Gold came under renewed pressure earlier today, briefly breaching below $4,500 level as the recent decline resumed. Although the precious metal later recovered some ground, the broader near-term outlook remains tilted to the downside as rising oil prices continue driving Treasury yields and Dollar higher together. The combination is creating an increasingly difficult environment for non-yielding assets, particularly as markets begin repricing inflation and interest rate expectations again.

The key driver behind Gold’s weakness is the oil-led inflation shock developing alongside escalating Middle East tensions. Brent crude’s surge above $111 has reinforced expectations that major central banks, especially the Federal Reserve, may need to keep interest rates elevated for longer despite slowing global growth. Higher oil prices feed directly into inflation expectations, which in turn lift benchmark yields and support the Dollar.

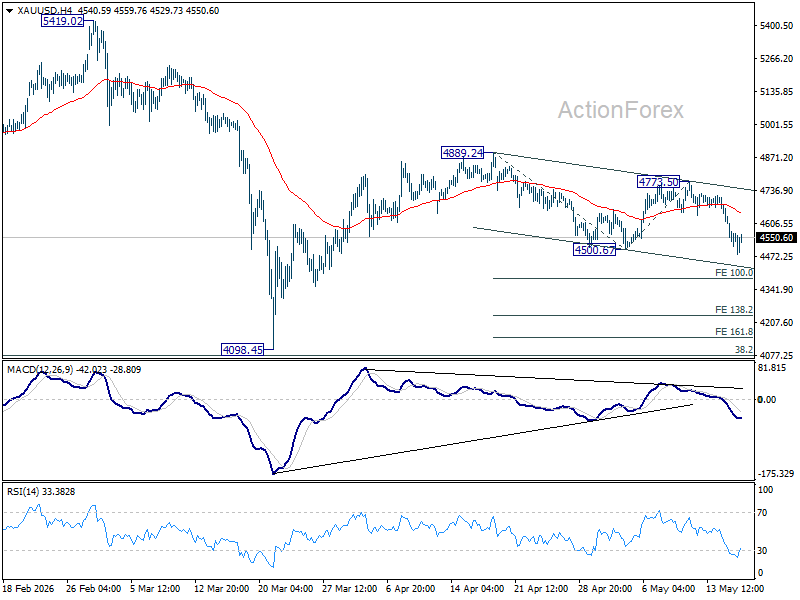

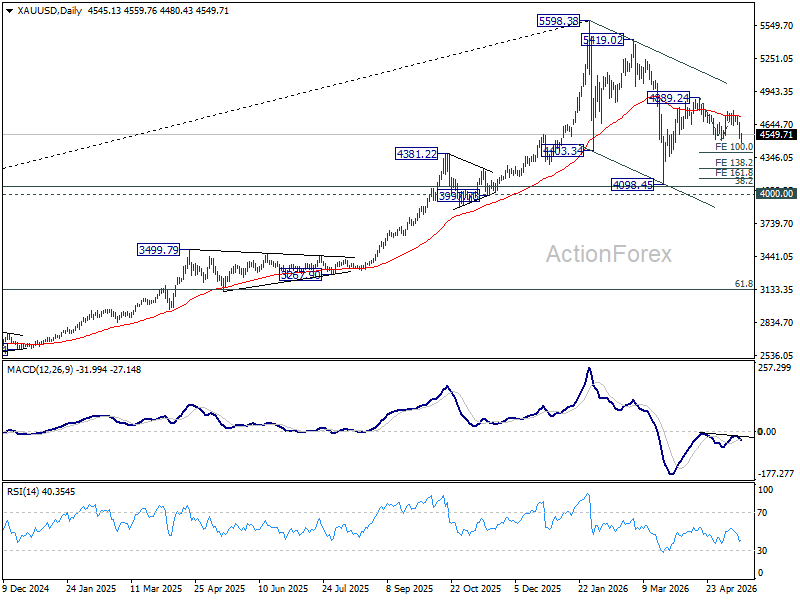

Technically, Gold remains vulnerable while 55 4H EMA (now at 4,649.90), caps rebounds. Further decline is expected toward 100% projection of 4,889.24 to 4,500.67 from 4,773.50 at 4,384.93. However, downside momentum has not yet become disorderly, and there should be meaningful support emerging between the 4,200 and 4,300 region. In particular, 138.2% projection level at 4,236.49 would likely provide a floor for stabilization. Overall, the current decline is viewed as the second leg of the broader corrective pattern from 4,098.45 low.

Still, that relatively stable outlook depends heavily on oil and bond markets remaining contained. If Brent crude remains below $120 crisis threshold and US 10-year Treasury yields stay below 5%, Gold should stabilize around the mentioned 4200/4300 region and then attempt a rebound. However, decisive break of either of those macro levels would likely trigger another wave of aggressive selling in Gold, quickly exposing the key psychological support around 4,000.

{kind=link}