- As widely expected, the RBNZ held the OCR at 2.25%.

- The three internal members voted for no change – including the Governor, with her casting vote – and the three external members voted for a 25bp hike.

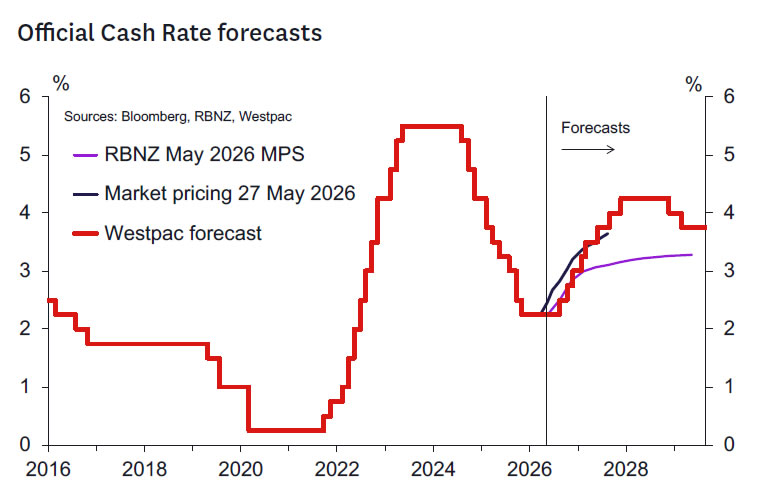

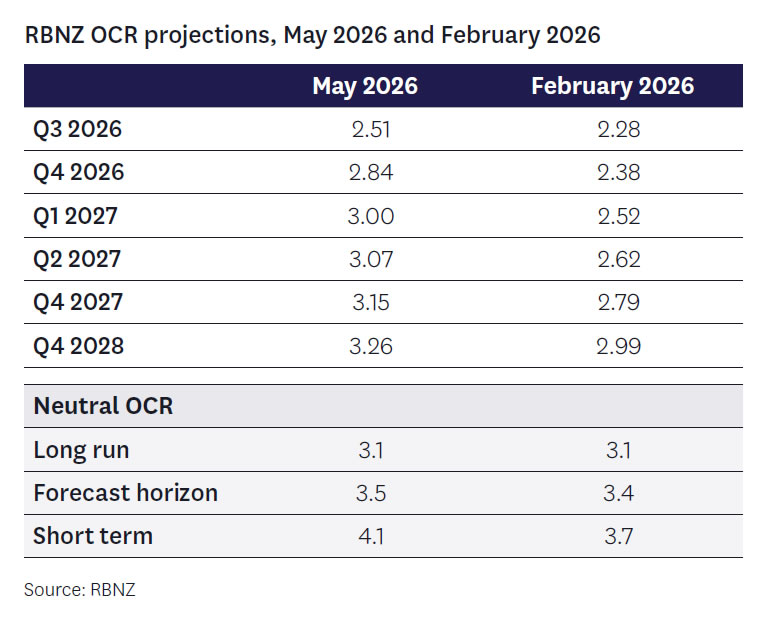

- The RBNZ’s revised OCR forecast signals three 25bp OCR increases in 2026 and a further modest lift in 2027.

- The RBNZ has significantly revised down its outlook for growth, but risks are viewed as still skewed to the downside.

