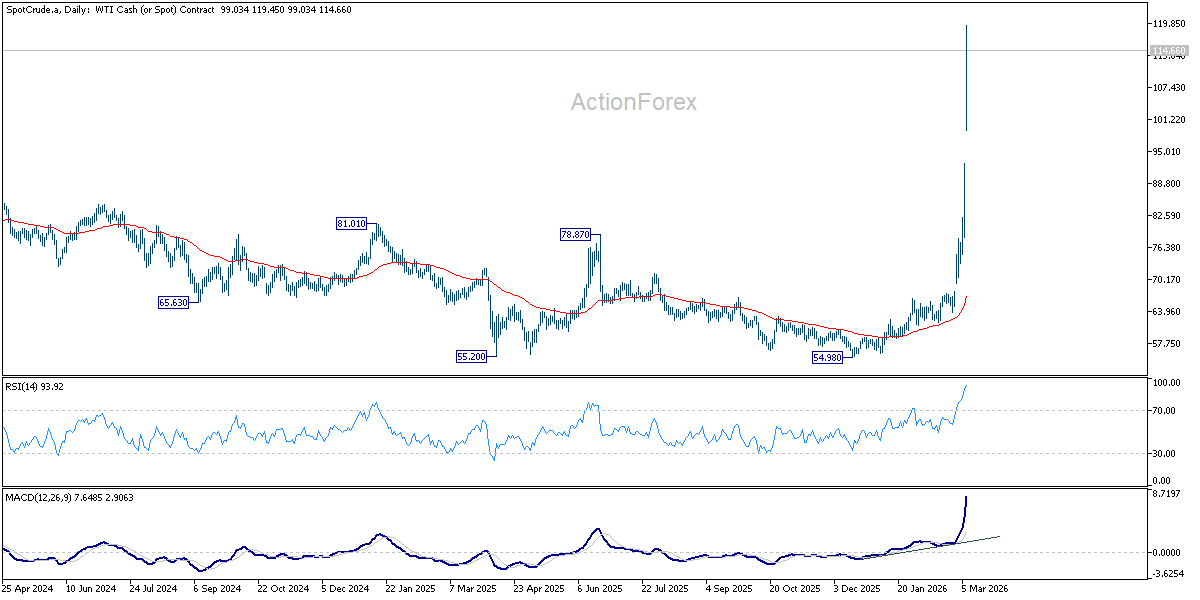

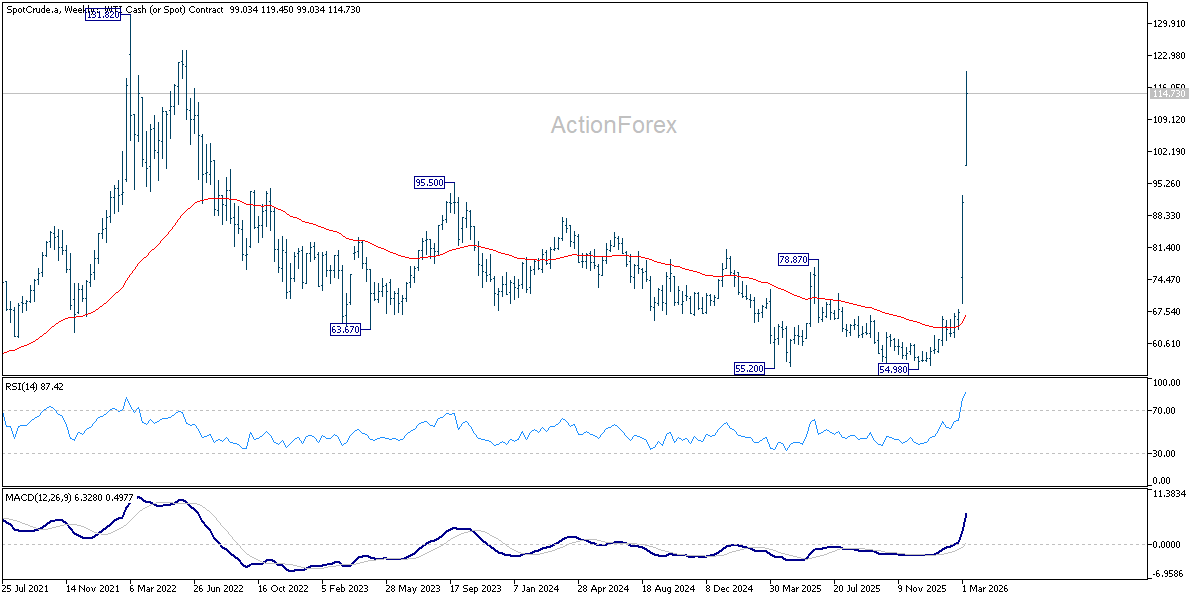

WTI crude oil surged above 110 mark at the start of the week, extending an explosive rally that has already lifted prices roughly 50% since the Middle East conflict began on February 28. The latest move followed a violent gap-up at the weekly open, highlighting how quickly markets are adjusting to the possibility that the crisis may evolve into a sustained disruption to global energy supply or even production.

Over the weekend, political developments effectively removed the remaining “diplomatic discount” that had been embedded in oil prices. Markets had previously assumed that negotiations, strategic reserves, or external intervention could eventually stabilize the situation. Those assumptions now appear increasingly fragile.

One key development was Iran’s leadership transition. The official appointment of Mojtaba Khamenei as Supreme Leader following the death of Ali Khamenei is widely interpreted as signaling a harder political stance in Tehran. Markets view the transition as reducing the probability of rapid diplomatic compromise.

At the same time, the US has sent a strong policy signal. President Donald Trump’s recent remarks that higher oil prices are “a very small price to pay” for defeating Iran suggest that Washington is unlikely to prioritize price stabilization through measures such as a Strategic Petroleum Reserve release. Combined with demands for “unconditional surrender,” the comments have removed much of the market’s expectation of near-term de-escalation.

With WTI already above 110, the key question for markets is no longer whether the rally will continue, but how far it could extend if the crisis intensifies. The outlook could be framed in three possible scenarios: 130, 150, and 200 oil.

The 130 Level: The “Geopolitical Spike”

The first scenario centers around the 130 level. This price zone represents what could be described as a “geopolitical spike,” driven primarily by fear and logistical disruption rather than a complete physical shortage of crude supply.

