The April CPI rose 0.4%mth to be up 4.2%yr.

The April CPI rose 0.4%mth to be up 4.2%yr. This represents a moderation from the 4.6%yr pace recorded in March and came in below Westpac’s near-cast of 0.9%mth/4.8%yr and market expectations of 4.4%yr. April is normally a seasonally strong month; the seasonally adjusted figure recorded a fall (–0.1%mth), compared with our nowcast of 0.3%mth. Much of the miss was concentrated in volatile or policy-affected items that do not speak to the pass-through of energy prices and other supply effects stemming from the conflict in the Middle East.

The miss to the downside was from:

- a sharper-than-expected decline in transport (–2.7%mth vs our –1.1% near-cast, subtracting 0.3ppts)

- a softer international travel result (+3.4%mth vs +9.7%mth).

- a fall in fruit prices also contributed to the weakness (-2.2%mth vs +4.6%mth)

- a softer rise in clothing & footwear prices (3.9%mth vs 4.7%mth).

On the upside:

- health was firmer than expected (+2.6%mth vs +1.9%mth), contributing 0.2ppts.

- new dwelling purchase prices picked-up further in April, rising 0.7%mth above our expectations for a 0.4%mth lift. This was the largest increase since November 2023.

- rents were broadly on par with last month’s increase and our expectations (0.2%mth).

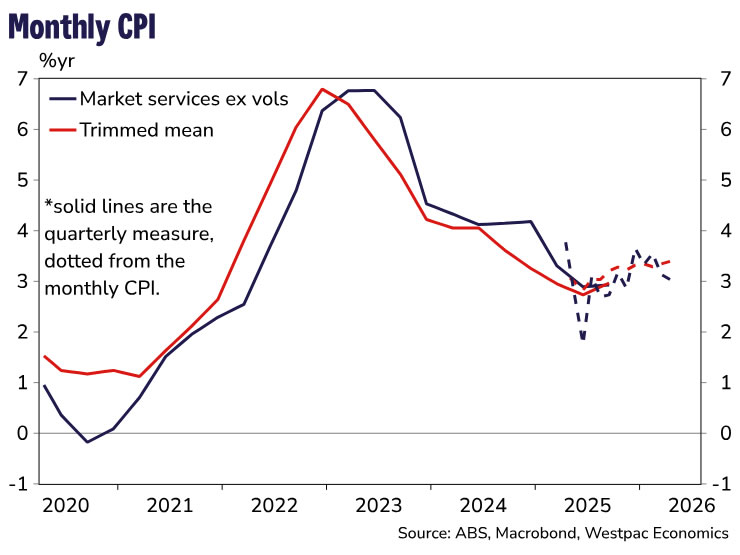

The monthly Trimmed Mean rose 0.3%mth, slighter softer than our expectations for a 0.4%mth lift. Nevertheless, the annual pace lifted slightly to 3.4%yr from 3.3%yr in prior month. The six-month annualised paced continued to ease, down to 3.2% from 3.8% in December.

While the headline April CPI was softer than expected, underlying inflation pressures are still building. The April data show clearer evidence of emerging pass-through of upstream costs. Home-building is the most obvious example, but ongoing above-target inflation in categories such as takeaway food and restaurant meals are also consistent with pass-through building.

The lift in upstream costs flowing into selling prices is also evident in the NAB business survey and ABS business indicators. Further construction trade price increases and the new fuel recovery rule for transport operators will add to near-term cost pressures. Consequently, we still expect Trimmed Mean inflation to rise to around 4% over the coming quarters.

While the headline figure was a (welcome) downside surprise, it was not a view-changing one.

As the RBA has also highlighted in recent research, pass-through of higher energy and regulatory costs to other prices is likely to be larger and faster than normal given the size of the shock. Today’s data showed some signs of this pattern, just not as much as we feared. We also think the RBA will mostly look through the apparent weakness in April labour force data, alert to the same unusual seasonality that we noted last week.

, compared with our nowcast of 0.3%mth. Much of the miss was concentrated in volatile or policy-affected items that do not speak to the pass-through of energy prices and other supply effects stemming from the conflict in the Middle East.){kind=link}