Markets are staying in a cautious holding pattern as investors awaited the highly anticipated Trump-Xi summit later this week, increasingly viewing the Beijing meeting as the decisive geopolitical checkpoint for both the Strait of Hormuz crisis and broader global trade relations. While financial markets remained relatively calm overall, underlying positioning continued reflecting elevated uncertainty around oil prices, inflation, technology supply chains, and geopolitical stability.

US equities closed mixed overnight, with NASDAQ retreating modestly after its recent record-setting rally. Asian markets traded mildly firmer led by gains in Japan and South Korea. Brent crude eased slightly but remained elevated above $106, signaling that geopolitical risk premium remains firmly embedded in energy markets even as traders avoid aggressive breakout positioning ahead of the summit. Gold continued fluctuating in a relatively tight range around the 4700 area, reinforcing the broader sense that markets are waiting for clearer direction from upcoming political developments.

In currency markets, Dollar remained the strongest major currency for the week so far, though without strong follow-through momentum. The greenback continued receiving support from rising oil prices and firmer US inflation data, which further reduced expectations for Federal Reserve rate cuts this year. Aussie is the second-strongest performer as resilient global risk appetite and AI-related optimism continued supporting commodity and semiconductor-linked assets. Loonie benefited from the rebound in crude prices.

By contrast, Yen is the weakest major currency as the impact of Japan’s recent intervention efforts faded. Sterling was the second weakest amid continuing concerns over political instability in the UK following mounting pressure on Prime Minister Keir Starmer after Labour’s poor local election performance. Swiss Franc also underperformed as rising global bond yields reduced demand for defensive assets. Euro and Kiwi traded closer to the middle of the major currency rankings.

The May 14–15 Trump-Xi summit in Beijing is viewed as far more than a standard diplomatic meeting. After Pakistan’s failed attempt to mediate between Washington and Tehran, markets see China as the only major power with enough economic leverage over Iran to help reopen the Strait of Hormuz. As the world’s largest buyer of Iranian oil and a likely cornerstone of Iran’s future reconstruction financing, Beijing is widely perceived as holding significant influence over Tehran’s strategic calculations.

That perception has effectively transformed the summit into the “Final Court of Appeal” for the Hormuz crisis. While discussions are expected to include tariffs, rare earth access, AI export controls, and broader trade relations, the energy and geopolitical dimension is likely to dominate market attention.

US President Donald Trump continued projecting a hardline posture ahead of the meeting. Speaking before departing for Beijing, Trump said he did not believe the United States needed China’s help to resolve the Iran conflict and reiterated that preventing Iran from obtaining nuclear weapons remained his only objective. “We’ll win it one way or the other, peacefully or otherwise,” he said, while also dismissing concerns about economic pain linked to the conflict. Markets, however, appear focused on whether the summit can ultimately produce enough diplomatic progress to prevent a longer and more economically damaging Hormuz crisis.

Meanwhile, the United States is reportedly seeking guaranteed access to Chinese-controlled critical minerals including rare earths, gallium, and germanium, while China remains eager for greater access to advanced US AI chips and semiconductor technology. The inclusion of Nvidia and Apple executives in summit-related discussions has intensified speculation that a broader “grand bargain” may be under consideration.

Washington could potentially ease certain technology export restrictions in exchange for stronger Chinese cooperation on Iran and regional energy stability. Such a framework could also involve expanded Chinese purchases of US agricultural, energy, and aerospace products under a new managed-trade arrangement.

In Asia, at the time of writing, Nikkei is up 0.79%. Hong Kong HSI is down -0.07%. China Shanghai SSE is up 0.45%. Singapore Strait Times is up 1.01%. Japan 10-year JGB yield is up 0.039 at 2.583. Overnight, DOW rose 0.11%. S&P 500 fell -0.16%. NASDAQ fell -0.71%. 10-year yield rose 0.05 to 4.46.

OECD Sees BoJ Raising Rates to 2% by End-2027

The OECD believes Japan’s monetary normalization cycle is still in its early stages, projecting the BOJ’s policy rate will rise from 0.75% to 2% by the end of 2027. Strong wage growth, resilient domestic demand, and improving inflation dynamics are increasingly supporting the case for continued tightening. Read More.

