Markets are beginning the week with a familiar but dangerous message: oil higher, yields higher, Dollar higher. Brent crude blasted above $111 in Asian trading while US 10-year Treasury yields climbed above 4.6%, extending the “Triple Higher” regime started lats week. Equities across Asia fell as investors rushed to price a worsening geopolitical backdrop, though selling stabilized somewhat into the afternoon as traders shifted into wait-and-see mode ahead of Washington’s next move.

The key issue now is no longer whether tensions are elevated. Markets already know that. The real question is whether the US-Israel-Iran conflict is about to enter a much more dangerous phase capable of producing further disruption to the global energy system. That fear intensified sharply over the weekend after the Trump-Xi summit failed to produce any meaningful diplomatic breakthrough on Iran or the Strait of Hormuz situation.

Attention now turns squarely to Trump’s scheduled Tuesday meeting with national security advisers in the White House Situation Room. According to multiple reports, the meeting will focus on military options regarding Iran after negotiations stalled further. Markets are treating the meeting as a potential turning point that could determine whether the conflict remains within the current framework of “managed tensions” or transitions into a broader and more dangerous phase involving expanded military operations and heightened risks to Gulf energy infrastructure.

In the week ahead, markets will also need to navigate several major economic events that could reshape rate expectations across currencies. The FOMC minutes will be scrutinized for signs of how impatient policymakers were becoming with the latest oil surge, while US PMIs will test whether growth momentum remains resilient enough for rates to stay elevated.

Elsewhere, UK CPI could become especially important for sterling and the BoE as Britain faces both political uncertainty and imported energy inflation pressure. Japan’s national CPI may further strengthen expectations for a June BoJ hike as Yen weakness amplifies imported inflation risks. Australia’s employment data and RBA minutes will shape whether another rate hike stayed in the discussion, while Canada’s CPI report will reveal whether the BoC can continue treating inflation pressures as temporary despite surging oil prices globally.

Key Economic Events — Week Ahead

| Currency | Event | Date |

|---|---|---|

| USD | FOMC Meeting Minutes | Wed, May 20 |

| USD | Flash PMI Manufacturing/Services | Thu, May 21 |

| EUR | Eurozone, Germany, France Flash PMI Manufacturing/Services | Thu, May 21 |

| GBP | UK CPI/Inflation Rate | Wed, May 20 |

| GBP | UK Flash PMI Manufacturing/Services | Thu, May 21 |

| GBP | UK Retail Sales | Fri, May 22 |

| JPY | Japan National CPI/Inflation Rate | Fri, May 22 |

| AUD | RBA Meeting Minutes | Tue, May 19 |

| AUD | Australia Employment Change/Labour Market Data | Thu, May 21 |

| CAD | Canada CPI/Inflation Rate | Tue, May 19 |

Oil Breaks Above $111 as US-Iran Conflict Enters Dangerous New Phase

Brent crude exploded above $111 as failed diplomacy, military escalation, and the UAE infrastructure strike pushed the US-Iran conflict into a dangerous new phase. Read More.

NZ Services Sector Still Contracting Despite April Rebound as Fuel Costs Bite

New Zealand’s services sector showed signs of stabilization in April, with PSI rising from 46.2 to 48.9 and new orders returning to expansion territory. However, businesses continued to warn about rising fuel costs and shipping disruption linked to conflict in the Strait of Hormuz, while smaller firms remained under significant pressure. Read More.

China April Data Misses Across the Board as Domestic Demand Weakens Sharply

China’s April data deteriorated sharply, with retail sales nearly stalling at 0.2% yoy, industrial production slowing, and fixed asset investment unexpectedly turning negative. The weak figures reinforced concerns that rising geopolitical tensions and higher energy costs are weighing heavily on domestic demand. Read More.

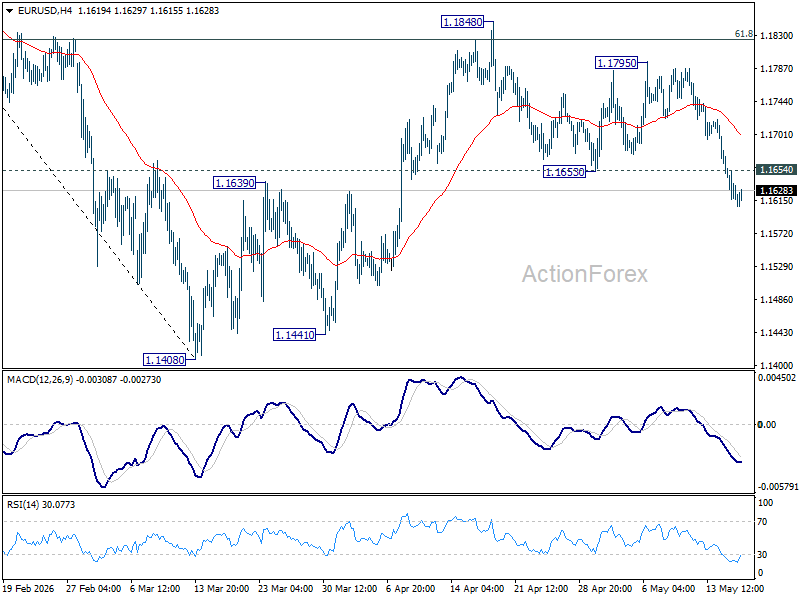

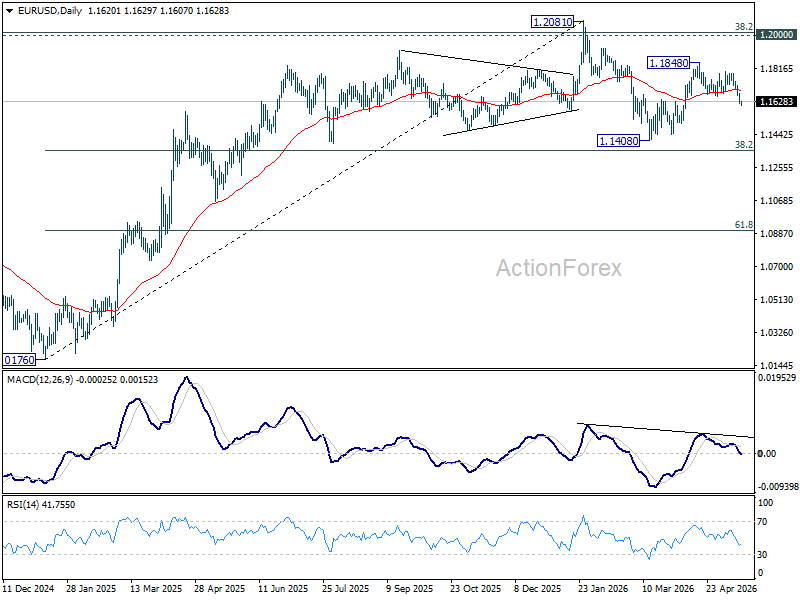

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1603; (P) 1.1637; (R1) 1.1658; More….

Intraday bias in EUR/USD remains on the downside as fall from 1.1848 is in progress. As noted before, rebound from 1.1408 could have completed as a corrective three-wave move. Deeper fall should be seen to retest 1.1408 low. Firm break there resume the whole fall from 1.2081. On the upside, above 1.1654 minor resistance will turn intraday bias neutral first.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1542). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}