The Strait of Hormuz normally carries roughly 21 million barrels per day, or about 20% of global oil consumption. Currently, around 150 oil tankers are reportedly waiting outside the Strait as shipowners assess security conditions. If this “tanker parking lot” persists for several more days, markets may begin treating the disruption as a sustained supply bottleneck.

Such a scenario could push oil toward the 130 level, similar to the price spikes seen during the early phase of the Russia–Ukraine war in 2022. At that stage, prices would largely reflect risk premiums and logistical friction rather than outright shortages.

The 150 level: The “Force Majeure” Threshold

A second and more severe scenario would involve oil approaching 150. Qatar’s Energy Minister Saad Sherida Al-Kaabi last week warned that both Brent and WTI could reach 150 per barrel within two to three weeks if the situation fails to stabilize.

The significance of the 150 level lies in the potential for a “force majeure” chain reaction. If exporters are unable to move crude through Hormuz, producers could begin legally suspending supply contracts. That would likely trigger panic buying by import-dependent economies.

Meanwhile, the 100% blockage of this route for more than two weeks mathematically could forces price to 150 to “choke off” enough global demand to match the remaining supply.

The 200 Level: The “Structural Damage” Scenario

The most extreme outcome would see oil moving toward 200 mark. This scenario would require a fundamental escalation of the conflict, including direct attacks on major energy infrastructure in the Gulf region.

Facilities such as Saudi Arabia’s Abqaiq processing plant, the UAE’s Upper Zakum field, and Kuwait’s Al-Zour refinery represent critical pillars of the global energy system. If these assets were damaged, the market would no longer be pricing temporary disruption but long-term structural damage to oil supply.

Unlike shipping disruptions, damaged energy infrastructure can take years to restore. In such a scenario, prices approaching 200 would reflect the market pricing in a multi-year global supply deficit rather than a short-term geopolitical shock.

{kind=link}