Bank of England left Bank Rate unchanged at 3.75%, in line with expectations, but the decision revealed a subtle shift in policy dynamics. The vote split moved to 8–1, with Chief Economist Huw Pill dissenting in favor of a 25bps hike. This marks a departure from the previous unanimous hold and signals that concerns about inflation persistence are beginning to surface within the Committee.

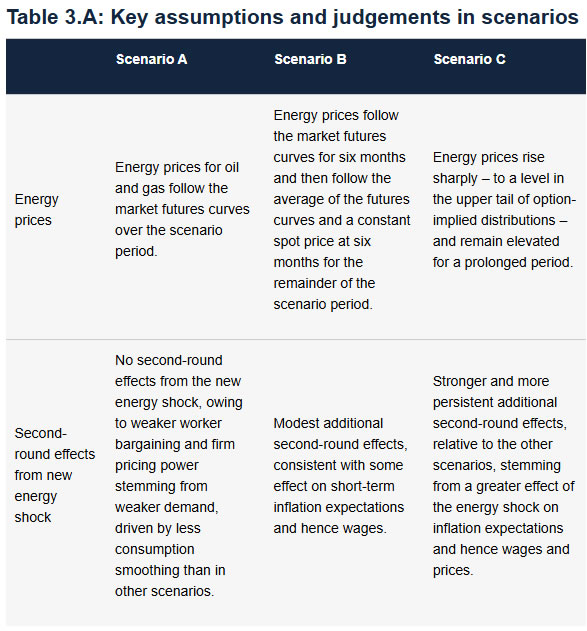

The central theme of the decision is the inflationary impact of the Middle East energy shock. The BoE acknowledged that CPI has already risen to 3.3% and is “likely to be higher later this year” as higher energy prices feed through. While monetary policy cannot directly influence energy prices, the Committee emphasized the need to ensure that the adjustment does not lead to sustained inflation above the 2% target. The risk of second-round effects in wages and pricing remains is key concern.

Pill’s dissent underscores that risk. He warned that higher energy prices could become embedded in inflation expectations, leading to more persistent price pressures. In his view, these second-round effects are “skewed to the upside,” and a “prompt but modest hike” would help mitigate the risk of inflation persistence. His stance contrasts with the majority, who see a loosening labor market and weakening growth as factors that could contain inflation over time.

The BoE’s scenario analysis highlights the uncertainty. While a benign path sees inflation returning below target, a more adverse scenario suggests CPI could rise as high as 5.6% in 2027 if second-round effects take hold. This framework makes clear that policymakers are actively considering the possibility of a more persistent inflation regime, even if it is not yet the base case.

| Summary of scenarios | 2026 Q2 | 2027 Q2 | 2028 Q2 | 2029 Q2 |

| Scenario A | ||||

| CPI inflation | 3.1 | 2.9 | 1.5 | 1.7 |

| GDP | 0.7 | 0.8 | 1.7 | 1.8 |

| Scenario B | ||||

| CPI inflation | 3.1 | 3.2 | 2 | 2 |

| GDP | 0.7 | 0.8 | 1.7 | 1.7 |

| Scenario C | ||||

| CPI inflation | 3.6 | 5.6 | 2.9 | 2.6 |

| GDP | 0.7 | 0.5 | 1.7 | 1.8 |

{kind=link}