- Dollar strength dominates markets, as the hawkish Fed overshadows geopolitics and lower oil prices.

- NFP week could drive September Fed hike expectations and boost market volatility.

- The euro lacks fresh bullish catalysts, all eyes on the preliminary inflation report and the ECB Forum.

- Peripheral currencies seek a reprieve; yen intervention looms while the pound awaits the new PM.

Dollar reaction surprises investors

The end of the Middle East conflict and the steps made so far towards securing a comprehensive deal over the next five weeks – with oil prices dropping aggressively but maintaining a small risk premium – has allowed investors to focus elsewhere.

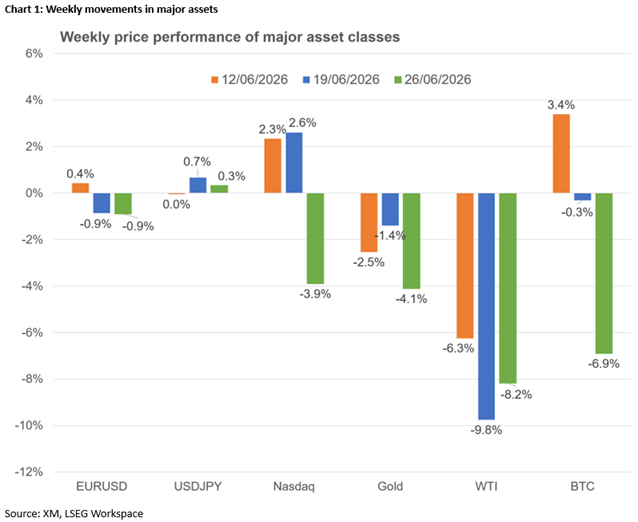

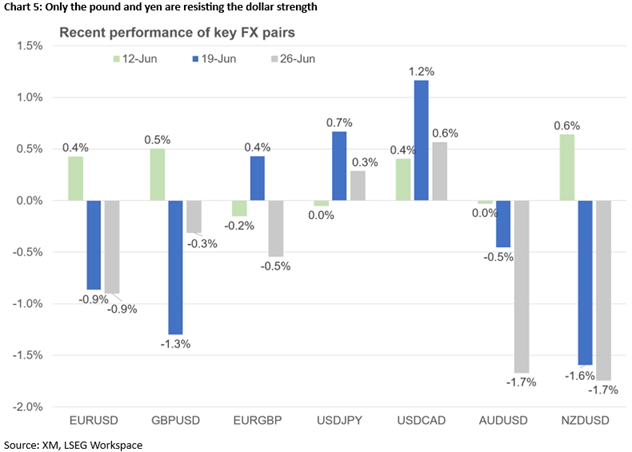

Contrary to expectations, the greenback has been the main protagonist lately. The dollar index has posted its best two-week performance since mid-March – at the height of the US-Iran-Israel conflict – outperforming every major currency this week, with euro/dollar dropping to a fresh one-year low.

The recent Fed meeting, with Chair Warsh bashing forward guidance and announcing committees to revamp the Fed, was hawkish enough to prompt a jump in rate hike expectations. There is currently a 72% chance of a 25bps rate hike in September, with next week’s US data potentially upsetting these expectations.

The prospects of higher funding costs and the lingering valuation concerns have put equities on the back foot, with the mighty technology stocks bearing the brunt. Interestingly, equity bulls have yet to treat the current weakness as an opportunity to enter long positions, confirming market angst.

While US Treasury yields dropped this week, mostly benefiting from the muted risk-off sentiment, but yield spreads remain favourable for the dollar, could the greenback maintain its current trajectory?

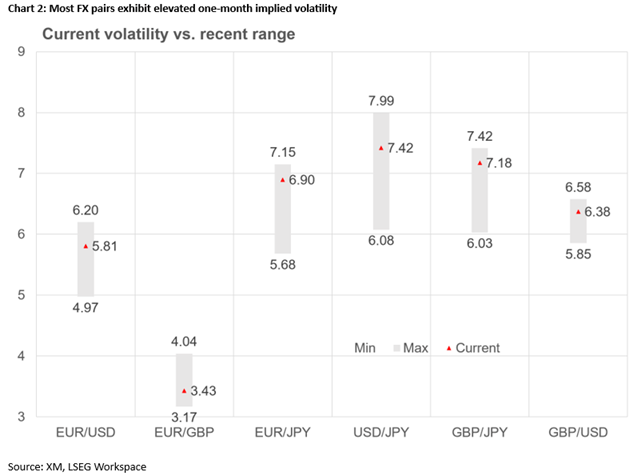

A data-heavy week is upon us. Combined with the holiday-shortened week in the US, due to the July 3 bank holiday, and the month-end, quarter-end and half-year-end rebalancing flows, volatility could rise aggressively, influencing traders’ behaviour.

