Dollar is being hit from both sides—soft inflation and warmer diplomacy. A cooler-than-expected PPI reading has eased pressure on the Federal Reserve to turn more hawkish, while renewed optimism around US-Iran negotiations is unwinding the war premium that briefly supported the greenback. Together, these forces are driving an extended, broad-based Dollar selloff in early US session.

The PPI data delivered a key relief signal for markets. Headline producer prices rose just 0.5% mom, well below expectations. But the most important detail came from services, which printed at 0.0% mom. This suggests that the inflation pipeline is not as clogged as feared, with businesses absorbing higher input costs rather than passing them on to consumers.

That dynamic is critical for Fed policy expectations. With margins compressing instead of prices rising across services, the data reinforces the view that underlying inflation pressures remain contained despite the energy shock. This gives the FOMC room to remain patient rather than reactive, validating recent messaging that more data is needed before committing to further tightening.

As a result, the “higher and still rising” rate narrative has been firmly pushed off the table for now. Instead, markets are anchoring expectations around a “higher for longer” stance, with reduced urgency for additional hikes. This repricing has weighed on US yields and removed a key pillar of Dollar support.

At the same time, geopolitics are moving in a more constructive direction. Markets are pricing progress again—not escalation—as signals emerge that US-Iran talks could resume as soon as this week. The breakdown in Islamabad is increasingly being viewed as a pause rather than a failure.

Reports that both sides were “80% there” before hitting a deadlock have given traders a tangible reason to expect a second round of negotiations. The remaining gap, largely centered on nuclear commitments, is seen as political and potentially bridgeable within the current ceasefire window.

European diplomacy is also stepping up. French President Emmanuel Macron confirmed that France and the UK will host a conference in Paris aimed at restoring freedom of navigation. The initiative seeks to bring in “non-belligerent countries”, raising the diplomatic cost of further escalation.

This combination of factors is driving a rapid unwind of the war premium. Oil has retreated rather than extending its rally, equities are holding firmer, and safe-haven demand for Dollar is fading. The earlier risk-off move is now being reversed as markets reposition for a continuation of diplomacy.

In the currency markets, Dollar remains the worst performer for the day, followed by Euro, and then Loonie. Kiwi is currently the strongest, followed by Aussie and then Sterling. Yen and Swiss Franc are trading in the middle of the pack.

In Europe, at the time of writing, FTSE is up 0.13%. DAX is up 1.19%. CAC is up 0.76%. UK 10-year yield is down -0.054 at 4.763. Germany 10-year yield is down -0.038 at 3.060. Earlier in Asia, Nikkei rose 2.43%. Hong Kong HSI rose 0.82%. China Shanghai SSE rose 0.95%. Singapore Strait Times rose 0.47%. Japan 10-year JGB yield fell -0.054 at 2.420.

Silver Rallies, Outperforming Gold, as Supply Shock Risk Builds on Sulphur Shortage and China Export Ban

Silver is outperforming gold as markets begin to price a potential supply squeeze driven by sulphur shortages and China’s export ban. With a key input under pressure and supply tightening from multiple fronts, the rally is shifting from a Dollar-driven move to a structural story. Read more.

US PPI Inflation Rises 0.5% as Led by 16.7% Surge in Gasoline Prices, But Misses Expectations

US producer price inflation picked up in March, led by a sharp jump in gasoline prices, but the broader picture remains contained. With core pressures steady and services inflation flat, the data suggests energy is driving the move rather than a broad inflation surge. Read more.

RBA’s Hauser Warns of ‘Central Banker’s Nightmare’ as Oil Shock Lifts Inflation, Hits Growth

RBA Deputy Governor Andrew Hauser warns that rising oil prices are delivering a “central banker’s nightmare,” with inflation climbing as growth risks build. With a potential income shock looming and policy uncertainty rising, the RBA faces a difficult balancing act. Read more.

Australian Consumer Sentiment Plunges as Fuel Prices Surge, RBA Still Set to Hike

Australian consumer sentiment has dropped sharply to near crisis levels as fuel prices and rate hikes hit households. But with inflation still elevated, Westpac expects the RBA to raise rates again in May and continue tightening later this year, highlighting the growing tension between weaker demand and persistent price pressures. Read more.

Australian NAB Business Confidence Plunges to -29 as Middle East Shock Hits

Australian business confidence has collapsed to GFC- and COVID-era levels as Middle East tensions hit sentiment, but activity is still holding for now. With cost pressures surging and price growth accelerating, the data highlights a growing tension between weakening outlook and rising inflation risks. Read more.

China Trade Signals Diverge as Weak Exports Meet Import Boom

China’s trade data showed a sharp split in March, with exports slowing to a five-month low while imports surged on commodity demand. Read more.

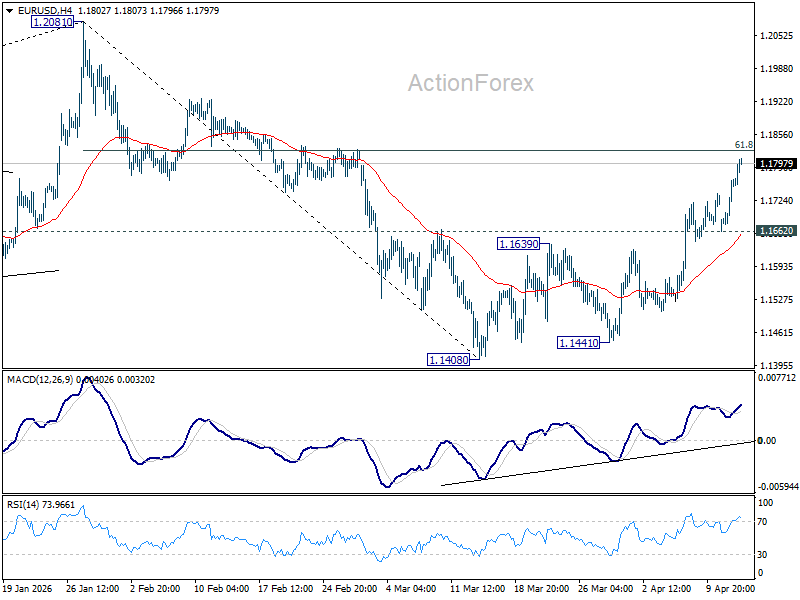

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1694; (P) 1.1729; (R1) 1.1795; More….

Intraday bias in EUR/USD remains on the upside for 61.8% retracement of 1.2081 to 1.1408 at 1.1824. Decisive break there will extend the rally from 1.1408 to retest 1.2081 high. For now, further rally will remain in favor as long as 1.1662 support holds, in case of retreat.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1513). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}