- We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 30 April in line with consensus and market pricing. All focus is on signals.

- We expect Lagarde to leave the door open for summer hikes in order to keep inflation expectations anchored, but at the same time not pre-commit to hikes.

- We expect the ECB to increase policy rates by 25bp in June and July.

We expect the ECB to leave the deposit rate unchanged at 2.00% on Thursday 30 April in line with consensus and market pricing. Recent communication from the ECB’s GC members has indicated that they are in no rush to increase policy rates. Lagarde has stated that the “ECB needs more data before drawing policy conclusions” and Schnabel has said that “the ECB can afford to take time to analyse Iran shock”. With significant uncertainty around the economic outlook, we believe the option value of “wait and see” at the April meeting is high compared to hiking.

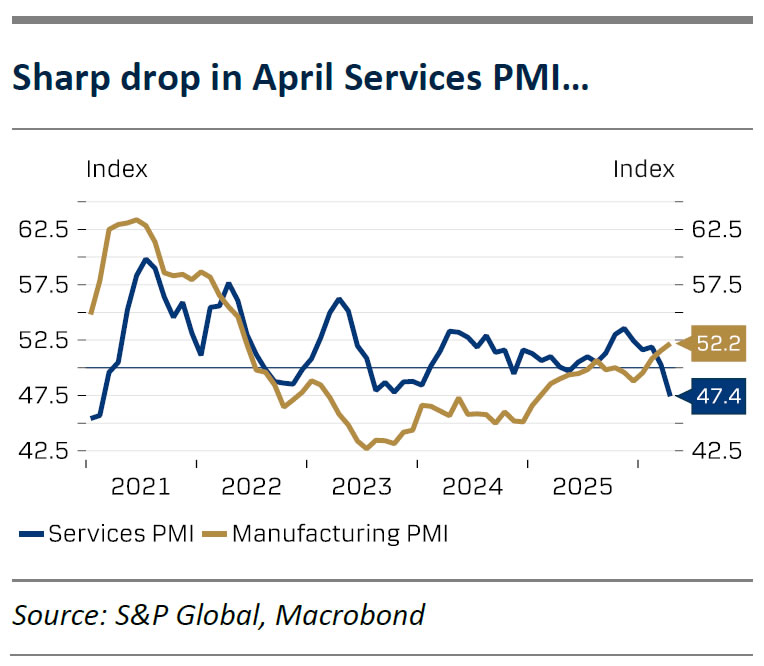

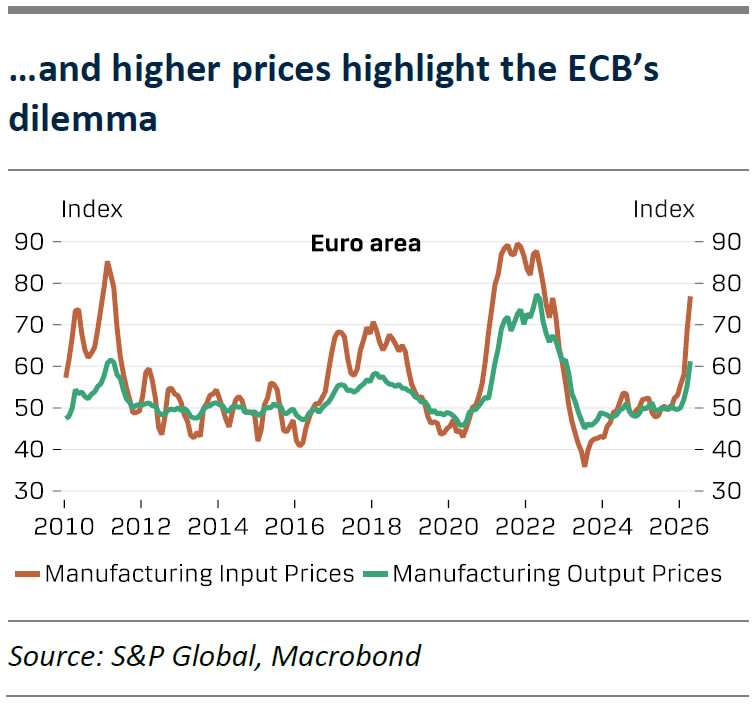

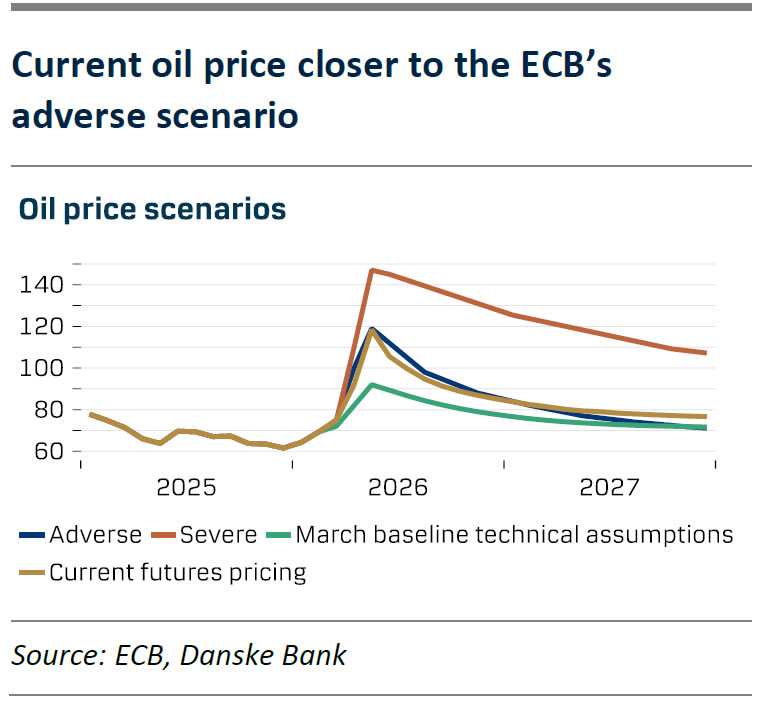

Since the March meeting, headline inflation increased as expected while the PMI data was weaker than expected, but with a sharp rise in price components (charts 1 and 2). Oil contracts for April and May are close to the ECB’s ‘adverse’ scenario while futures have fluctuated and are now close to the adverse scenario (chart 3). The inflation outlook is thus closer to the ‘adverse’ scenario which supports our view of two hikes, as around 35bp worth of hikes was included in the projections’ technical assumptions. The ECB’s communication is still