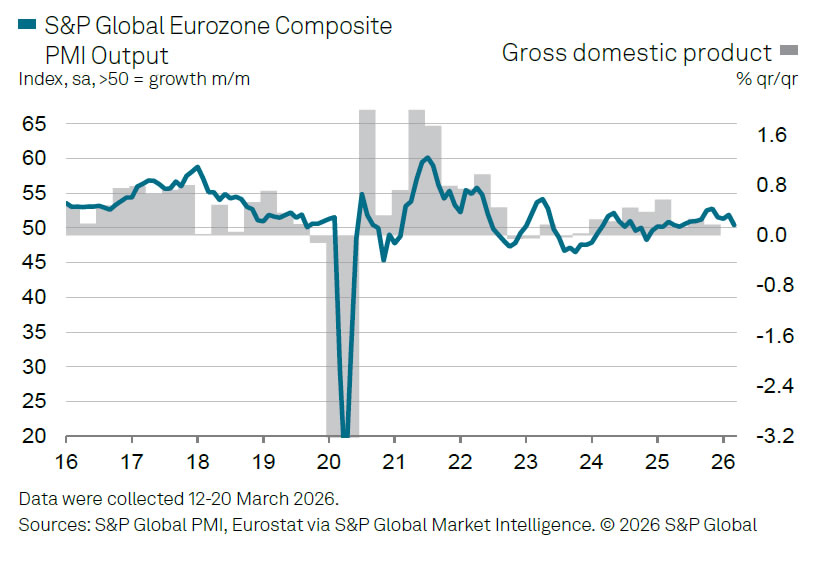

Eurozone PMI data for March point to growing stagflation risk, with rising cost pressures colliding with slowing growth. PMI Manufacturing rose from 50.8 to 51.4, marking a 45-month high. But this strength was offset by weakness in services, where PMI Services fell from 51.9 to 50.1. As a result, PMI Composite declined from 51.9 to 50.5, its lowest level in 10 months.

The divergence highlights an uneven economic picture. While manufacturing continues to benefit from pockets of external demand, the services sector is losing momentum as business confidence deteriorates and new orders weaken. According to S&P Global’s Chris Williamson, output growth has slowed to “near-stagnation”, with forward-looking indicators pointing to a heightened risk of a downturn in the coming months.

At the same time, inflation pressures are intensifying sharply. Firms reported the fastest rise in input costs in over three years, driven by higher energy prices and worsening supply chain disruptions linked to the Middle East conflict. Supplier delays have surged to their highest since mid-2022.

The data present a difficult backdrop for the EB. With growth slowing toward stagnation while price pressures accelerate, policymakers face a challenging trade-off. Williamson noted that the ECB is no longer in a “good place” on the growth-inflation balance, with survey indicators pointing to inflation nearing 3% and GDP growth slipping below 0.1% in the near term.

{kind=link}