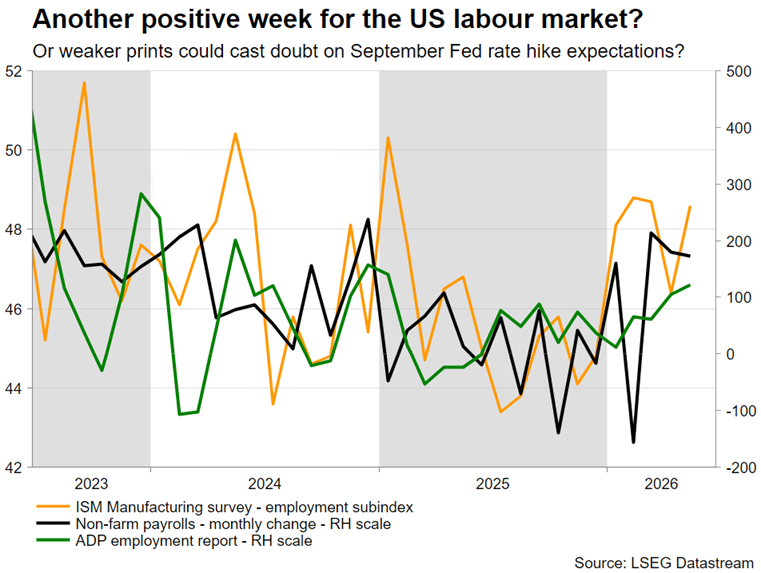

All eyes are on Thursday’s NFP release

Tuesday’s CB Consumer Confidence index could continue its upward trend, confirming the positive state of the US consumer, while the prices paid subindex of Wednesday’s ISM Manufacturing PMI should offer valuable insight into inflation pressures.

Tuesday’s JOLTS report, the Challenger Job Cuts and the ADP employment reports on Wednesday could prove the best appetizer for Thursday’s nonfarm payroll report. As already noted, Friday’s data releases have been transferred to Thursday, July 2, thus shrinking the trading session.

Following a decent run of job-related data, with the three-month NFP average rising to 188k that is the highest rate since Q1-2024, most Fed members believe that the jobs market is healthy without fuelling inflation. A series of significant downside data surprises might change their minds, upsetting rate hike expectations.

Notably, the dollar seems to be benefiting under both risk-on and risk-off scenarios at this stage. Lower chances of a September hike could boost equity indices and attract fresh inflows into US dominated funds seeking exposure in the technology sector. On the flip side, strong US data would further support Fed rate hike expectations, benefiting the dollar.

Interestingly, investors are trying to adjust to the reduced Fedspeak, with many wondering if Warsh has imposed a limit on public appearances or whether Fed members are just careful not to alienate Warsh with their commentary.