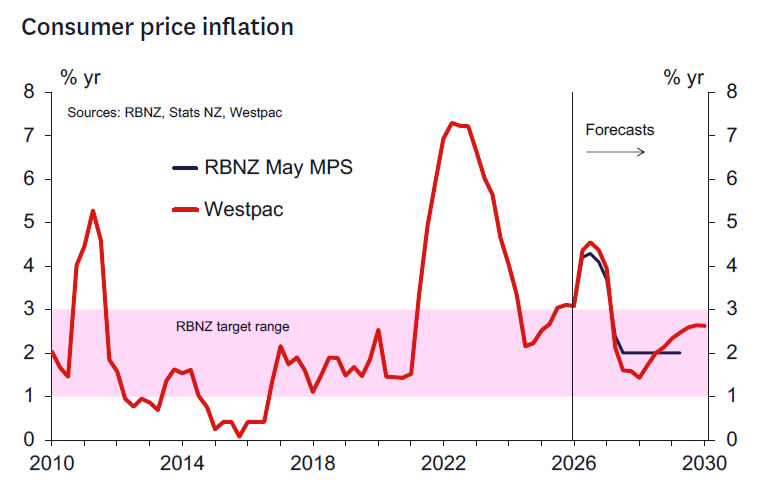

- The RBNZ has revised up its forecast of inflation to a peak of 4.3% in Q3 2026. While inflation is forecast to return to 2% in mid-2027, risks are viewed as skewed to the downside.

- Westpac continues to expect that the OCR will remain unchanged in July, and that it will be increased in September, October and December. Our medium-term OCR forecast remains unchanged.

- The delay in beginning the tightening cycle increases our confidence that the OCR will need to rise to 4.25% ultimately before inflation is sustainably returned to 2%. The Governor appears keen to wait until the RBNZ sees the “whites in the eyes” of core inflation before responding. That inevitably means the RBNZ will be late to the party.

Key take out: OCR rising in 2026, but a July start remains in the balance.

As widely expected, the RBNZ held the OCR at 2.25% and a vote was required to determine the outcome. Also as expected, the RBNZ’s revised projections include a pulling forward of the timing of projected policy tightening. The end 2026 OCR forecast was lifted to 2.84% – close to our 2.8% expectation.

The MPC seems finely balanced in terms of the start of the tightening cycle, but united in the view that the OCR rises towards 3% by the end of this year. Also, there is a strong sense that the OCR will ultimately need to increase to the low 3’s.

With a 3:3 split in the MPC the onus possibly falls to the internals and effectively the Governor to get over the line for a hike. These members are looking for evidence of increased core inflation, along with signs of pressure on wages and inflation expectations. We don’t think the RBNZ will get meaningful information on that until just before the September meeting.

The other key factor is the progress of the war, which perhaps suggests this dovish group thinks that things might be resolved soon, allowing more room to wait. We think they will be disappointed there.

Another issue is the path of the data, with dovish members noting some data was weaker than expected. Looking ahead, our Q2 GDP forecast is -0.3% vs their 0%, so there is some scope for disappointment there. The Record of Meeting explicitly notes that the Committee sees the risks are to the downside for domestic growth. Neutral rate estimates were revised up perhaps more than we thought, but clearly laying the basis for increased rates soon enough.

The main fly in the ointment of this argument is the potential for a new MPC member be appointed – expected in June – and hence their view might be influential. Having said that, one wonders if a brand-new member will be keen on deviating from their internal colleagues’ opinion in that first meeting.

The bottom line is that the OCR is rising in 2026 and looks set to end 2026 at the 3% level we currently forecast. We are not convinced that the OCR will increase in July, given the lack of evidence we think will be available on core inflation, wages and long-term inflation expectations pressures. The Governor emphasized the role of long term 5–10-year inflation expectations in her assessment that expectations remain well anchored. Information on these indicators will not be available before the July meeting. Hence the thesis the RBNZ will wait to see the “whites of the eyes” of persistent inflation pressures remains the base case.

The RBNZ makes a strong case for a higher OCR this year but is delaying action. That’s unfortunate and does confer risks of a turnaround in the future and increases confidence that we will need to see 4% plus interest rates before CPI inflation is brought to heel. However, the Governor’s vote today was in line with her previous messaging which strongly suggested a high bar to consider lifting the OCR today. It seems sensible to assume she will continue to pursue that strategy. The big surprise was that it was the external members that have swung decidedly hawkish. That’s telling but the internal consensus needs to flip to get the tightening cycle going.

