Today’s calendar is packed with major data releases including GDP and inflation from Eurozone and the US, ECB and BoE rate decision, and escalating geopolitical risks all converging. But markets are not struggling to find direction. Oil is doing that job. Brent crude has surged above the key $120 psychological level, hitting a four-year high, forcing markets to reprice inflation, policy expectations, and currencies simultaneously.

The trigger is a clear escalation in rhetoric and positioning. Reports that U.S. Central Command will brief President Donald Trump on potential military action against Iran have rattled markets. Additionally, the messaging from Washington has turned more aggressive. Trump’s public statements, including a stark “No More Mr. Nice Guy” stance, are being interpreted by markets as a shift from “maximum pressure” to “active deterrence.” This raises the risk that current tensions could evolve into a more direct confrontation.

Traders are now moving away from a “resolution” mindset and toward a “prolonged standoff” scenario, with risk of re-escalation in conflicts. The break above $120 is more than a technical move. It signals that markets are beginning to price in further prolonged supply disruption. If tensions escalate further, this level could quickly become the new baseline rather than the peak.

This oil surge is feeding directly into inflation expectations and, by extension, central bank policy outlooks. That is particularly relevant today as both the Bank of England and the European Central Bank are set to announce rate decisions.

For the Bank of England, a hold at 3.75% remains the overwhelming consensus. However, the focus will be on the vote split and forward guidance. After a unanimous hold in March, there is now a possibility of hawkish dissent in favor of a rate hike, especially as policymakers assess the risk of second-round effects from rising energy prices on wages and services inflation.

Governor Andrew Bailey’s commentary will be closely watched, particularly for any indication that the BoE sees the oil shock as more persistent. If policymakers signal concern about inflation becoming embedded, market expectations for further tightening could firm quickly.

At the European Central Bank, a hold at the 2.00% deposit rate is also almost certain. However, the meeting carries significant forward guidance risk. Markets are currently pricing in two 25bps hikes for the remainder of 2026, with June seen as the “live” meeting for the first move.

The key question is whether President Christine Lagarde will signal that timeline more explicitly. Any hint toward a June hike would effectively validate market pricing and could push European yields higher, reinforcing the broader tightening narrative.

At the same time, a heavy data calendar looms. U.S. GDP and PCE inflation, alongside Eurozone GDP and CPI, would normally drive markets. But today, their role is secondary. Instead, they will be filtered through the oil narrative. Strong inflation data will reinforce the current trajectory, while weaker growth may be overlooked unless it becomes severe enough to challenge the tightening bias.

In currency markets, Dollar is the strongest performer so far this week, supported by safe-haven demand and a subtle shift in Fed expectations following the latest decision. With three policymakers opposing even an easing bias, markets are now pricing less than a 5% chance of a rate cut by year-end.

Canadian Dollar is the second strongest, benefiting from the surge in oil prices. Australian Dollar also remains firm, as higher energy costs reinforce expectations that the RBA will proceed with a rate hike in May and more thereafter.

At the other end of the spectrum, Swiss Franc is the weakest performer. The widening interest rate gap is weighing heavily, as other central banks lean toward tightening while the SNB is expected to remain on hold.

Yen remains under pressure despite the risk environment. USD/JPY has surged beyond the 160 intervention red line, but Japanese authorities are unlikely to act decisively in the current volatile environment. Instead, the currency is continuing to reflect the impact of higher global yields and energy costs.

With so many moving parts, markets are navigating a complex maze. But the hierarchy is clear—oil and geopolitics are setting the direction, while central banks and data are being forced to react.

In Asia, at the time of writing, Nikkei is down -1.32%. Hong Kong HSI is down -1.20%. China Shanghai SSE is up 0.16%. Singapore Strait Times is up 0.61%. Japan 10-year JGB yield is up 0.058 at 2.523. Overnight, DOW fell -0.57%. S&P 500 fell -0.04%. NASDAQ rose 0.04%. 10-year yield rose 0.06 to 4.42.

Gold Hit by Double Whammy, Heading Back Toward 4,000

Oil and yields are squeezing Gold from both sides. With downside momentum building, the 4,000 level is coming back into view. Read More.

Japan Industrial Output Falls -0.5% as Petrochemical Weakness Dominates

Japan’s factory output is slipping as energy-linked sectors are hit by supply disruptions, even as retail sales rebound and consumption holds up. Read More.