The Euro seeks a bullish catalyst

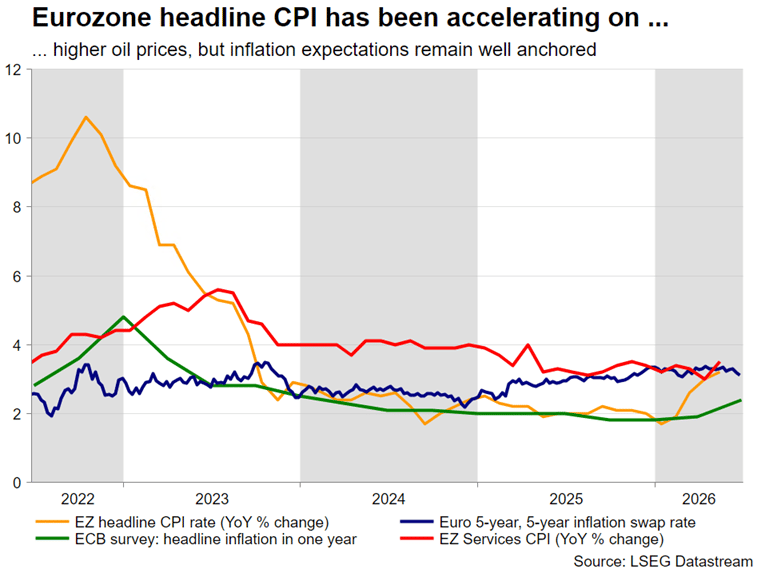

The euro remains under pressure, as the lack of tailwinds is quite evident. Amidst a decent run of economic data, the impact of hawkish monetary policy has probably reached its limit. Markets are assigning an 80% chance of a September hike, but hawkish commentary has had a muted impact on the euro, as seen in this week’s performance against both the dollar and the pound.

Should Wednesday’s preliminary inflation report post a sizeable upside surprise, ECB hawks might increase their pressure for a July rate hike. However, with oil prices dropping around 20% in June, there is a strong probability of a significant downside surprise, suppressing July hike expectations. In this case, the euro could experience further weakness, even against the pound.

A plethora of central bankers, including President Lagarde, will be on the wires next week, as the annual ECB Forum in Sintra, Portugal is taking place from June 29 to July 1. Rumours about her early departure have receded lately, but the discussion is not over.

The Pound and Yen will remain the spotlight for different reasons

Both the pound and gilts have welcomed that other candidates decided to step aside, opening the door for Burnham, who is now expected to take office in mid-July.

This development allows the BoE to remain focused on restoring price stability, with the split between doves and hawks remaining wide, but that might change when the new PM details his economic plan. Nationalizations, higher public spending and tax increases might not be welcomed by investors, with the BoE potentially forced to focus on financial stability rather than fighting elevated inflation.

Meanwhile, the recent BoJ hike and the continued hawkish rhetoric have not reversed the yen’s fate, with investors continuing to ignore the repeated verbal interventions and keeping dollar/yen above 160.

The clock is ticking down to the next intervention, but is Japan waiting for the greenlight from the US? Is PM Takaichi resisting an intervention and opposing further BoJ hikes to keep the stock market rising? Is the Finance Ministry waiting for the right date to intervene? The real reason might be a combination of the above, but with the July 3 US bank holiday coming up, questions could be answered soon.

Aussie and loonie crave a risk-on reaction – Gold suffering to continue

Peripheral currencies have been suffering from the current dollar rally and the mixed risk appetite. The aussie will be looking at the RBA minutes and strong Chinese PMI data to support rate hike expectations, while Canadian data could remain bleak, keeping the loonie under pressure and adding to the 3% losses posted over the past four weeks.

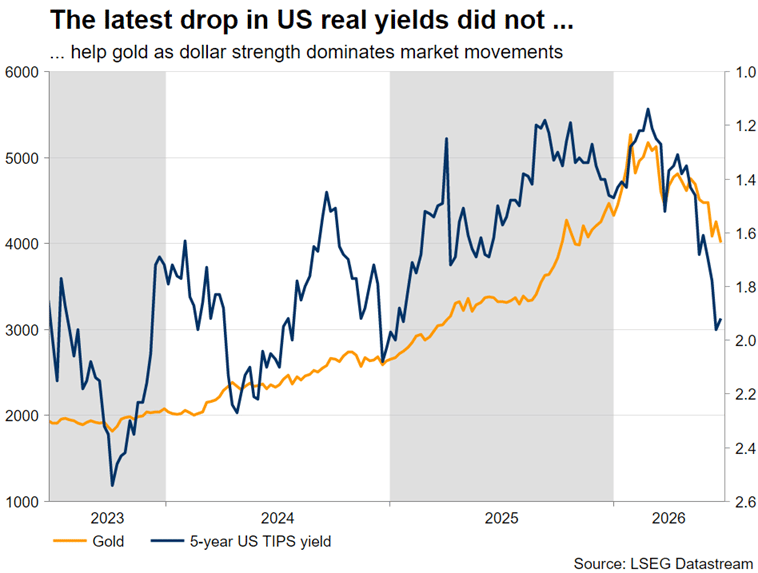

Finally, the $4,000 level is proving tougher to crack than bears expected. A move towards $4,400 is needed to reverse the current bearish sentiment, but this looks far-fetched until an acute equity market correction occurs, which would initially benefit gold, and weak US data push out Fed hike expectations.

{kind=link}