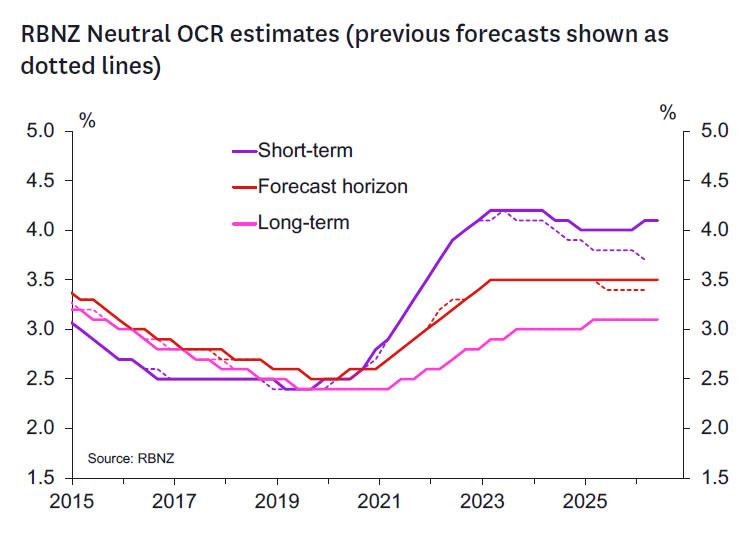

The RBNZ’s OCR projection has been revised higher and now peaks at 3.28% in June 2029 (their previous forecasts from February rose more gradually, peaking at 3% in 2029). There were also upward revisions to the RBNZ’s forecasts for the “short-term” and “forecast horizon” measures of the neutral level of the OCR (the “long-run” measure was unrevised).

The upward revision to the RBNZ’s OCR profile reflects the sharp rise in inflation pressures stemming from the Middle East conflict. While the recent rise in fuel prices is expected to be temporary, there are expected to be longer lasting pricing impacts that will add to the pressure on inflation at medium term horizons. The evolution of wage and price setting behaviour was noted as expected to be a key influence on how quickly the OCR will rise.

The RBNZ’s forecasts for the OCR in 2026 are similar to our own. However, after early 2027 the RBNZ’s forecasts rise more gradually compared to our own (as we expected).

Westpac’s OCR call.

We continue to expect no change in the OCR in July and 25bp hikes in September, October and December. Our longer-term OCR forecasts remain unchanged.

A July hike can’t be ruled out and probably hinges on the strength of the economy and the assessment of the level of excess capacity that comes to light between now and July. We suspect their concerns on further downside risks will be borne out.

We may get some additional colour from the Governor on the likelihood of a July hike in her post Statement media appearances.

RBNZ forecast detail.

Overall, the RBNZ’s forecasts for economic conditions are similar to our own.

On inflation, the RBNZ expects inflation will peak at 4.3% this year. That’s just slightly lower than our forecast for a peak of 4.5%. However, given the volatility in oil prices and broader ructions in the global economy, it’s not a major difference.

The RBNZ expects that inflation will drop back next year when oil prices eventually ease, and their forecast show annual inflation settling comfortably at 2% from mid- 2027. In contrast, we think that inflation could fall back more sharply next year. But that’s due to swings in oil prices, rather than a difference in views on underlying economic conditions.

However, while we see more downside risk for imported inflation next year, we continue to think the RBNZ is underestimating the upside risk for non-tradables prices (and hence overall inflation) at longer horizons. Despite a modest upwards revision to the RBNZ’s nontradables inflation forecasts, they still settle at relatively benign levels. In contrast, we expect the continued large increases in council rates and other administered prices will keep domestic inflation at firmer levels for an extended period. That risk has been compounded by the recent increases in global oil prices and other input costs.