New Zealand Inflation Expectations Jump as RBNZ OCR Outlook Turns Hawkish

The RBNZ’s latest Survey of Expectations showed inflation concerns intensifying sharply in New Zealand, with one-year CPI expectations surging above 3.4% while markets also lifted their outlook for future OCR settings. At the same time, growth expectations weakened noticeably, highlighting a more difficult balancing act for policymakers. Read More.

Fed’s Goolsbee: Inflation Is Moving the Wrong Way, Labor Market Is Not

Chicago Fed President Austan Goolsbee warned that inflation is “going the wrong way,” expressing particular concern that services inflation remains too strong even beyond the direct impact of oil prices. Read More.

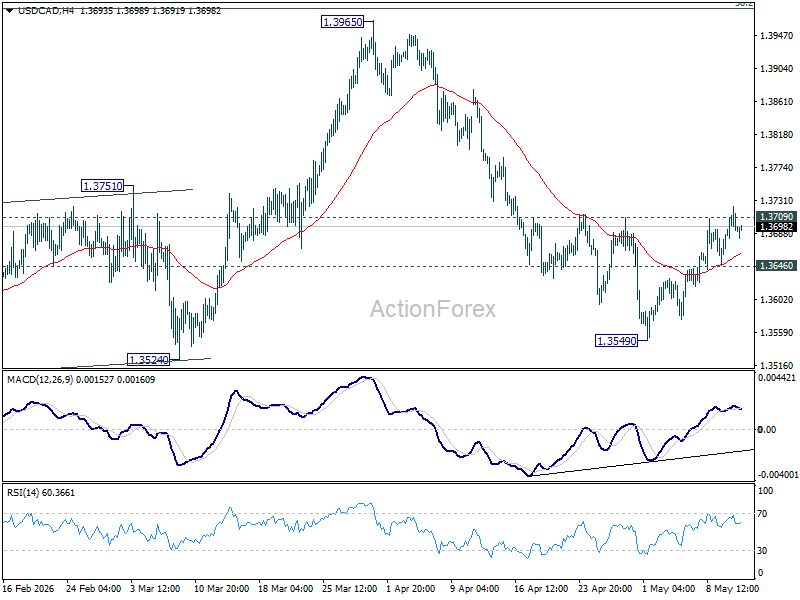

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3667; (P) 1.3695; (R1) 1.3722; More…

USD/CAD’s breach of 1.3709 resistance indicates short term bottoming at 1.3549, on bullish convergence condition in 4H MACD. Rise from there is seen as the third leg of the corrective pattern from 1.3480. Intraday bias is mildly on the upside for further rise towards 1.3965 resistance. On the downside, though, break of 1.3646 minor support will bring retest of 1.3549 instead.

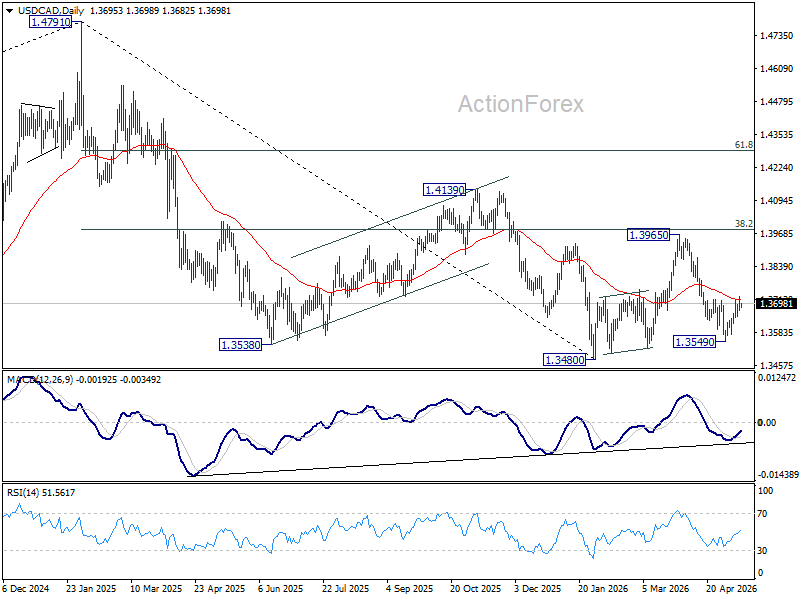

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already.

{kind=link}