Markets stopped panicking — for now. After opening the week with a sharp risk-off move driven by surging oil prices and fears of wider Middle East escalation, traders shifted back into wait-and-see mode as the US session approached. Brent crude slipped back below $110, US futures recovered from deeper losses, and broader market sentiment steadied as investors reassessed whether diplomacy might still have one final opening left.

That stabilization was triggered by reports that Pakistan had delivered a revised Iranian proposal to Washington aimed at ending the war in the Middle East. Iranian officials later confirmed that Tehran’s position had indeed been conveyed to the American side through Pakistani mediation. While details remain unclear, the mere existence of a renewed diplomatic channel was enough to cool some of the panic that had swept through energy markets earlier in the day.

But markets are not suddenly optimistic. The mood is closer to conditional calm — a temporary pause because no new escalation has happened yet. Investors broadly understand that time may be running out for negotiations. US President Donald Trump’s Tuesday Situation Room meeting with national security advisers is now looming over global markets as the next major decision point. Reports indicate the White House is explicitly reviewing options for military action against Iran after diplomacy stalled further following the failed Trump-Xi summit last week.

Meanwhile, the oil market itself is becoming increasingly unstable beneath the surface. Reports that Europe could face shortages within weeks are colliding with the approaching end of the seasonal demand lull. As Memorial Day travel demand in the US and holiday consumption in the UK begin lifting fuel demand again, the oil market could enter a “non-linear” phase where physical shortages force buyers to bid aggressively for supply regardless of valuation.

That possibility matters because non-linear commodity moves tend to spread rapidly across the entire macro landscape. Higher oil feeds inflation fears, pushes Treasury yields higher, supports the Dollar, and pressures equities simultaneously. It also explains why traders remain reluctant to fully embrace today’s calmer tone even as Brent retreated from its highs.

In FX markets, Yen led losses as immediate panic hedging faded, while Sterling outperformed alongside Kiwi and Aussie as broader sentiment stabilized modestly. Dollar and Loonie also weakened slightly as oil pulled back from peak levels. Euro and Swiss Franc traded more defensively in the middles.

In Europe, at the time of writing, FTSE is up 0.45%. DAX is up 0.86%. CAC is down -0.32%. UK 10-year yield is down -0.06 at 5.122. Germany 10-year yield is down -0.013 at 3.157. Earlier in Asia, Nikkei fell -0.97%. Hong Kong HSI fell -1.11%. China Shanghai SSE fell -0.09%. Singapore Strait Times rose 0.15%. Japan 10-year JGB yield rose 0.041 to 2.746.

Gold Slips Below 4500, May Stabilize Near 4200 Unless Brent and Treasury Yields Break Crisis Levels

The latest drop in Gold below 4500 is being driven less by fading safe-haven demand and more by rising oil prices, Treasury yields, and “higher for longer” interest rate fears. The next key test sits near 4200. Read More.

Oil Breaks Above $111 as US-Iran Conflict Enters Dangerous New Phase

Brent crude exploded above $111 as failed diplomacy, military escalation, and the UAE infrastructure strike pushed the US-Iran conflict into a dangerous new phase. Read More.

NZ Services Sector Still Contracting Despite April Rebound as Fuel Costs Bite

New Zealand’s services sector showed signs of stabilization in April, with PSI rising from 46.2 to 48.9 and new orders returning to expansion territory. However, businesses continued to warn about rising fuel costs and shipping disruption linked to conflict in the Strait of Hormuz, while smaller firms remained under significant pressure. Read More.

China April Data Misses Across the Board as Domestic Demand Weakens Sharply

China’s April data deteriorated sharply, with retail sales nearly stalling at 0.2% yoy, industrial production slowing, and fixed asset investment unexpectedly turning negative. The weak figures reinforced concerns that rising geopolitical tensions and higher energy costs are weighing heavily on domestic demand. Read More.

