Australia’s latest economic data were supposed to answer one question: has April’s oil shock weakened the economy enough to keep the Reserve Bank of Australia comfortably on hold?

Instead, they delivered a more complicated answer.

AUD/USD has begun to stabilize after a sharp selloff this week, reflecting a data flow that was mixed at first glance but surprisingly consistent underneath. Headline inflation eased, yet core inflation accelerated. Employment rebounded, even if the quality of hiring softened. Most importantly, household spending bounced back strongly, suggesting consumers have largely absorbed the hit from higher energy prices.

Inflation remains the biggest challenge for policymakers. Annual CPI slowed to 4.0% from 4.2%, helped by lower fuel prices. But that is unlikely to provide much comfort to the RBA. Its preferred trimmed mean inflation measure accelerated to 3.6%, while services inflation picked up to 3.7%, showing that domestic price pressures remain stubborn despite improving energy costs. In other words, imported inflation may be easing, but home-grown inflation is proving harder to tame.

The labor market offered a similarly balanced picture. Employment rose by a stronger-than-expected 40.3k and unemployment edged down to 4.4%, but April’s job losses were revised substantially deeper. Full-time employment increased by only 5k, with most hiring concentrated in part-time work, while hours worked declined -1.1% over the month. The report does not point to an overheating jobs market, but neither does it suggest labor conditions are deteriorating rapidly.

Perhaps the most significant report received the least attention. Household spending rebounded 1.3% mom in May after April’s -1.7% mom decline, with all nine spending categories recording gains. That broad-based recovery indicates domestic demand has regained much of the ground lost during the oil-price shock, raising the possibility that stronger consumption could keep underlying inflation elevated over coming months.

The combined message from this week’s releases is that the RBA’s job has become more difficult rather than easier. A softer headline inflation reading alone might have strengthened the case for staying on hold. But resilient demand, sticky core inflation and a labor market that continues to hold together mean another rate hike in August remains very much in play, though not confirmed

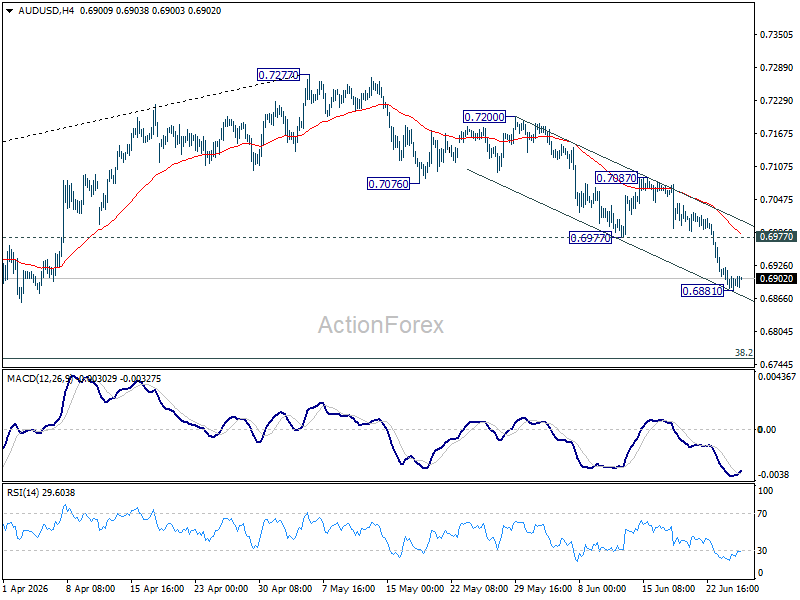

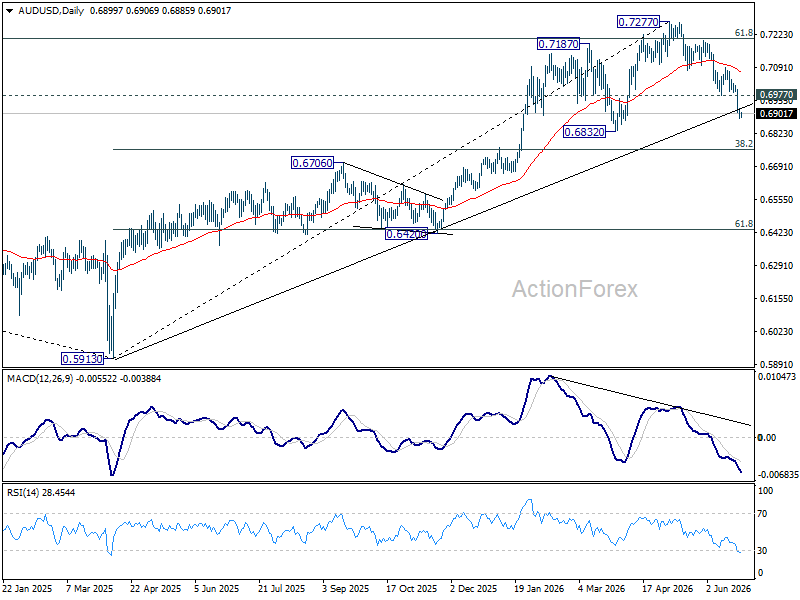

Technically, AUD/USD may have established a temporary low at 0.6881, allowing for a period of consolidation. However, any recovery is likely to remain capped below 0.6977, now acting as resistance. The broader decline from 0.7277 is still viewed as a correction of the rally from the 2025 low at 0.5913, with scope for a deeper fall toward the 38.2% retracement at 0.6756 before a more sustainable bottom is formed.

{kind=link}