This week, US 10-year Treasury yield has surged through its March-April range in a violent breakout that has pushed yields to fresh 52-week highs and their highest levels since early 2025. This is not just another inflation scare. Markets are beginning to reprice the entire higher-for-longer story all over again — and this time, the move is being fueled by geopolitics, oil, and a rapidly shifting acceptance that the Federal Reserve may need to revert to tightening.

The turning point came after President Donald Trump returned from China without securing a breakthrough on Iran. Markets had hoped Beijing might use its leverage to help pressure Tehran into ending the conflict and reopening the Strait of Hormuz. Instead, Trump appeared to leave empty-handed, leaving oil markets firmly convinced the energy shock is not ending anytime soon. Brent crude has remained pinned near $110, keeping inflation fears elevated and destroying confidence that price pressures will cool quickly enough for the Fed to ease policy.

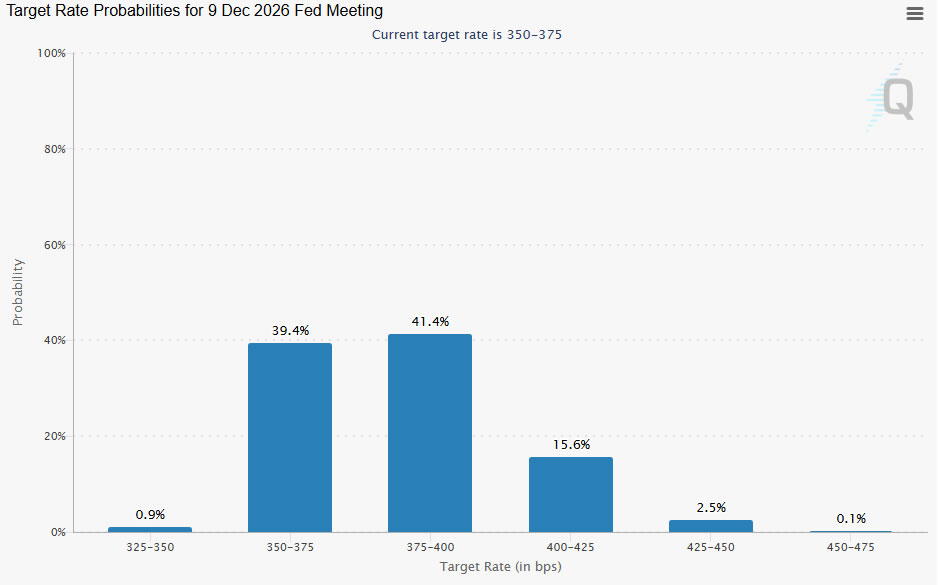

That has cornered the Federal Reserve. Recent CPI and PPI reports already showed inflation remaining stubbornly resilient even before the latest oil surge fully feeds through the economy. Now traders are rapidly capitulating on earlier expectations for rate cuts and instead confronting the possibility that rates may need to stay elevated well into next year — or even rise further. Fed fund futures are now pricing around a 60% probability of another Fed hike before year-end.

The implications are becoming increasingly dangerous for other asset classes. Equities have managed to ignore higher yields for months thanks to AI enthusiasm and resilient earnings. But a risk-free rate approaching 5% changes the valuation equation dramatically. At the same time, soaring Treasury yields are acting like a global vacuum cleaner for capital, sucking money back into Dollar assets and placing enormous strain on emerging market currencies and global liquidity conditions. The Indian Rupee’s collapse to record lows is looking less like an isolated event and more like an early warning sign.

Technically, the next key focus for 10-year yield is 100% projection of 3.96 to 4.48 from 4.23 at 4.75. That level now represents a major near-term line in the sand.

Decisive break above 4.75 could quickly accelerate the move toward 161.8% projection at 5.07, a level dangerously close to the multi-decade highs seen in 2023 and one that could significantly intensify pressure across equities, currencies, and global financial conditions more broadly.

For now, near-term bias remains firmly to the upside as long as 4.48 resistance-turned-support continues holding on any pullback.

{kind=link}