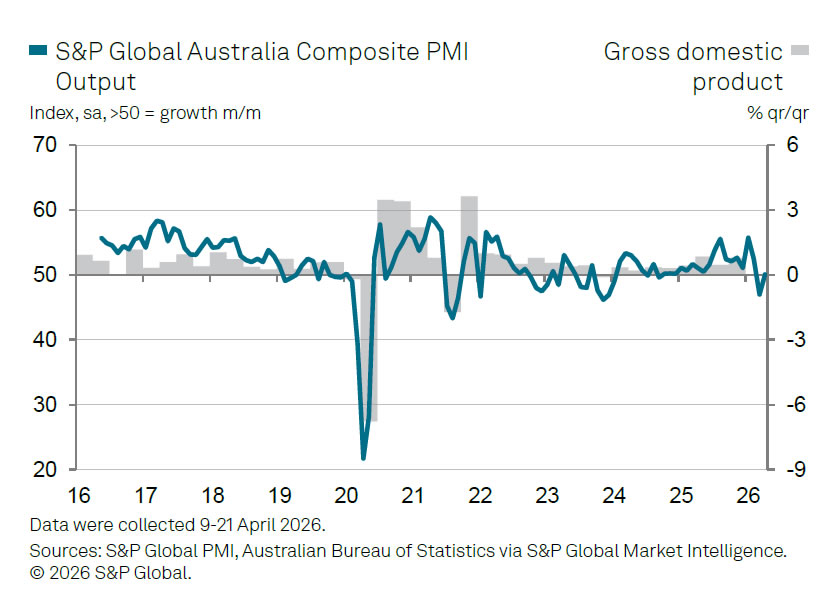

Australia’s private sector returned to modest growth in April, with the S&P Global Flash Composite PMI rising from 46.6 to 50.1, just crossing back above the expansion threshold. The improvement was driven by a sharp rebound in services, where PMI jumped from 46.3 to 50.3, signaling stabilization after March’s contraction.

However, the recovery remains uneven. Manufacturing PMI rose from 49.8 to 51.0, back into expansion territory, but output within the sector fell further from 49.4 to 48.2. This divergence suggests that while sentiment and headline activity improved, actual production conditions remain under pressure, reflecting ongoing disruptions in supply chains.

Cost pressures are intensifying. Input price inflation accelerated for a third consecutive month, reaching its highest level since August 2022, driven largely by higher fuel and shipping costs linked to the Middle East conflict. Businesses are passing on part of these increases, with output prices rising at the fastest pace in three-and-a-half years.

Overall, the data points to a fragile recovery. Services are providing near-term support, but manufacturing remains constrained, and inflation pressures are building again.

| Indicator | Apr 2026 | Mar 2026 |

|---|---|---|

| PMI Composite | 50.1 | 46.6 |

| PMI Services | 50.3 | 46.3 |

| PMI Manufacturing | 51.0 | 49.8 |

| Manufacturing Output | 48.2 | 49.4 |

| Input Cost Inflation | ↑ | ↑ |

| Output Price Inflation | ↑ | ↑ |

| Supply Chain Lead Times | Lengthened | — |

| Demand / Confidence | Soft | Soft |

{kind=link}