relatively hawkish, and they signal that curbing upside price pressures carries more weight than mitigating deteriorating growth prospects. Moreover, we anticipate rate increases to ensure inflation expectations remain anchored. We therefore expect the ECB to raise policy rates by 25bp at the June and July meetings, bringing the deposit rate to 2.50%.

With an unchanged decision in April all focus during the meeting will be on signals, and we expect Lagarde to leave the door open for summer hikes in order to keep inflation expectations anchored. The ECB is likely broadly satisfied with the current market pricing of 65bp worth of hikes this year. Although we do see room for market pricing falling slightly as most recent communication from the ECB’s GC members has increasingly mentioned deteriorating growth prospects from higher energy prices. For this reason and given the extraordinary uncertainty about the economic outlook we do not expect any pre-commitments to summer hikes. Lagarde will likely state that the ECB remains data-dependent and will look at incoming data on a meeting-by-meeting basis before making decisions. At the same time, we expect her to communicate a full commitment to price stability and say that the ECB is ready to act if data warrants it. On the strategy side, we favour playing the move for lower short-end swap rates highlighting the negative growth effects from the negative supply shock. While timing is tricky, we monitor the 2Y1Y ESTR swap for re-entry after taking 9bp profit last Friday, as we still like the strategic nature of the trade.

{kind=link}