Dollar strength remains the dominant theme in global markets as investors continue to digest the Federal Reserve’s hawkish shift. The greenback extended gains broadly after policymakers effectively endorsed another rate hike this year and left the door open to additional tightening if inflation remains stubborn. Markets are now confronting a realistic scenario in which the Fed raises rates once, or even twice, before year-end. That repricing has provided a powerful tailwind for the Dollar, helping it maintain leadership in the currency markets throughout the week.

Yet unlike previous episodes of aggressive Fed repricing, risk sentiment has proven remarkably resilient. The post-FOMC selloff in US equities already appears to be fading, with futures pointing to a rebound led by technology stocks. Intel surged after US President Donald Trump announced a partnership with Apple to design chips in the United States, helping lift the broader semiconductor sector. Nvidia and Micron Technology also advanced strongly. The recovery is consistent with developments in Asia, where South Korea’s Kospi and Japan’s Nikkei both climbed to fresh record highs earlier in the day. Investors continue to embrace the AI growth story even as interest rate expectations move higher.

That leaves markets balancing two powerful but competing forces. On one side is a Fed that has become more concerned about inflation persistence and appears willing to tighten policy further if necessary. On the other is an AI-driven investment boom that continues to support equity valuations and broader risk appetite. The result may not be enough to derail the Dollar’s rally, but it could make the advance more uneven as capital continues flowing into growth-oriented sectors and equity markets.

Elsewhere, central bank developments offered mixed support for major currencies. Sterling weakened after the Bank of England delivered a hawkish hold that failed to satisfy bulls looking for clearer signals of another rate hike. While Huw Pill and Megan Greene voted for an increase, many economists noted little evidence that the Bank’s centrist members are moving toward tighter policy. Some analysts also argue that falling energy prices following the U.S.-Iran agreement reduce the likelihood of a BoE hike later this year, making an extended pause the more likely outcome.

Meanwhile, the Swiss National Bank reinforced its dovish stance after holding rates at 0.00%. SNB Chair Martin Schlegel emphasized that “our readiness to intervene in the FX market is increased” if necessary, adding that a “strong and rapid appreciation of the Swiss franc could endanger price stability in Switzerland.” The comments highlighted the contrast between a Fed increasingly focused on inflation persistence and an SNB still more concerned about excessive currency strength.

For the week so far, the Dollar remains the runaway leader among major currencies. Yen is holding second place despite falling to a two-year low against the greenback, reflecting broader strength against other currencies. Aussie ranks third, supported by resilient risk sentiment and AI-related optimism. At the other end of the table, Sterling is the weakest performer as markets question whether the BoE will ultimately follow through with another hike. Kiwi and Loonie round out the bottom three, while Euro and Swiss Franc remain stuck in the middle of the pack.

BoE Holds at 3.75%, But 7-2 Vote Keeps Rate Hike Risk Alive

A 7-2 vote is not a comfortable hold. The Bank of England left rates unchanged, but the split shows a meaningful hawkish faction remains active within the MPC. Read More.

SNB Holds at 0%, Sees Energy-Driven Inflation as Temporary

Higher inflation didn’t change the SNB’s view. Officials see the recent rise in prices as largely energy-driven and temporary, leaving policy firmly on hold. The SNB’s biggest concern isn’t inflation. It’s the franc. Policymakers left rates at 0% and reiterated their readiness to intervene if Swiss currency strength threatens price stability. Read More.

Gold and Silver Rejected Key Resistance, 4,000 and 60 at Risk If Fed Hikes Twice

Markets are focused on one Fed hike. Precious metals should be watching for two. Six policymakers already project two or more increases, a scenario that could put Gold 4000 and Silver 60 under growing pressure. Read More.

USD/JPY Hits Two-Year High as Hawkish Fed Revives Rate Hike Bets

A hawkish Fed, rising US rate expectations drives USD/JPY higher. The pair is now challenging levels not seen in two years. Warsh’s first meeting changed the conversation. A hawkish dot plot, higher inflation projections and an unwillingness to rule out future hikes have reignited expectations for tighter Fed policy. Read More.

US Initial Jobless Claims Beat Expectations, Continuing Claims Edge Higher

Layoffs remain low, but finding a new job is getting harder. Initial claims fell below expectations, yet continuing claims continued to trend higher, pointing to a slower labor market beneath the surface. Read More.

