- We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 19 March in line with consensus and market pricing. All focus is on signals.

- Lagarde to communicate a full commitment to price stability and readiness to act to upward price pressures but at the same acknowledge highted uncertainty and that it is too early to draw firm conclusions.

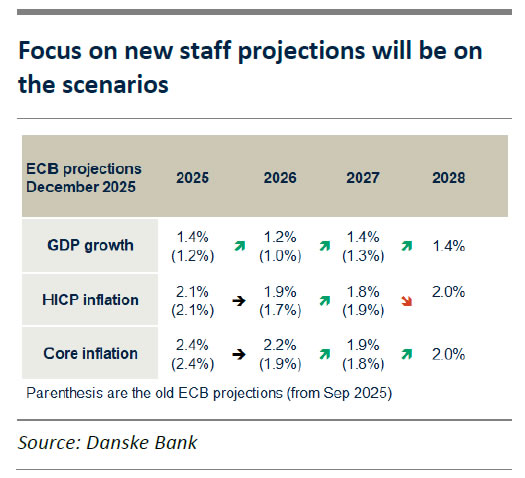

- The baseline staff projections will not incorporate higher commodity prices so attention will be on the scenarios, where we expect the ECB to communicate upside inflation risks and downside growth risks.

- Our baseline is unchanged ECB rates in 2026 and 2027 but with upside risk.

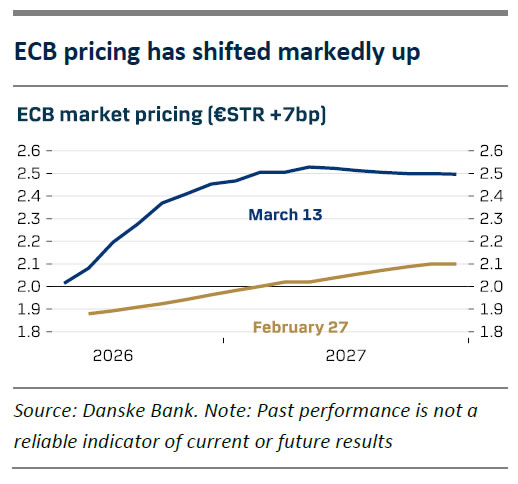

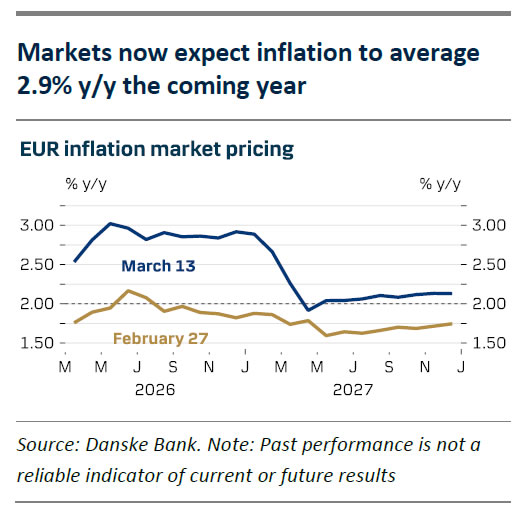

We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 19 March in line with market pricing and consensus. The ECB is faced with a drastically changed economic outlook due to the war in Iran. Inflation expectations have risen sharply with markets now expecting inflation to average 2.9% y/y for the rest of the year. This has led to significant repricing of the ECB with a total of 45bp worth of hikes priced in by YE 2026 with the first full 25bp hike in September. The communication from Governing Council members the past week has shown a divergence in views. ECB’s Kazimir gave a string of hawkish comments noting that “a reaction by the ECB is potentially closer than many people think” and Schnabel called for “vigilance”. “Vigilance” was in the period from 2005 to 2011 a synonym for a hawkish stance that led to a subsequent policy rate hike. More dovish members have signalled a wait and see approach with Guindos saying, “we need to keep a cool head and not overreact,” and Cipollone “it’s far too early to have a full assessment”. We expect Lagarde to strike a balance between the camps by stating that ECB is fully commitment to price stability and ready to act to upward price pressures, but at the same acknowledge highted uncertainty and that it is too early to draw firm conclusions.

The meeting will include a new set of staff projections. Because the cut-off date for the technical assumptions on energy prices was prior to the war in Iran, the baseline scenario will not fully reflect the rise in energy prices and is therefore of smaller interest. Attention will instead focus on the published alternative scenarios that incorporate higher commodity price assumptions. The upside energy price scenario will provide important insight into how the ECB staff views higher energy prices’ impact on the euro area economy, thereby offering a signal for the rate path. We pay special attention to mentioning of medium-term inflation risks since market-based measures have risen above 2% (1y1y inflation at 2.20%, 2y2y at 2.13%, and 5y5y at 2.20%). If Lagarde explicitly mentions that risks to medium-term inflation have shifted upwards, we would interpret this as a clear hawkish signal.

In December 2023 ECB staff modelled a similar Middle East war scenario with a partial closure of the Strait of Hormuz and a lift of the oil price to USD 130/bbl and natural gas at EUR 83/Mwh. This led to 0.85pp higher euro area HICP inflation in the first year and 0.6pp lower GDP growth compared to the baseline. We therefore expect ECB to highlight that the risk assessment on inflation is tilted to the upside while the growth risks are tilted to the downside.

Our baseline is unchanged ECB rates but with a clear upside risk

In our base case we expect the rising energy prices to have a temporary effect on the price level, but we expect only small changes to medium-term inflation due to limited pass-through to core. We note that in the past six months the ECB has been focused on core inflation amid headline being projected below 2% in 2026/27. As the 2025 strategy review also acknowledged, the flexibility in the medium-term inflation target should allow larger short-term deviations due to more frequent supply shocks. We therefore expect the ECB to “look through” the Iran shock as growth is also negatively affected, and subsequently we do not expect the ECB to raise policy rates in 2026 nor 2027. However, the scars from the latest inflation crisis have likely lowered the threshold for when the ECB will act to upward price pressures even though the textbook reaction would be to “look through” the shock. Central banks tend to fight their last wars (too hawkish ahead of GFC in 2008, too dovish ahead of 2022 inflation crisis). Combined with energy prices and risks of second round effects, this constitutes an upside risk to our ECB call even though the economic situation is significantly different compared to 2021/2022.

{kind=link}