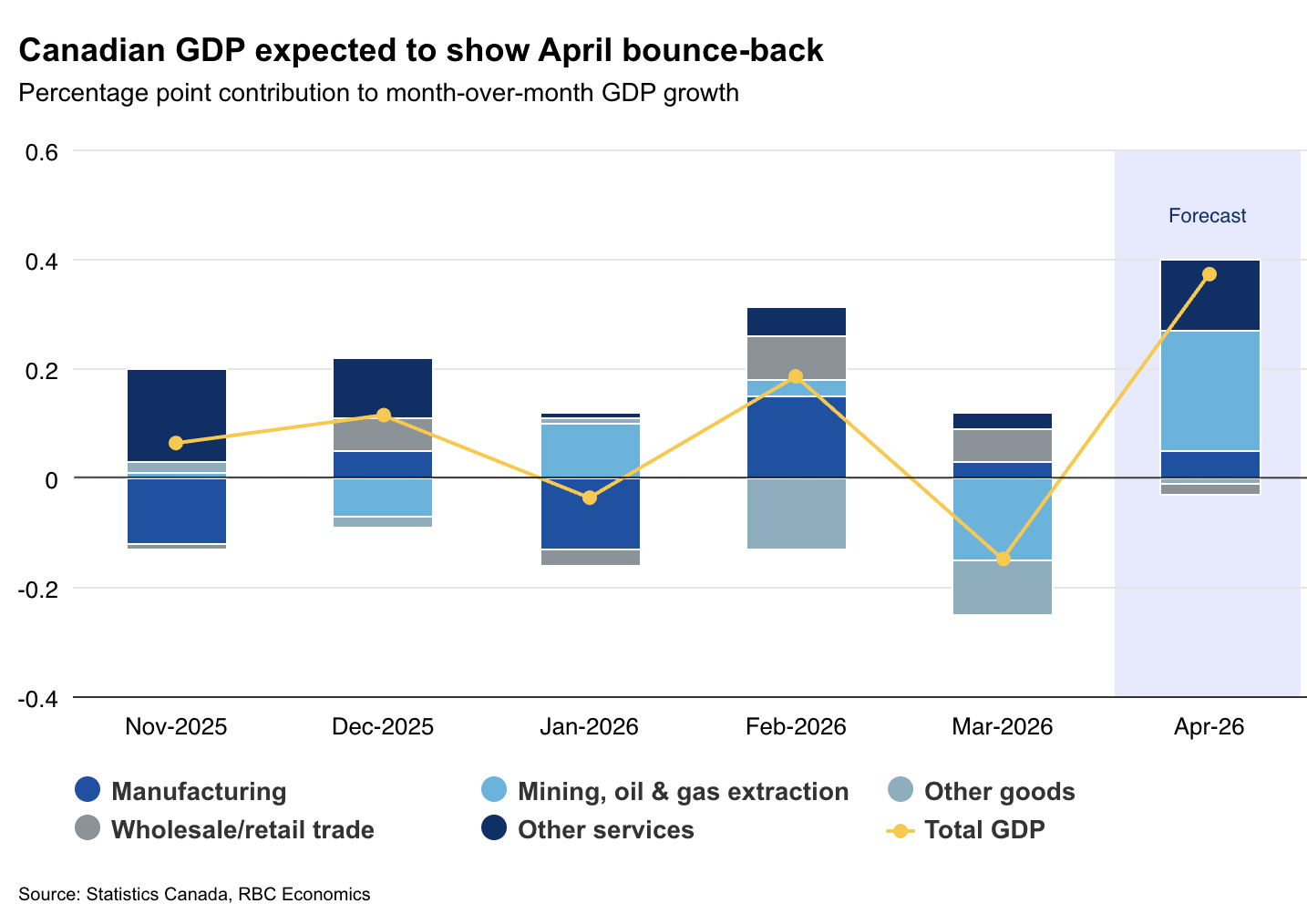

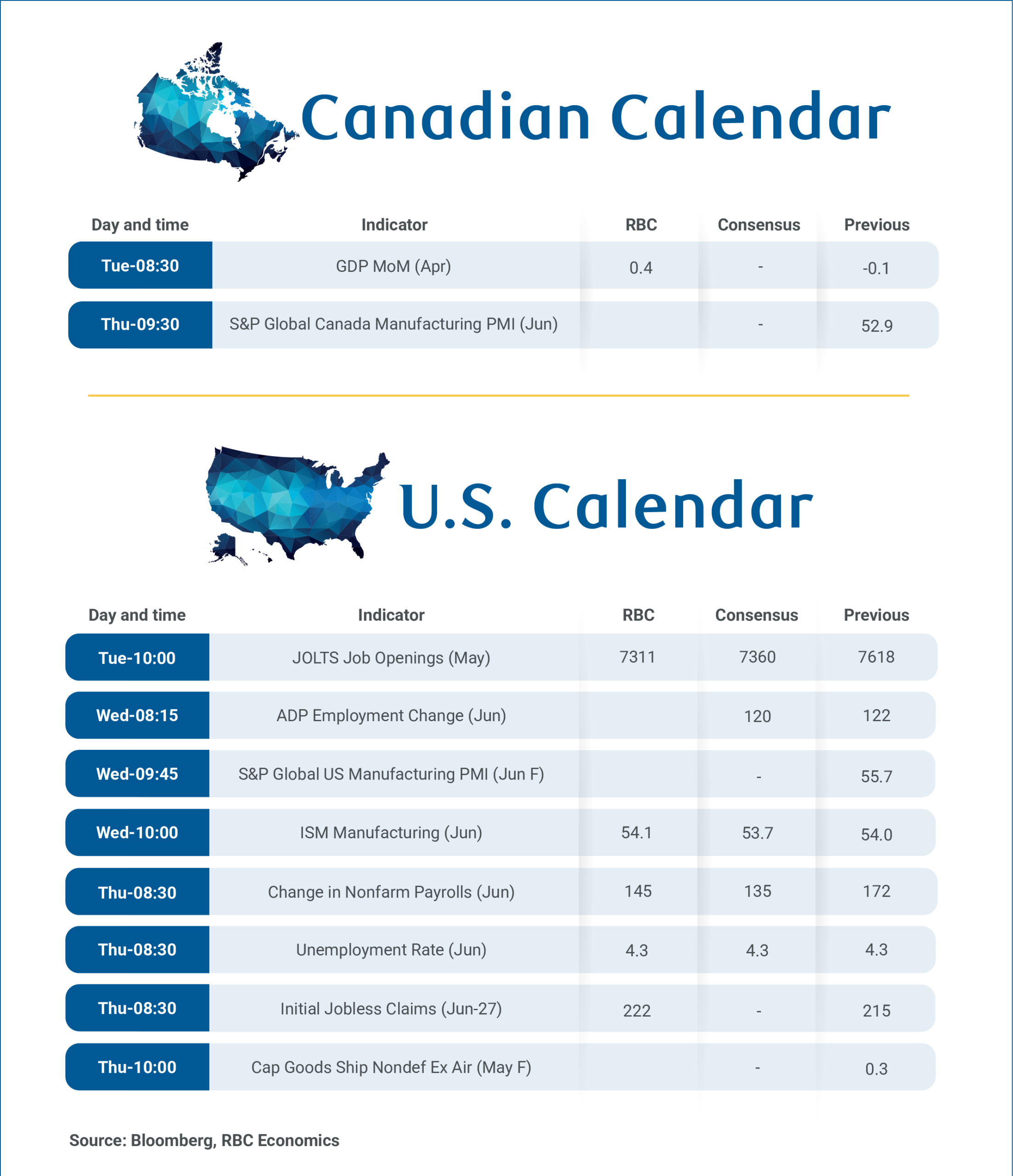

We expect real gross domestic product in Canada to show a 0.4% increase in April on Tuesday after stagnating for two straight quarters.

That would be consistent with Statistics Canada’s preliminary estimate a month ago, although we expect it was led by a relatively narrow rebound in mining, oil and gas extraction.

Early data is pointing to a significant increase in non-conventional oil extraction and oil drilling in April. Adding in a pickup in manufacturing GDP, goods-producing sectors overall likely expanded by 1%.

Service sector GDP is expected to have gained 0.1% with weaker wholesales (-0.3%), and flat retail GDP offset by growth in other industries including real estate and rentals after Canadian home resales ticked higher (seasonally adjusted) in April for the first time since October 2025.

Preliminary monthly GDP data has been highly revision-prone, but overall, data has been pointing to a firming in economic activity in Q2 with early May data also looking broadly better..

Labour market data in May firmed, and the housing market continued to show signs of thawing with resales up 5.1% from April (the largest increase since October 2024).

StatCan’s advanced indicators also pointed to rising nominal retail and manufacturing sales in May, the former consistent with our card transactions tracker suggesting resilient, albeit slightly weaker spending growth.

And, global oil prices have moved lower in recent weeks. If sustained, those declines will help to restore some household purchasing power eroded by higher fuel costs, while also limiting risks of inflation spreading beyond energy prices.

BoC to stay on hold in 2026

The combination of signs of firming Q2 GDP growth, and easing inflation pressures should help to validate the Bank of Canada’s call to not overreact to temporarily higher oil prices or mechanically softer economic data. With growth picking up in Q2 and core inflation remaining subdued, we continue to expect no change in interest rates from the central bank in 2026.

South of the border, the U.S. Federal Reserve tilted decidedly hawkish in their latest meeting—first under new Chair Kevin Warsh. Half of the FOMC (excluding Warsh) expected at least one rate hike in 2026, prompted by concerns over sticky-to-accelerating core inflation readings while labour markets remain robust.

On Thursday, we expect May’s U.S. employment report to broadly reinforce that view with a 145,000 payrolls’ gain, alongside a steadily low 4.3% unemployment rate.

{kind=link}