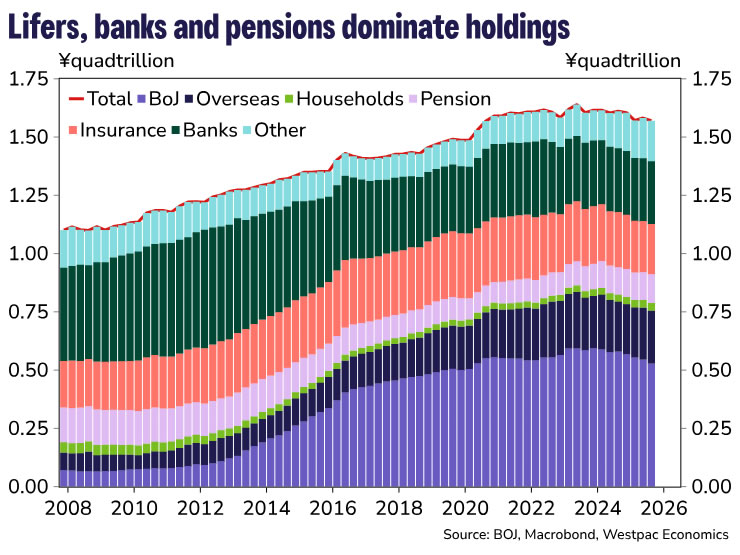

Interest cost concerns also miss the mark for another reason. Interest costs as a share of GDP remain low in Japan compared to peers and, given the BoJ owns around half of outstanding JGBs, almost half of the Government’s initial interest outlay flows back to the government, making them fiscally neutral. The pace of the BoJ’s balance sheet normalisation will be gradual and only as market conditions warrant, and so this interest cost offset is set to remain in place for the foreseeable future.

The portion of the bond market not held by the BoJ is mostly held by domestic investors, with foreign ownership sitting at 14%, compared to 23% in the US and 31% in the UK. This insulates against risks of foreign capital flight in times of uncertainty making comparisons between Takaichi and Truss unjust. Domestic players tend to hold JGBs to match liabilities, particularly important for Japan’s large life insurance sector, and regulatory requirements. The MoF has proven nimble in its flexibility to match issuance tenors to demand to accommodate preferences. In the near term, our Strategy team continues to expect that Japan is unlikely to export as much capital to offshore bonds and will continue to purchase JGBs. Further information on this will come in April as the investment intentions of Japan’s mega life insurers are made public.

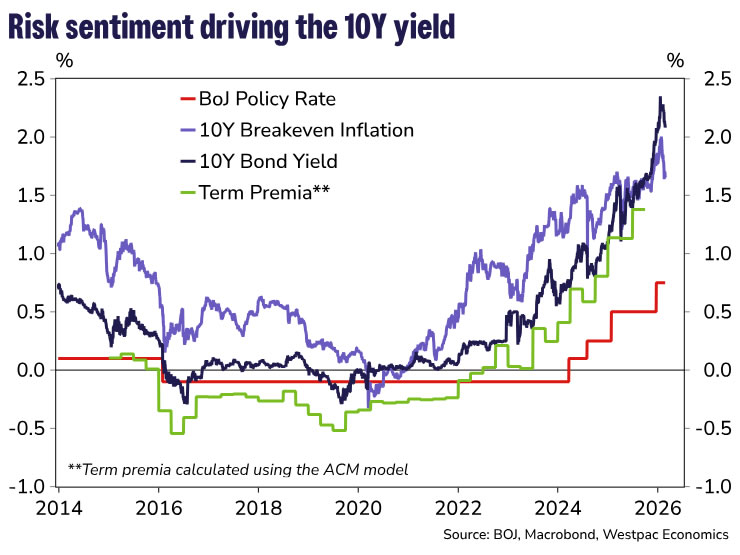

Given these factors, we anticipate the premium markets are pricing into JGBs will fade with time returning the 10-year government bond yield to 2.0%, roughly 100bps above the terminal policy rate. This is still at the high end of global cash to 10-year curve spreads, but not deleteriously so. We see this adjustment unfolding over the next year, as markets continue to focus on supply dynamics and political noise even as Japan’s underlying fiscal and macro fundamentals remain supportive.

{kind=link}