NZ ANZ Business Confidence Slumps to -10.6, Inflation Expectations Highest Since Feb 2024

Cost pressures are surging in New Zealand, driving inflation expectations higher and pushing business confidence back into negative territory. Read More.

China PMI Signals Modest Growth as Services Slip and Cost Pressures Build

China’s PMI data shows resilient output but growing divergence and rising inflation pressures within the economy. Read More.

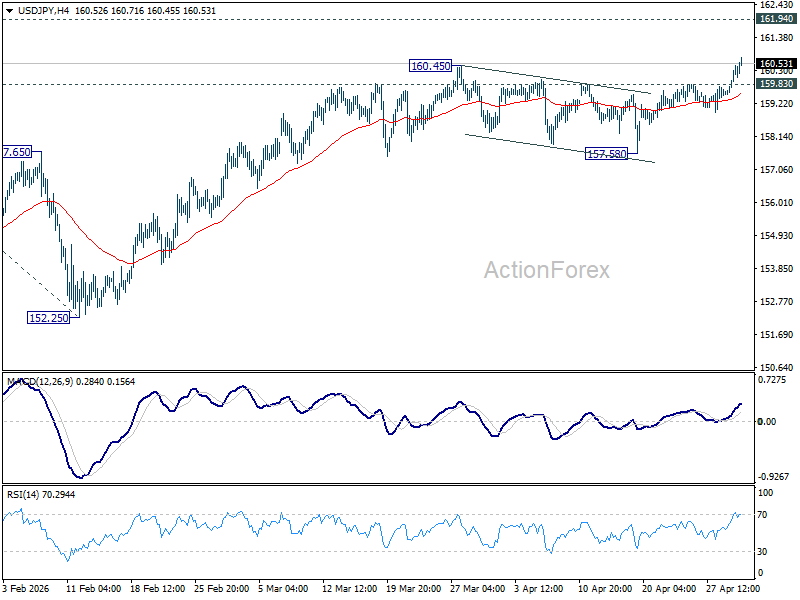

USD/JPY Daily Outlook

Daily Pivots: (S1) 159.79; (P) 160.14; (R1) 160.79; More…

USD/JPY’s break of 160.45 resistance confirms resumption of rally from 152.25. Intraday bias is on the upside for retesting 161.94 high. Decisive break there will target 61.8% projection of 139.87 to 159.44 from 152.25 at 164.34 next. On the downside, below 159.83 minor support will turn intraday bias neutral first. But downside of retreat should be contained well above 157.58 support to bring another rally.

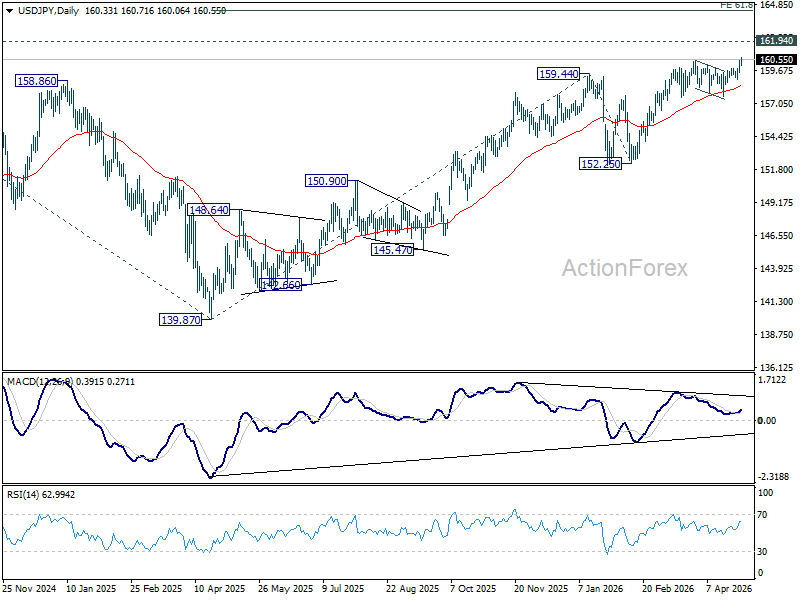

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.81) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

{kind=link}