- Stalled US-Iran talks support high oil prices and periodic risk-off market moves.

- Focus shifts to new Fed Chair and Fedspeak as inflationary pressures accelerate.

- Nvidia earnings could extend or derail the US equity rally; gold lacks bullish catalysts.

- PMIs are key to Euro’s performance; UK political unrest could intensify, weakening the Pound.

- Dollar/Yen rises again as BoJ’s intervention strategy fails.

Middle East Conflict Dictates Market Sentiment

Two-and-a-half months since the start of the US-Iran conflict, and a comprehensive agreement remains elusive. Behind-closed-doors negotiations continue, but there seems to be reduced incentives from both sides to find the solution that will reopen the Strait of Hormuz. This leaves the rest of the world fighting over reduced oil supply, keeping prices above $100, central bankers on edge and causing short-lived episodes of risk-off.

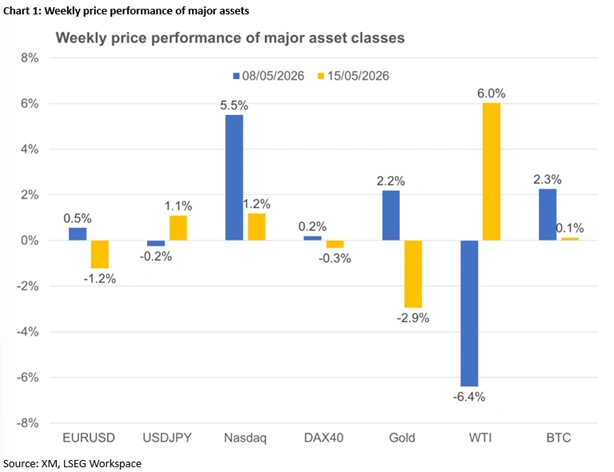

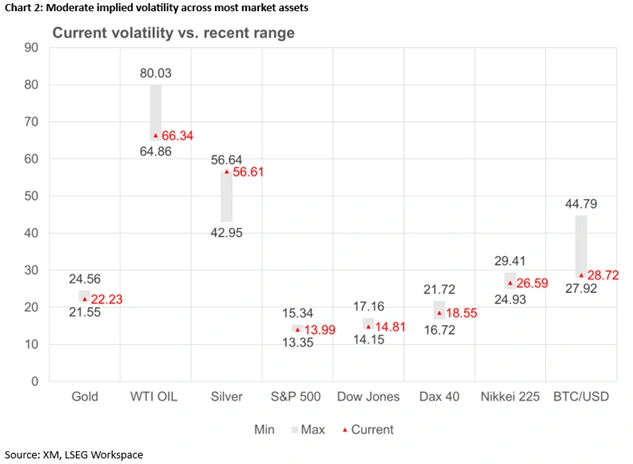

Following a period of range-trading, both the US dollar and gold are on the move, at the time of writing, driven mostly by Middle East headlines. Meanwhile, US equity indices have posted fresh all-time highs, despite the mixed data releases, while, oddly, bitcoin appears to be more responsive to these economic outlook concerns. With implied volatility remaining moderate, which events could shake markets next week?

Chair Powell Is Replaced by Warsh: The End of an Era

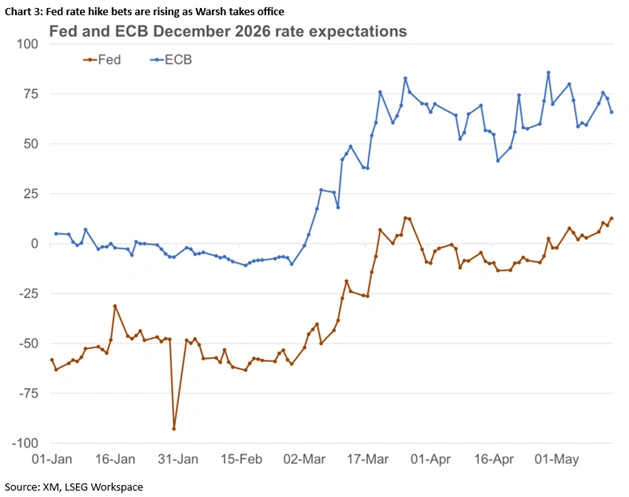

After eight years in charge, Powell’s term as the Chair of the Federal Reserve has been completed, with Kevin Warsh officially taking office. His monetary policy views are still a black box, but the countdown for his first speech, which would be extremely market-moving, has just commenced.

