- The ECB held policy rates unchanged as widely expected with the deposit rate at 2.00% on Thursday 30 April.

- Lagarde refrained from giving firm guidance of the future rate path and stated that the ECB will have more information in June to take a decision, including new projections and scenarios. By extension, the market reaction was highly contained.

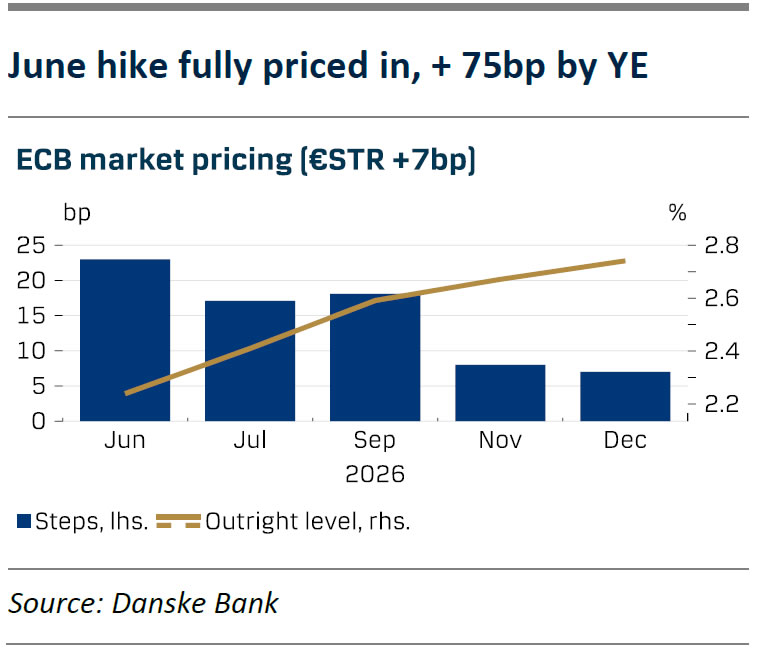

- We continue to expect the ECB to increase policy rates by 25bp in June and July, respectively.

The ECB decided to keep the three key policy rates unchanged at the April meeting as widely expected by both consensus and markets, keeping the deposit rate at 2.00%. The ECB stated that both the upside risks to inflation and downside risks to growth have intensified. Yet, the GC remains “well positioned” to navigate the uncertainty and they asses long-term inflation expectations are “well anchored”. ECB highlights that the implications of the Iran war depend on the intensity and duration, so they are not drawing firm conclusions yet but remain in “wait and see” mode.

During the press conference Lagarde refrained from giving firm guidance on the future path of interest rates. She highlighted the deteriorating growth prospects and that she was “certainly not seeing second-round effects”. Lagarde noted that it was a unanimous decision within the GC to keep rates unchanged, but they debated various options including a rate hike, which was a view held by some members of the GC. The ECB will have more information in June where their staff both updates the baseline projections and the economic scenarios. Until then, the ECB is faced with an “ocean of uncertainty”. As a consequence, the market reaction was highly contained with European rates remaining in a tight range, ending the press conference 1-2bp lower with EUR/USD breaking slightly below the 1.17 mark.

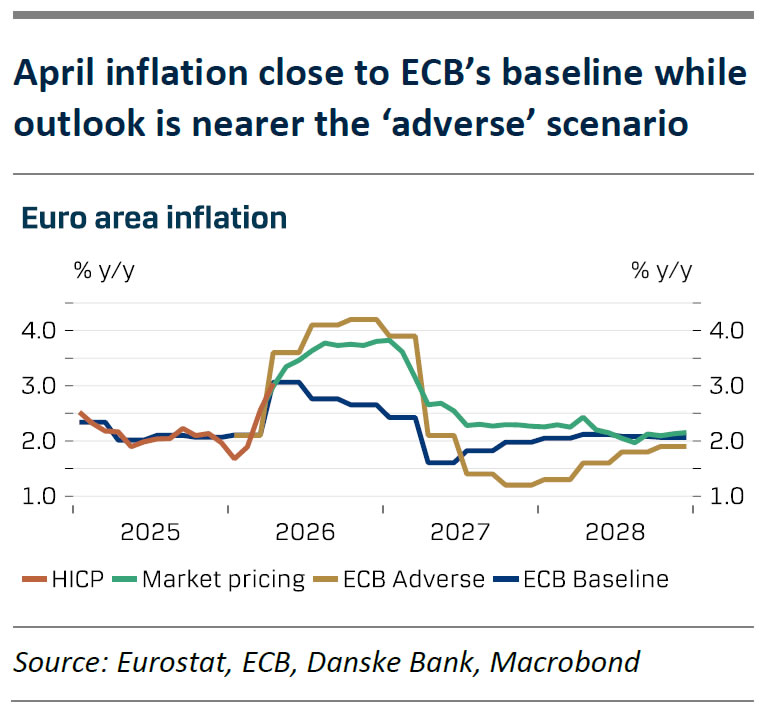

Lagarde stressed that the economy is clearly moving away from the baseline scenario, which aligns with our thinking. Inflation in April rose as expected to 3.0% y/y, similar to the ECB’s March baseline forecast but the outlook is closer to the “adverse” scenario when looking at market pricing (see chart) and seller price expectations rose significantly in the EC’s survey. At the same time Q1 GDP growth was weaker than expected and both consumer confidence, services PMIs, and employment expectations took large hits in April. Since ECB must balance higher inflation with lower growth, we expect two hikes is enough to keep inflation expectations anchored. We therefore keep our call of expecting the ECB to hike policy rates by 25 bp in June and July, bringing the deposit rate to 2.50%. We see risks to the call as tilted to the downside.

{kind=link}