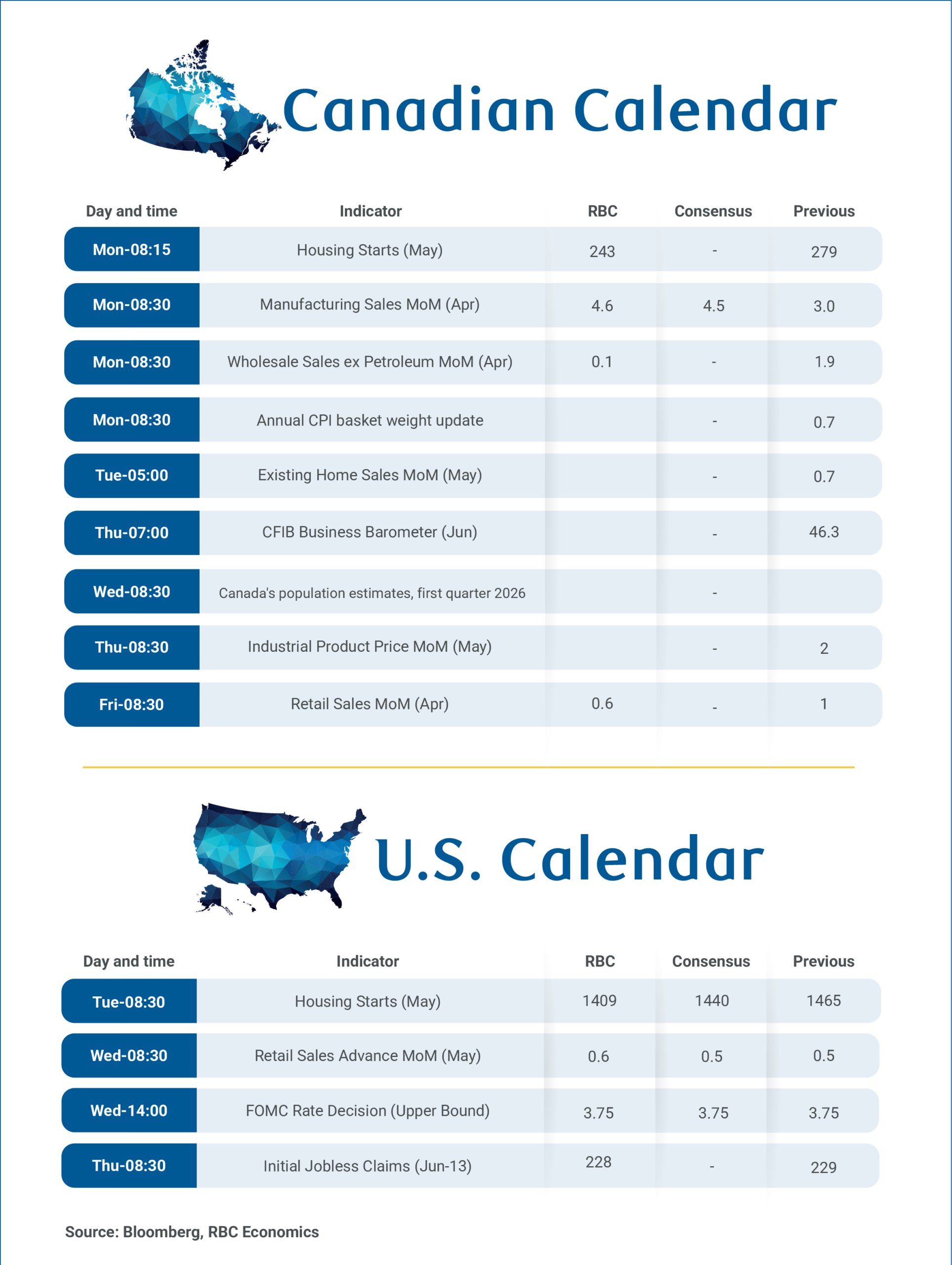

April’s manufacturing and wholesale reports on Monday and retail sales on Friday should support the Bank of Canada’s (and our) outlook of Canada’s growth resuming in Q2 after Q1’s contraction.

Statistics Canada’s advanced estimate is a 4.6% rise in manufacturing sales, and a 0.6% increase in retail sales. Part of these reflect higher petroleum prices. But, manufacturing sales volume would still be up nearly 3% after accounting for that, and there’s little evidence so far that high gasoline prices are crowding out retail spending in other areas.

Wholesale sales (excluding petroleum) likely held onto strength in April after a larger 1.9% nominal increase (1.7% real) in March. Home resales in May should also point to further stabilization in housing markets with some of the least affordable and most depressed larger cities (like Toronto) showing green shoots in early reports.

Overall, data should be broadly consistent with the preliminary estimate that real Canadian gross domestic product rose 0.4% in April. However, these advance monthly production estimates have been highly volatile, prone to revisions, and are less reliable than usual as a gauge for quarterly GDP growth.

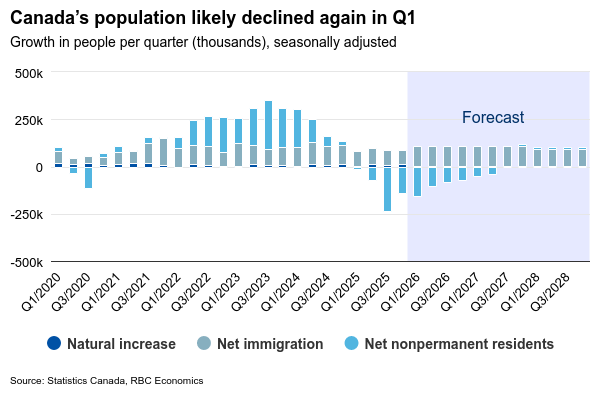

Importantly, headline GDP and employment data also remain heavily influenced by large population swings. Quarterly demographics’ estimates on Wednesday are expected to show a third consecutive decline in population in Q1 due to a rapidly shrinking pool of non-permanent residents. That should leave recent softer GDP numbers still looking better on a per-capita basis.

Warsh’s Fed moving further away from rate cuts

Between Canada and the U.S., we highlighted diverging macro trends with a stronger U.S. economy requiring the U.S. Federal Reserve to keep interest rates at higher levels than in Canada.

Our base case forecast, however, remains that the BoC and Fed will stay on the sidelines this year. We expect the FOMC to hold the Fed Funds rate steady on Wednesday, but move further away from a cutting bias towards a more neutral stance given the recent run of data.

U.S. labour market reports have consecutively surprised to the upside, alleviating concerns over the employment of the Fed’s dual mandate. In the meantime, headline U.S. inflation has risen on the back of surging gasoline prices and sticky core inflation. Attention next week will also be on the new Fed Governor Kevin Warsh, who will preside over his first FOMC meeting after taking office in May.

U.S. retail sales likely rose in May, but details will be closely watched for signs whether higher spending on gasoline from higher prices is beginning to squeeze spending on other products. U.S. consumer spending has remained resilient so far, but through a drawdown in savings that isn’t sustainable. Still, vehicle sales rose in May and we look for control sales (excluding gasoline, auto purchases, and building material store sales) to edge up 0.3%.

outlook of Canada’s growth resuming in Q2 after Q1’s contraction.){kind=link}