The Fed maintained its policy stance unchanged, as widely expected. Stephen Miran dissented in favour of a rate cut, while three participants dissented against maintaining an easing bias. Powell announced he continues as a Fed Governor past his term as Chair but did not specify for how long.

Powell flagged that growing number of participants are seeing current stance as neutral but did not suggest rate hikes were in the cards for now. Neither the statement nor Powell discussed the Fed’s balance sheet operations.

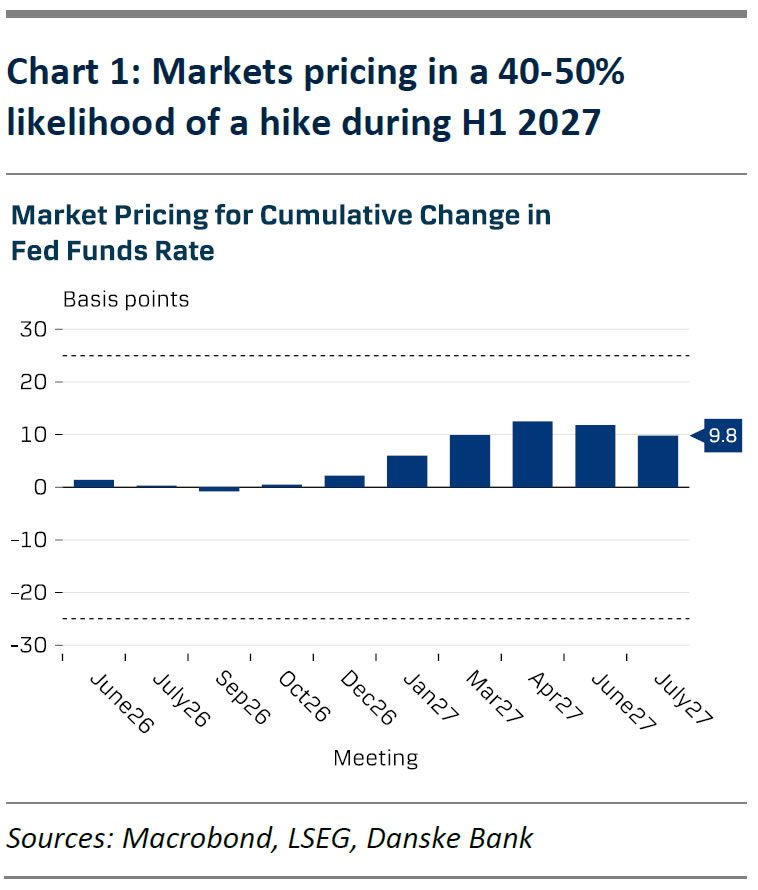

UST yields moved higher, with markets erasing earlier bets for rate cuts this year and instead pricing in around 50% probability of a hike in H1 2027. We maintain our relatively dovish call, and still expect two cuts in Sep and Dec.

Jay Powell’s final press conference as the Fed chair was as much about guidance during a difficult time for policy setting, as it was about his personal choice. Powell continues as a Fed Governor also after his term as the Chair ends 15 May, though he intentionally did not specify for how long. The decision is hawkish on the margin, as it blocks Trump from nominating a new and potentially more dovish replacement.

It also means Stephen Miran, who was the only participant voting in favour of a cut, will not continue as a Governor in June when Kevin Warsh takes his seat. Powell tied his future exit to DoJ’s criminal investigation being ‘well and truly over’, but we also flagged in RtM USD, 28 April, that staying beyond midterms could complicate Trump’s task of replacing him with a dove like Miran if Democrats manage to flip the Senate.

Three participants – Logan, Kashkari and Hammack – dissented against the Fed’s current easing bias. That said, all three have been firmly in the FOMC’s hawkish camp for a while, as they vocally opposed the latest rate cut already last fall. Powell specified that no one in the committee argued for a hike, and majority did not want to send a signal that a hike would be equally likely as a cut. On the other hand, Powell emphasized that the committee will not be even thinking about cutting for the next few months, as it waits to see both the effects of the energy supply shock and whether tariff-driven inflation begins to fade.

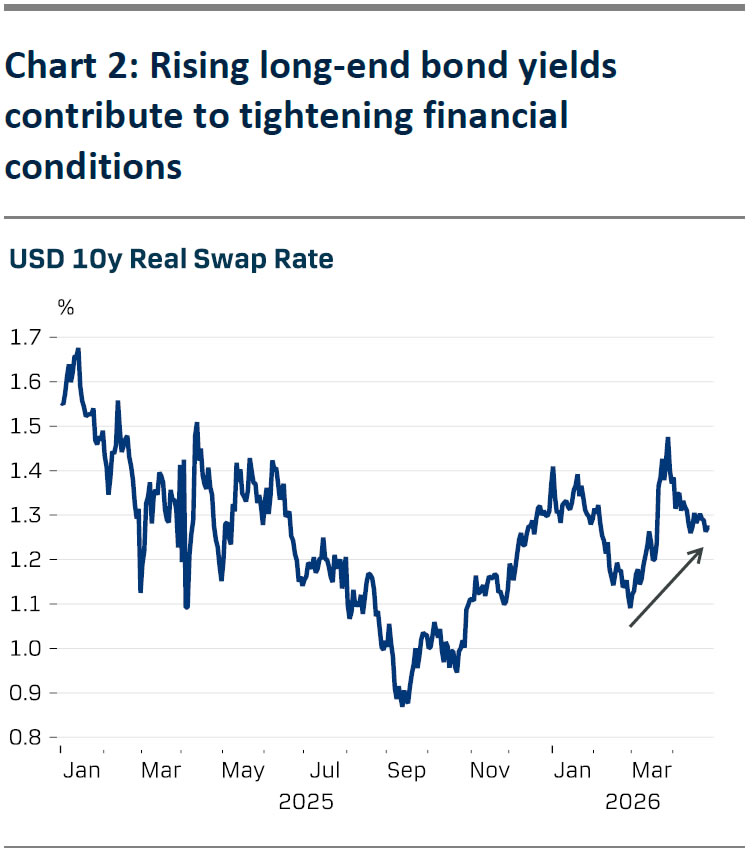

We still think the Fed will eventually resume its easing cycle with two final cuts in September and December. The war in Iran hurts the economy where we see it as already vulnerable to setbacks – in private consumption via lower disposable income, and in non-AI investments via higher interest costs. Bond yields continued to rise during the press conference, and not just because inflation expectations are following oil prices. The 10y real swap rate is even above its pre-war levels (chart 2). The bottom line is that tighter financial conditions are already weighing on the growth outlook even without explicit policy stance tightening.

Neither the statement nor Powell touched upon the Fed’s balance sheet, but we expect further guidance on the T-bill Reserve Management Purchases in the minutes. Earlier guidance suggests purchase amounts will continue to decline sharply in May.

{kind=link}