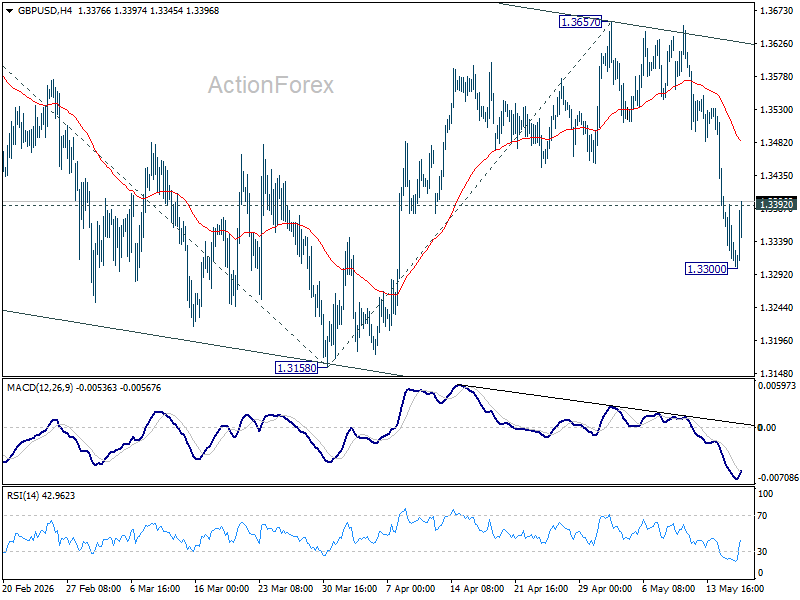

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3290; (P) 1.3347; (R1) 1.3379; More…

Intraday bias in GBP/USD is turned neutral first with current recovery, and some consolidations would be seen above 1.3300 temporary low. Further fall is expected as long as 55 4H EMA (now at 1.3483) holds. Below 1.3300 will target a retest on 1.3158 support first. Decisive break there will target 100% projection of 1.3867 to 1.3158 from 1.3657 at 1.2948. However, sustained break of the EMA will dampen the bearish case and turn bias back to the upside for 1.3657 resistance instead.

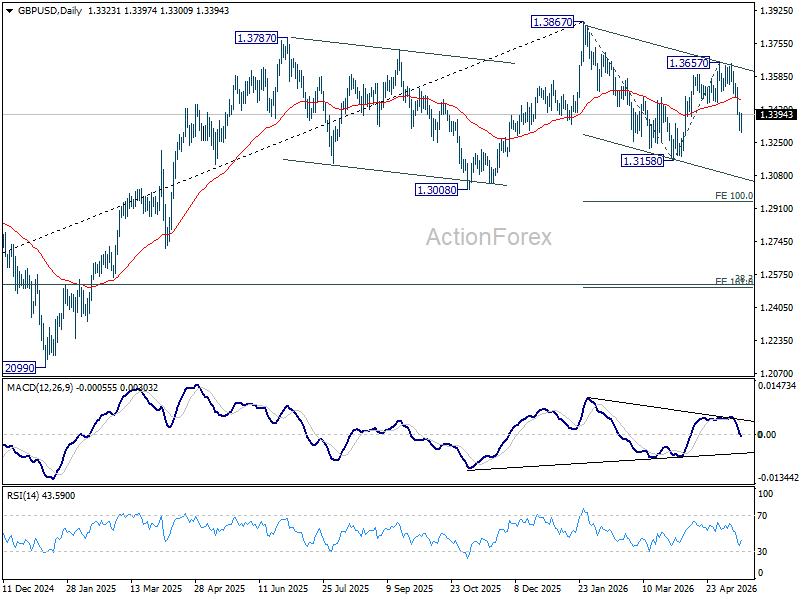

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is in favor for a later stage, towards 1.4248 key resistance (2021 high). However, firm break of 1.3008 will at least bring deeper fall to 38.2% retracement of 1.0351 to 1.3867 at 1.2524, with increased risk of bearish reversal.

{kind=link}