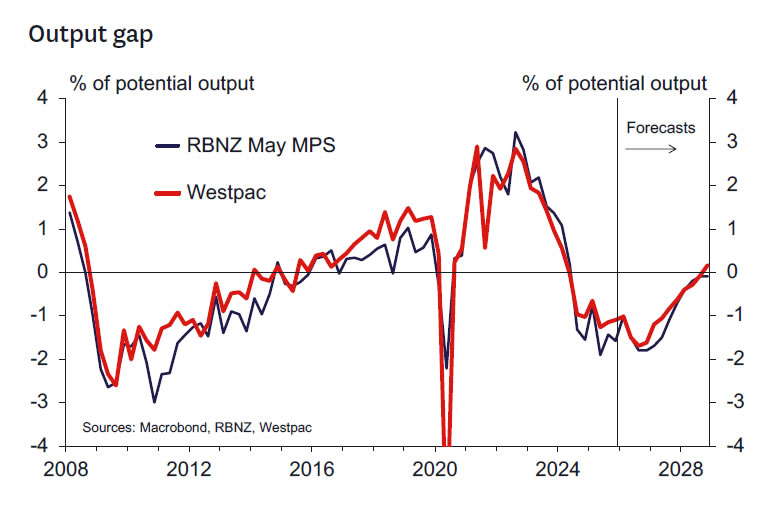

On activity, the RBNZ’s forecast for GDP growth, the labour market and the output gap are all broadly similar to our own. Forecasts for GDP growth have been revised down. Higher living costs are expected to be a drag on household spending. Similarly, the downturn in economic conditions is expected to dampen hiring and investment spending by businesses. That softness in demand is expected to offset some of the upward pressure on consumer prices, but not enough to prevent a sharp lift in inflation in the near term.

Alternative scenarios.

We’re not surprised to see that the RBNZ considered multiple scenarios around the outlook for the economy, given the current uncertainty stemming from the Middle East conflict. The focus of these scenarios, though, was the uncertainty around how economic activity and inflation might respond, rather than the path of oil prices per se.

- In the first scenario, the conflict lasts longer than assumed in the central projection, with Dubai crude oil prices reaching $120/bbl, holding there over the rest of this year, and only falling back as far as $100/bbl in later years. Firms respond by pre-emptively raising their prices in a coordinated manner, along the lines of the model that external MPC member Gai set out in his recent speech. Annual inflation peaks at 5.8%, and the OCR needs to rise faster and further to bring inflation back to target.

- The second scenario assumes the same oil price track as above, but with more restrained pricing behaviour by firms. Inflation does spike to around 5% in the near term, but does not become as persistent, and the OCR does not need to rise much more than in the baseline projections.

- The third scenario assumes the same oil price track as in the baseline forecasts, but with a larger negative demand shock for the global and domestic economies. Inflation initially spikes to around 4% but falls back within the target range more quickly as firms struggle to pass on higher costs, and the OCR remains on hold at 2.25% for some time to combat a further deterioration in demand.

The value of these scenarios is not in trying to predict exactly how things will pan out, but to convey the RBNZ’s response function under a range of different conditions. With that in mind, what can we take from these? One key takeout is that the policy responses are asymmetric in terms of time horizons. Under the first two scenarios, the OCR track doesn’t diverge much from the baseline projection until late 2026 or early 2027, as it takes time to determine whether second-round price effects are occurring beyond the initial oil price shock. In contrast, the weak demand scenario has an immediate impact – the OCR track allows no possibility of a hike in July, September, or any time soon. If we’re in the scenario 3 world, this will likely become apparent from the activity data over the next couple of months.

Notably, the RBNZ has only explored scenarios where oil prices are either in line with or higher than their central forecast. That leaves open the question of how the RBNZ would respond to a favourable oil price ‘shock’ – indeed, oil prices are currently below the RBNZ’s central projection, which would have been finalised a week ago. Presumably a sustained pullback in oil prices would bring the RBNZ somewhere closer to its pre-conflict view of the world – with the economy gradually recovering and the OCR eventually being raised to a more ‘neutral’ level.