UK Jobs Growth Stalls as Claimant Count Jumps, Wage Pressures Ease Slightly

The claimant count jumped. The unemployment rate fell. Britain’s latest labor market report delivered conflicting signals, leaving policymakers with little reason to change course. Read More.

New Zealand Q1 GDP Meets Forecasts at 0.8% as Manufacturing Drives Growth

New Zealand’s recovery is gaining traction. GDP growth accelerated to 0.8% in the first quarter, with manufacturing, business services and wholesale trade driving the expansion. Read More.

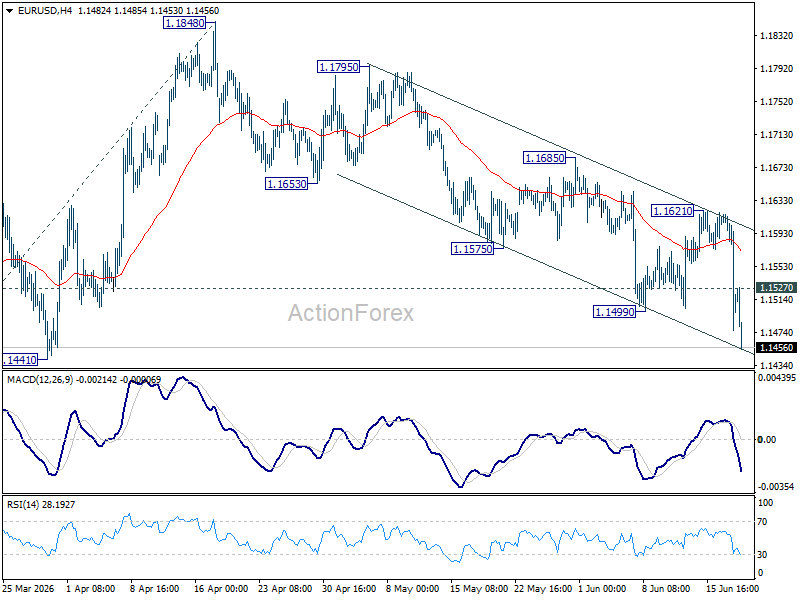

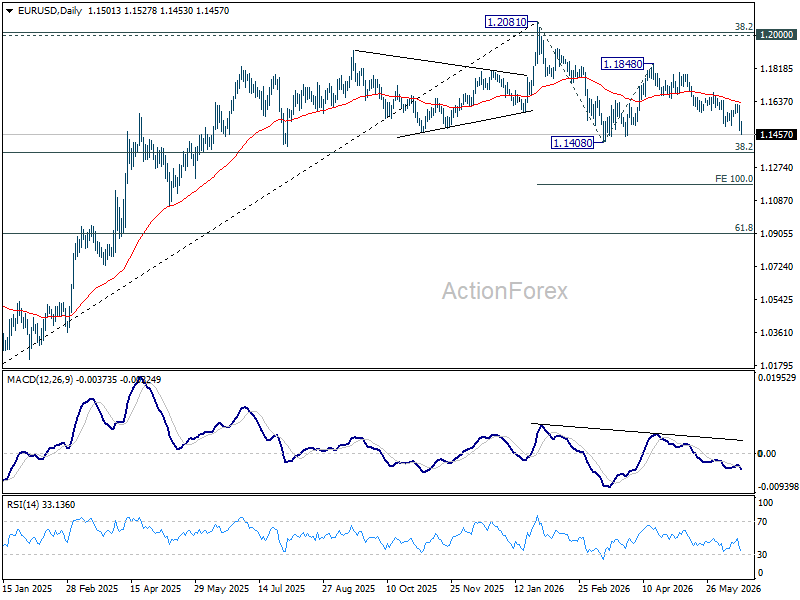

EUR/USD Daily Outlook

Intraday bias in EUR/USD is back on the downside with break of 1.1499 support. Further fall should be seen to retest 1.1408 low. Firm break there will resume whole decline form 1.1408 to 100% projection of 1.2081 to 1.1408 from 1.1848 at 1.1175. On the upside, above 1.15247 minor resistance will turn intraday bias neutral again first. However, outlook will remain mildly bearish as long as 1.1621 resistance holds, in case of recovery.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1547). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

{kind=link}

{kind=link}