Risk sentiment deteriorated sharply today as investors concluded that the Trump-Xi summit failed to deliver a credible diplomatic breakthrough on the Strait of Hormuz, forcing markets to begin pricing a longer-lasting inflation shock tied to prolonged energy disruption. Global equities and precious metals are sold off together as rising oil prices and higher Treasury yields tightened global financial conditions. Dollar surged broadly in response, supported simultaneously by rising US yields, inflation fears, and defensive risk positioning.

China’s Foreign Ministry stated on Friday that shipping routes “should be reopened as soon as possible” and called for a “comprehensive and lasting” ceasefire. However, Beijing provided no operational details regarding how such reopening would be achieved, nor any indication that China would actively pressure Tehran into ending disruption risks in the Strait.

At the same time, the core strategic issue surrounding Iran’s uranium enrichment program remains unresolved. While US President Donald Trump said that: “We don’t want them to have a nuclear weapon,” neither side provided clarity regarding enrichment limits, inspections, or broader nuclear conditions. For markets, the central issue increasingly remains a “black box.”

Instead of signaling de-escalation, investors interpreted Trump’s comments regarding expanded Chinese purchases of US crude as evidence that Washington may be preparing for a prolonged disruption rather than expecting rapid normalization. Trump said after the summit: “China is going to buy oil from the US.” That statement appears to have shifted market thinking away from a “Hormuz reopening” scenario toward a “supply rerouting” scenario.

Markets had previously hoped Beijing would use its leverage as the largest buyer of Iranian oil to pressure Tehran toward reopening shipping routes. Instead, the summit outcome increasingly suggests that global energy trade may simply adapt around continuing disruption, leaving the geopolitical risk premium firmly embedded in oil markets.

That interpretation was reinforced further by comments from Iranian Foreign Minister Abbas Araqchi, who said Tehran has “no trust” in the U.S. and remains skeptical about Washington’s intentions. “Contradictory messages” from the Trump administration have complicated negotiations, Araqchi said, while describing Pakistan’s mediation efforts as being in “difficulty” rather than failed outright.

His comments directly highlighted the contradiction between Washington’s simultaneous military pressure campaign and diplomatic messaging. The remarks suggest any meaningful diplomatic off-ramp remains distant after the conclusion of the Trump-Xi summit.

Markets also reacted to reports that the United Arab Emirates will accelerate expansion of a major oil pipeline through Fujairah by 2027, significantly increasing export capacity that bypasses the Strait of Hormuz altogether. That development carries important symbolic significance. Regional producers themselves appear to be preparing for a world where Hormuz instability persists far longer than initially expected.

In currency markets, Dollar remained the strongest performer of the week by a clear margin, followed by Yen and Euro. Kiwi was the weakest currency, followed by Aussie and Swiss Franc. Sterling and Loonie traded in the middle.

In Europe, at the time of writing, FTSE is down -1.67%. DAX is down -1.75%. CAC is down -1.53%. UK 10-year yield is up 0.181 at 5.175. Germany 10-year yield is up 0.088 at 3.131. Earlier in Asia, Nikkei fell -1.99%. Hong Kong HSI fell -1.62%. China Shanghai SSE fell -1.02%. Singapore Strait Times fell -0.14%. Japan 10-year JGB yield rose 0.07 to 2.705.

Oil Surges Toward $110 as Trump-Xi Summit Signals Supply Rerouting, Not Hormuz Resolution

Oil markets rallied after traders concluded the Trump-Xi summit failed to resolve the Hormuz crisis and instead pointed toward a long-term rerouting of global energy flows. Read More.

USD/JPY Climbs Toward 160 as Rising US Yields Test Japan’s Intervention Resolve Again

USD/JPY climbed back toward the critical 160 level as surging US Treasury yields widened the US-Japan rate gap and intensified doubts over whether Japanese intervention can still effectively stabilize the Yen. Read More.

Japan PPI Surges 4.9% as Energy Shock Intensifies

Japan’s wholesale inflation accelerated sharply in April as higher oil prices, chemical costs, and a weak Yen intensified imported inflation pressures, reinforcing expectations for further BoJ tightening. Read More.

New Zealand PMI Falls to 50.5 as New Orders Turn Negative

New Zealand’s manufacturing sector lost significant momentum in April as new orders fell into contraction territory and firms reported rising freight, fuel, and supply-chain pressures linked to the Iran war. Read More.

USD/JPY Climbs Toward 160 as Rising US Yields Test Japan’s Intervention Resolve Again

USD/JPY climbed back toward the critical 160 level as surging US Treasury yields widened the US-Japan rate gap and intensified doubts over whether Japanese intervention can still effectively stabilize the Yen. Read More.