In this context, the minutes from the April meeting will be released on Wednesday. Investors will be interested in the extent of the hawkish debate within the council, and the members’ willingness to decide on a rate change in June. With Warsh in charge, the overall stance could materially shift though, but the minutes and the continued Fedspeak will give a strong indication of where the center of gravity lies within the council.

Various housing data, the preliminary PMIs and the Philadelphia Fed Manufacturing survey would offer valuable information on the underlying economic trends. Notably, despite the strongly accelerating CPI and PPI reports, markets are currently pricing in just 13bps of tightening in December, with the first 25bps rate hike fully priced in by April 2027.

Therefore, the dollar will remain torn between various headwinds and tailwinds. A US-Iran agreement, a harder stance on tariffs and potentially abysmal US Treasury auctions, Wednesday’s 20-year auctions could be the weakest link, might dent the dollar’s appeal, while renewed Middle East headlines keeping the door open to fresh hostilities, beefed up chances of rate hikes, and the continued strong performance by US equities will keep the dollar in demand.

The latter is key, as Wall Street continues to ignore the US economic data, concerns over a global slowdown and rising US Treasury yields, attracting interest from domestic and foreign investors. The focus shifts to the Nvidia earnings announcement on Wednesday, when a stellar report, with an upbeat outlook, would drive major US equity indices even higher. This also means that the bar for disappointment is rather low, as any hint of easing demand or lower investment appetite could hit risk appetite considerably, sending shockwaves across asset classes.

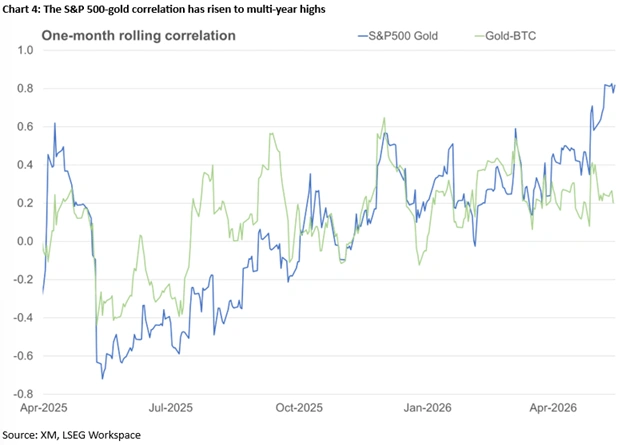

Meanwhile, gold remains driven by the dollar’s bouts of strength, higher Treasury yields and shrinking real rates. When investors eventually refocus on tariffs and the US ballooning debt, gold could surge again, but, at the moment, it remains highly correlated with equities. Interestingly, the one-month correlation between gold and the S&P 500 index has risen to the highest level since October 2012, when gold was drawn into a three-year long decline, losing around 40% of its then value.

