- We expect the Bank of England on hold on 30 April. We pencil in no rate changes for the coming 12 months but with risks tilted towards hikes.

- Data has come in mostly on the hawkish side since March as the economy has weathered the energy blow better than expected. Like consumer sentiment, it could still turn sour, though.

After the BoE’s hawkish turn in March, investors quickly started to price in near-term hikes but from mid-March to mid-April much was priced out again not least because Governor Bailey has been quite clear that the BoE is in no rush. During the recent week, pricing has taken another turn on the back of deteriorating energy markets and macro data coming in mostly on the hawkish side.

Starting with the soft data, April consumer sentiment declined for a third consecutive month, suggesting solid retail sales growth in March is probably not fully reflecting consumers reaction to the energy shock. The salary index in the KPMG and REC report on jobs ticked lower in March and the freshest part of the official labour market report also showed 11K jobs were lost in March while February was revised lower pointing to lower payrolls after the recent release had shown signs of improving.

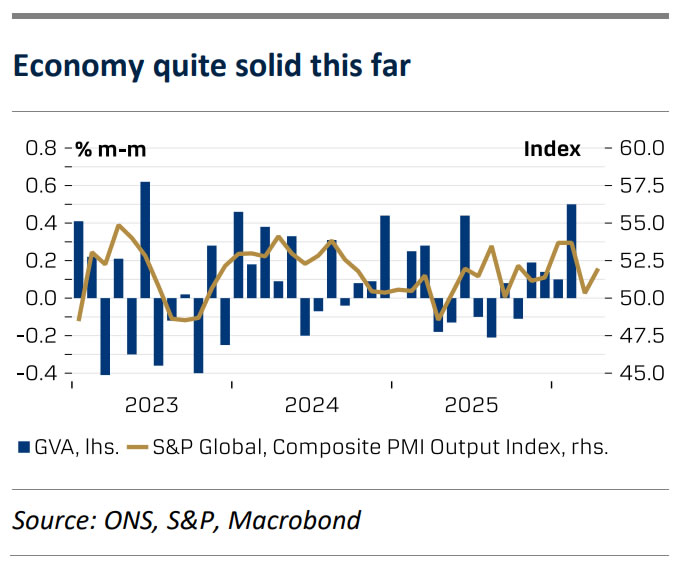

On the other hand, the more outdated part of the report shows that a worrying increase in unemployment has reversed with a 0.3 percentage point decline in February to 4.9% and the trend for lower wage growth not as strong as expected. Furthermore, the UK headed into the energy crunch with surprisingly strong momentum, as the service sector drove 0.5% mom GDP growth in February. April PMIs suggest the economy has remained afloat with the service sector even accelerating leaving composite PMI at a solid 52, much stronger than expected. Price indexes increased a lot, mostly for input prices but also the output price index has crossed 62 levels its highest since early 2023. Core inflation edged lower in March slightly below expectations, but service inflation rebounded to 4.5%, clearly too high.

BoE call. Even if recent data has come in quite solid, the UK labour market is much cooler and the starting point for the Bank Rate at 3.75% is much higher compared to 2022. Hiking rates will have to be weighed against a considerable risk of exacerbating a looming economic contraction. We think it is most likely the BoE will remain sidelined for the foreseeable future.

Market reaction. With the hawkish repricing in mind, we see risks slightly tilted towards a more dovish stance, supportive for EUR/GBP. We think the BoE is most likely to refrain from pushing back too much on market pricing, though. We forecast EUR/GBP to move higher towards 0.89 on a 6-12-month horizon.

{kind=link}