Gold found its footing above $4,000 after June’s disappointing US payrolls report triggered broad-based Dollar selling and eased expectations for a near-term Fed rate hike. But the rebound is already losing momentum this week. The reason is simple: while payrolls surprised on the downside, the Fed’s bigger concern is not employment—it’s inflation.

The post-NFP rally illustrated that tension perfectly. Dollar Index slipped to a two-week low near 100.75 after the jobs report, allowing Gold to climb back above $4,200. Yet the move quickly stalled. By Monday, the Dollar was already recovering. Rather than extending higher, Gold struggled to capitalize on last week’s softer labor data, suggesting the market has already moved beyond the initial payroll-driven reaction.

The bigger story lies in the Fed’s June policy projections. Two weeks before the payroll report, policymakers delivered a meaningful hawkish shift by raising the median 2026 federal funds rate projection from 3.4% to 3.8%. That was more than a routine adjustment. It transformed the committee’s central outlook from one additional rate cut to one additional hike. Nine officials now expect rates to rise further, eight see policy staying unchanged, and only one continues to project another cut.

Against that backdrop, one weak employment report was never likely to overturn the Fed’s broader inflation narrative. Markets have delayed expectations for the next hike from September toward December, but they have not abandoned the idea altogether. As long as investors continue to believe the next policy move is more likely to be another hike than a cut, Gold will struggle to build a sustained rally.

That is why this week’s ISM Services PMI and Wednesday’s FOMC minutes may have only limited influence. They can shape short-term sentiment, but neither is likely to change the market’s broader view of Fed policy. The more important event arrives on July 14, when the June CPI report will provide the clearest evidence yet of whether the Fed’s inflation concerns are justified.

The stakes are unusually high. The June Summary of Economic Projections lifted the Fed’s forecasts for 2026 headline and core PCE inflation sharply higher, while May CPI had already accelerated to 4.2%. If June inflation surprises to the upside, policymakers will have fresh evidence that inflation pressures are proving more persistent than hoped. That would reinforce expectations for another rate hike, supporting the Dollar and Treasury yields while limiting Gold’s upside. On the other hand, a softer CPI report would undermine the Fed’s inflation thesis and could finally give Gold the catalyst needed to break convincingly above recent resistance.

Until that verdict arrives, Gold may struggle to escape its current range. The market appears caught between two competing narratives: a labor market that is gradually cooling and a central bank that is still more worried about inflation than growth. Without clearer evidence that inflation is easing, the recent rebound risks becoming little more than a pause within a broader decline.

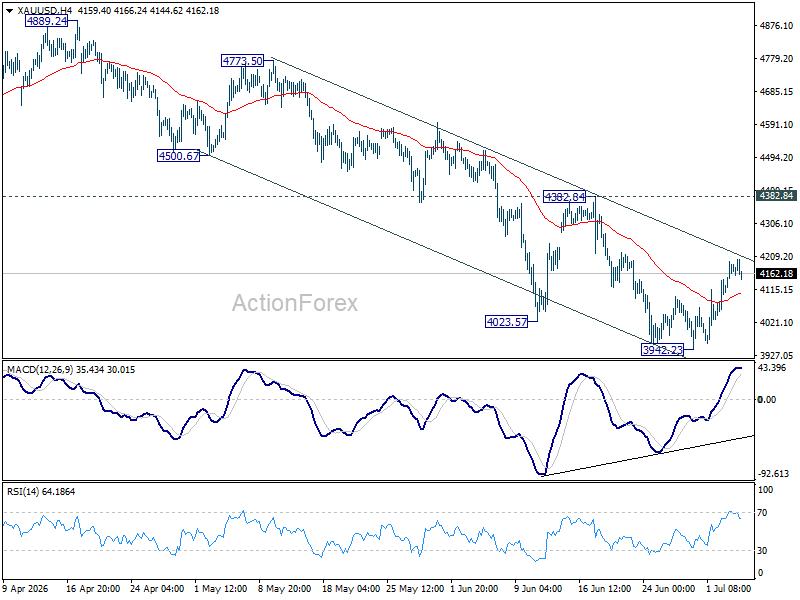

Technically, Gold appears to have established a short-term floor at 3942.23, supported by bullish convergence on 4H MACD. Additional consolidation is possible in the near term, but the broader outlook remains bearish while 4,382.84 caps the recovery. Failure there would keep the downtrend from 5,598.38 intact and maintain the risk of another decline through 3,942.23 toward the 50% retracement of 1,614.60 to 5,998.38 at 3,606.49.

Even so, the daily chart also shows bullish convergence developing on the MACD, suggesting downside momentum is gradually fading. Decisive break above 4382.84, followed by sustained trading above the 55 D EMA, now at 4364.94, would provide the first meaningful evidence that a medium-term trend reversal is underway, opening the way toward the descending trend line near 4,630.

{kind=link}