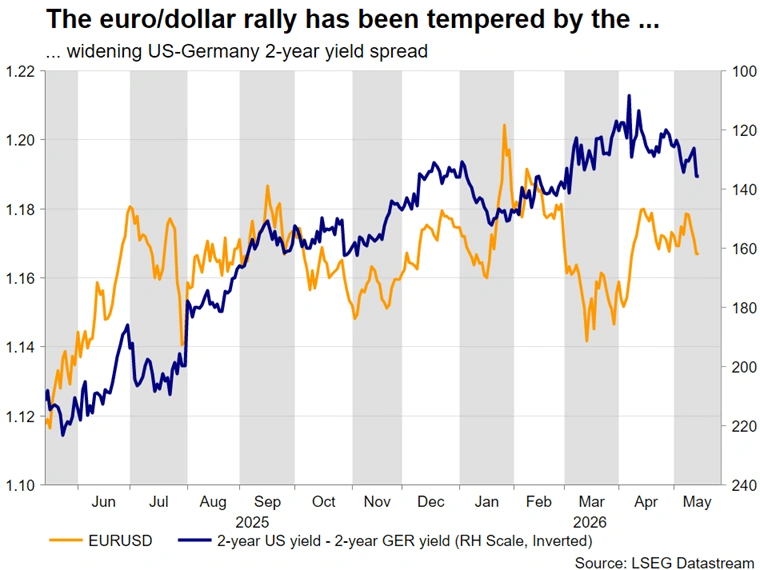

Both the Euro and the Pound Face Various Issues

With inflation indicators edging higher, and the hawks appearing to have the upper hand in the ECB, the June rate hike seems inevitable, unless the US-Iran conflict is sorted fairly swiftly, with the Euro benefiting from the dollar’s broad weakness.

ECB doves are focused on the likely economic slowdown, and hence a weak set of PMI figures next week, showing for example a drop in the Germany Manufacturing PMI below 50, will not be taken lightly by the doves. That said, with the ECB’s price stability mandate and the price subindices of both German Services and Manufacturing PMIs rising to multi-year highs in April, rate hike bets will remain supported even if the Euro finds itself under selling pressure on expectations for a weak Q2 GDP performance.

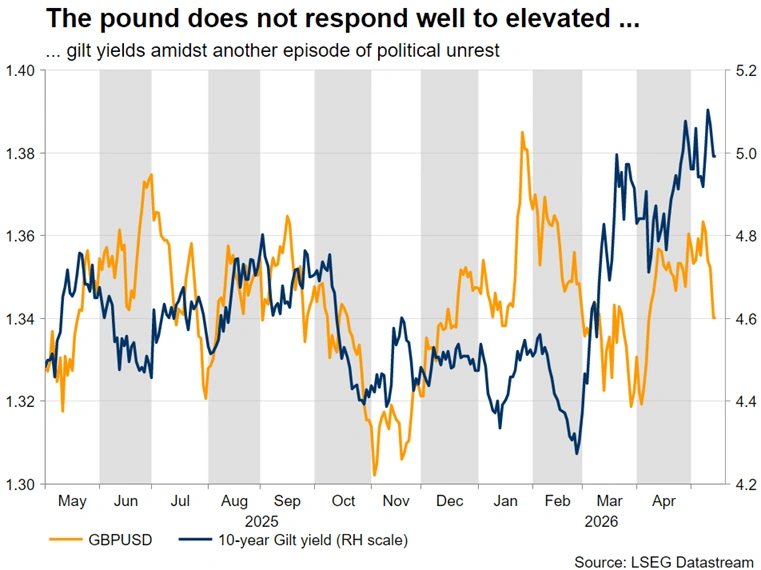

The situation is far more complicated in the UK. PM Starmer’s days in charge appear to be numbered, with the probability of a more left-leaning PM taking office rising daily, bringing back memories of the Truss market rout. Long-term gilt yields have climbed to a two-decade high, with the 30-year hovering above 5%, while the Pound is down 2% against the Dollar this week.

Meanwhile, despite the satisfaction with the Q1 and March GDP and production figures, economic sentiment remains weak, especially as there are concerns about consumer spending. This sentiment will be tested next week, with a barrage of data for April and more specifically, the Claimant Count figure, and the inflation and retail sales reports.