Japan PPI Surges 4.9% as Energy Shock Intensifies

Japan’s wholesale inflation accelerated sharply in April as higher oil prices, chemical costs, and a weak Yen intensified imported inflation pressures, reinforcing expectations for further BoJ tightening. Read More.

New Zealand PMI Falls to 50.5 as New Orders Turn Negative

New Zealand’s manufacturing sector lost significant momentum in April as new orders fell into contraction territory and firms reported rising freight, fuel, and supply-chain pressures linked to the Iran war. Read More.

Fed’s Williams Sees No Need for Rate Changes Right Now

Fed’s John Williams said policymakers see no urgent need to change interest rates despite rising inflation pressures tied to the Middle East conflict, emphasizing that longer-term inflation expectations remain stable for now. Read More.

Fed’s Barr Says Shrinking Balance Sheet Should Not Trump Financial Stability

Fed Governor Michael Barr warned that proposals to shrink the Fed’s balance sheet by weakening bank liquidity requirements could make the financial system more fragile rather than safer. His remarks highlighted growing debate inside the Fed ahead of the Kevin Warsh era. Read More.

EUR/USD Mid-Day Outlook

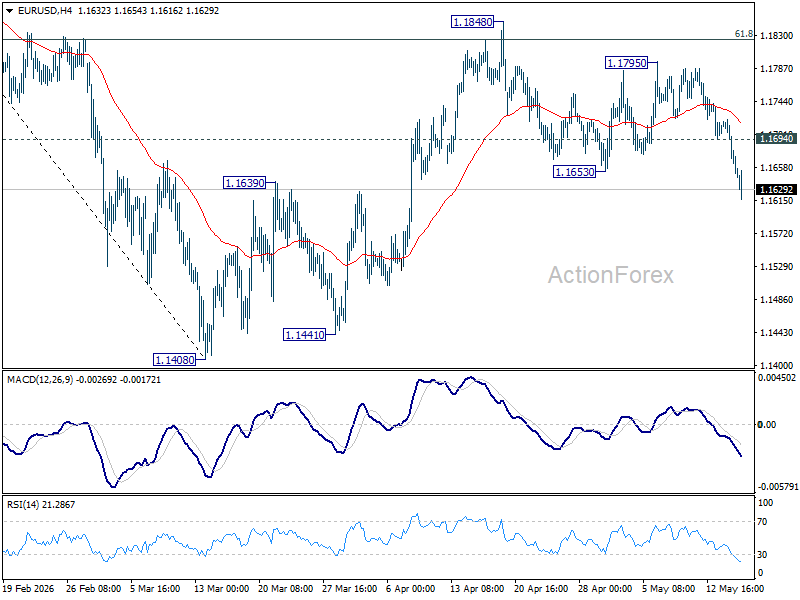

Daily Pivots: (S1) 1.1647; (P) 1.1684; (R1) 1.1703; More….

EUR/USD’s decline continues today and the break of 1.1639 resistance turned support suggests that rebound from 1.1408 has completed as a corrective three-wave move at 1.1848. Intraday bias remains on the downside for retesting 1.1408 low. Firm break there resume the whole fall from 1.2081. On the upside, above 1.1694 resistance will turn intraday bias neutral first.

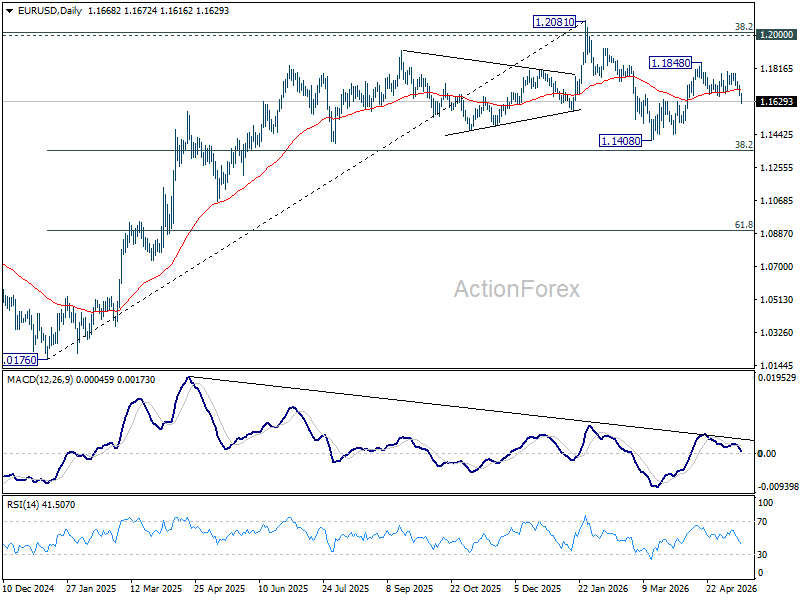

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1539). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}