Key things to watch ahead of the RBNZ’s 8 July OCR Review.

The next RBNZ policy review will take place on 8 July. A key focus between now and then will be on developments in the Middle East, and their impact on trading partner growth and key export and import commodity prices. The RBNZ’s scenarios seem to focus on the idea of higher for longer oil prices. While we think that’s appropriate, if oil prices shift by enough to bring down inflation forecasts significantly then this might assuage concerns of inflation persistence a bit.

The domestic data flow between now and then is relatively light. The most important domestic economic releases are:

- The Q1 GDP report (18 June): While this data largely predates the Middle East conflict, the outcome will be compared to the RBNZ’s estimate, with any deviation having implications for the RBNZ’s estimate of the output gap. The RBNZ’s forecast of 1.0% growth is slightly firmer than our own view (0.8%q/q).

- The May Selected Price Indexes (16 June): With the Q2 CPI report not released until 21 July, the RBNZ will have limited pricing data with which to assess whether inflation is beginning to broaden beyond the firstround direct impact of higher energy prices.

- The April and May filled jobs reports (28 May and 29 June): With the next Household Labour Force Survey not due until 5 August, the Monthly Employment Indicator will provide insight as to whether renewed business sector caution is spilling over into greater labour market slack.

In addition to the above, key monthly indicators such as the BusinessNZ manufacturing and services indexes (mid- June) and the ANZ Business Outlook survey (end of May and June) will also be of interest. The next QSBO survey is not released until 14 July, although it is possible that the RBNZ will receive a heads-up on how this is shaping up prior to the 8 July policy decision. Developments in retail spending and housing-related indicators will also be monitored to judge the how the energy price shock is impacting activity. The RBNZ will also monitor movements in key export commodity prices and financial conditions.

Notable quotes.

Some notable quotes from the today’s RBNZ commentary were as follows:

Current state of the economy

“ Domestically, business contacts and surveys indicate weaker confidence and spending. For some firms, rising costs are squeezing profit margins and curbing investment and hiring intentions”

“ Indicators of economic activity have deteriorated, in some cases more quickly than anticipated.”

The Middle East

“ The Committee noted that the outlook for energy prices depends on how the conflict evolves, the extent of damage to energy infrastructure in the Middle East, and the speed with which global supply chains adjust.”

“ Members noted that these events will encourage firms to permanently reconfigure their supply chains to reduce exposure to the region. Along with stronger global demand for renewable energy, this may place further upward pressure on global energy prices in the near term.

Growth outlook

“ Near-term economic activity is likely to be weaker than assumed…”

“ Annual GDP growth in 2026 is now expected to be 0.9 percentage points lower…”

“ The balance of risks is… to the downside for growth.”

Output gap/excess capacity

“ Unemployment remains elevated, indicative of spare capacity in the labour market.”

“ Spare capacity in the economy is likely to dampen second-round inflationary pressure.”

Inflation outlook

“ Inflation is expected to peak at 4.3 percent in the September quarter…and to return to the 2 percent target mid-point in mid-2027.”

Inflation expectations

“ Medium- to long-term inflation expectations remain consistent with inflation returning to the 2 percent target mid-point…”

“ While shorter-term inflation expectations have increased, medium- to longer-term expectations remain close to 2 percent.”

Current policy stance

“ Financial conditions have tightened materially this year…”

Risks to the inflation outlook

“ The balance of risks is to the upside for inflation…” Global growth

“ New Zealand’s trading partners are expected to see weaker growth and higher inflation.”

“ The Middle East conflict poses downside risks to global economic activity.”

Outlook for monetary policy

“ The OCR will most likely need to increase sooner and by more than envisaged…”

“ All Committee members agreed that increasing the OCR at upcoming meetings would likely be necessary…”

“ The pace of OCR increases will depend on… wage- and price-setting behaviour versus weaker economic activity…”

{kind=link}