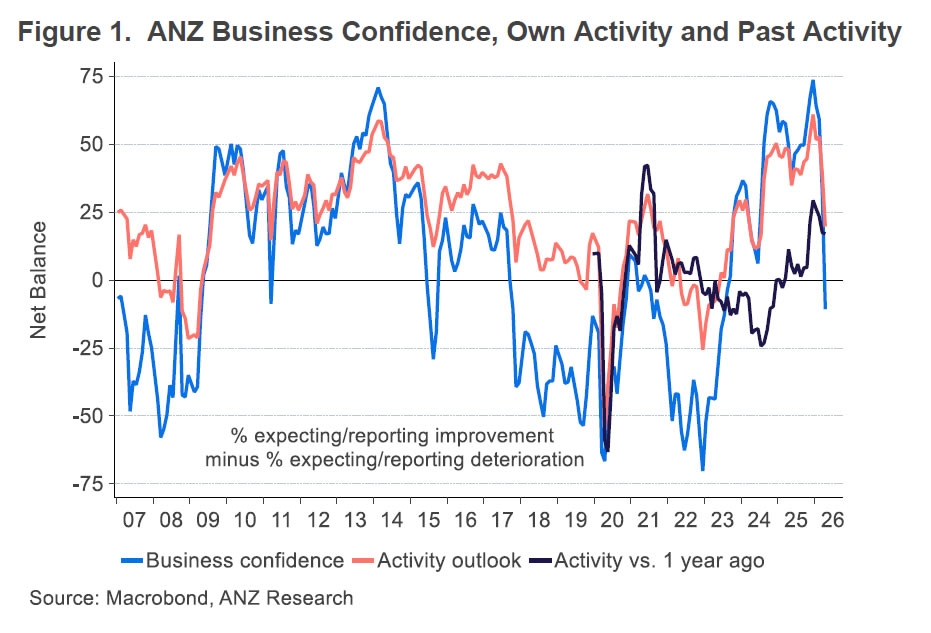

New Zealand business confidence deteriorated sharply in April, with ANZ’s headline index plunging from 32.5 to -10.6, highlighting a rapid shift in sentiment amid rising cost pressures. Firms’ own activity outlook also fell significantly from 39.3 to 19.6. One-year ahead expectations, meanwhile, jumped from 3.08% to 3.81%, the highest since February 2024.

Cost pressures have intensified again. Cost expectations rose from 84.7 to 90.4 in net terms, reaching the highest level since January 2023. On a three-month horizon, cost expectations surged from 2.99% to 4.57%, the highest since May 2023. This reflects a renewed wave of input cost pressure hitting firms, reinforcing the inflation impulse from external shocks.

Pricing behavior is firm but not accelerating as sharply. Pricing intentions edged down from 60.3 to 57.7, led by strong retail pricing at 78, while services at 51 dragged the overall measure lower. Short-term pricing expectations rose slightly from 2.37% to 2.41%, with manufacturing firms showing stronger pass-through at 3.4% compared to just 2.0% in services. This divergence suggests uneven ability to pass costs on.

Importantly, the underlying picture is not uniformly negative. ANZ noted that many activity indicators improved relative to late responses in the prior month, indicating that some of the initial confidence shock has eased. For the RBNZ, the challenge is clear: rising cost pressures and inflation expectations increase the risk of persistence, even as pricing and wage behavior remain relatively contained for now.

| Indicator | March | April | Change |

|---|---|---|---|

| ANZ Business Confidence | 32.5 | -10.6 | ↓ Sharp drop |

| Own Activity Outlook | 39.3 | 19.6 | ↓ Significant decline |

| Inflation Expectations (1yr) | 3.08% | 3.81% | ↑ Highest since Feb 2024 |

{kind=link}