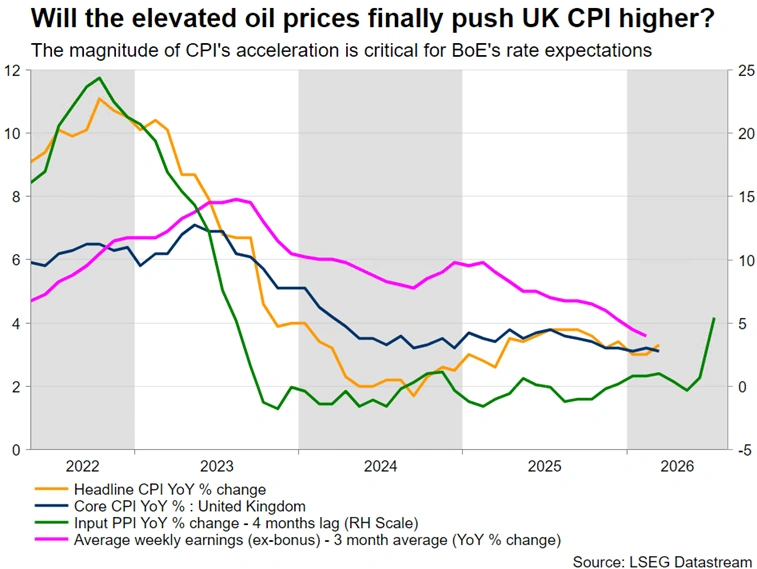

In particular, a jump in CPI near 4%, coupled with a weaker set of preliminary PMI surveys, which coincidentally have been holding up very well with the April Manufacturing survey climbing to a four-year high despite the evident inflation acceleration, would deepen the schism within the MPC ranks. The hawks are expected to become even bolder about their intention to support a June rate hike, with Pound traders being more worried about the growth outlook and the political unrest.

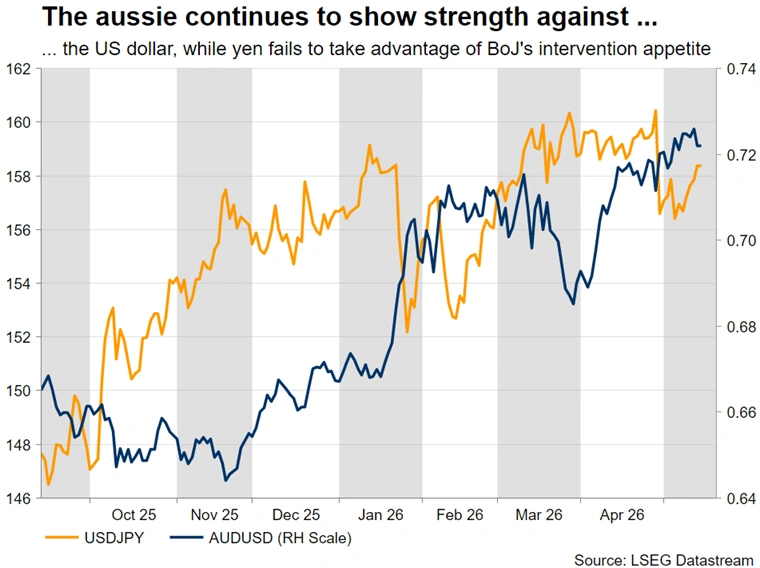

Never-Ending Pressure on the Yen

After dropping by five big figures on April 30, Dollar/Yen has climbed above 158 again, as investors are reacting to the weak approach by Japanese officials in terms of actual market intervention. Understandably, a sustainable Yen rally needs strong economic data and a realistic chance of tighter policy ahead, both of which could improve next week. A strong Q1 GDP report, along with another jump in the manufacturing PMI survey and further hawkish rhetoric from BoJ officials, could convince investors that a BoJ June rate hike is more likely than not.

Loonie’s Mixed Outlook, Aussie Focuses on China’s Data

Aussie traders will watch Monday’s Chinese data for some much-needed signals that the Chinese economy is finally over the recent prolonged soft patch, though such signals are highly unlikely considering the wider economic tensions, and Tuesday’s RBA minutes for hawkish signs to trigger another upleg in Aussie/Dollar.

In the meantime, the Loonie has been on the back foot in May, with the focus shifting to Tuesday’s April CPI report and Friday’s retail sales figures. An initial Loonie rally due to a potentially strong upside surprise in inflation would fade if retail sales data point to deteriorating domestic demand. Stagflation would complicate the BoC’s outlook, with the balance tilting towards rate cuts if tariff developments return to the spotlight again.

{kind=link}