Sterling softened after the latest UK labor market data reinforced expectations that the Bank of England is likely to adopt a more patient near-term stance on interest rates. The sharp decline in payroll employment, rising unemployment rate, and cooling wage growth excluding bonuses all pointed to a labor market that is gradually losing momentum, reducing pressure for immediate additional tightening from the BoE.

Still, the BoE cannot easily pivot dovish given the renewed surge in global energy and import costs. Higher oil prices linked to the Gulf conflict continue threatening imported inflation, and a weaker Pound would only amplify those pressures further. That leaves policymakers in a difficult position: the domestic economy argues for caution, but external inflation risks argue against cutting rates prematurely.

The IMF effectively endorsed that balancing act this week, recommending restrictive policy to prevent energy costs from feeding into broader inflation while also urging the BoE to remain ready to adjust policy “in either direction” if conditions change.

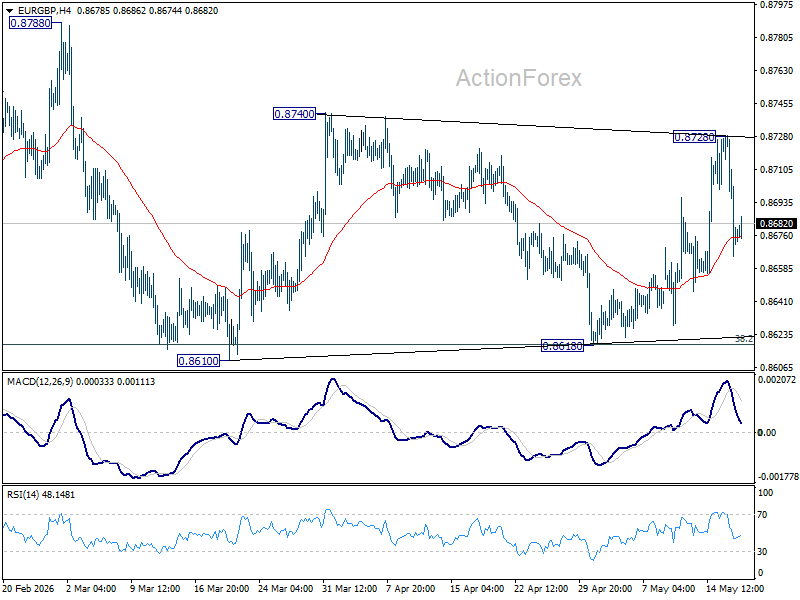

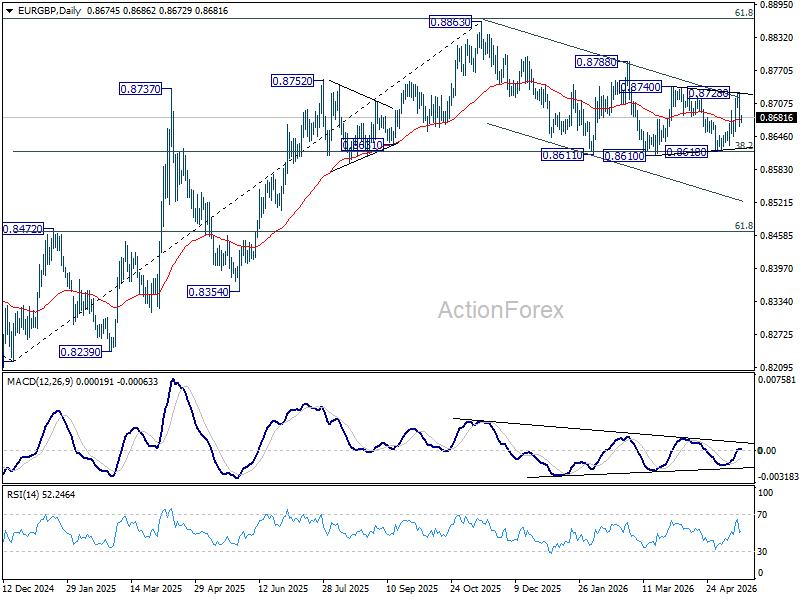

Technically, EUR/GBP remains trapped in an indecisive sideways range. The cross failed to break through 0.8740 resistance and remains capped by the near-term falling channel ceiling, keeping downside risks modestly favored. However, there is also insufficient selling momentum to break below 38.2% retracement of 0.8821 to 0.8563 at 0.8661, leaving the broader direction unresolved for now.

That leaves tomorrow’s UK CPI report as the likely catalyst for the next decisive move. A softer inflation reading could reinforce expectations for prolonged BoE patience and potentially lift EUR/GBP higher through resistance. But if inflation remains sticky — particularly due to energy costs — Sterling may quickly regain support as markets reassess the chance of a BoE hike in the near term.

{kind=link}