- US CPI report and Fed Chair Warsh’s dual testimonies in the spotlight.

- Headline inflation is expected to ease, but will the deceleration surprise?

- Investors to monitor Warsh’s rhetoric for clues about a September rate hike.

- Euro/dollar could revisit recent lows if CPI surprise on the upside and Warsh appears hawkish.

Dollar in demand

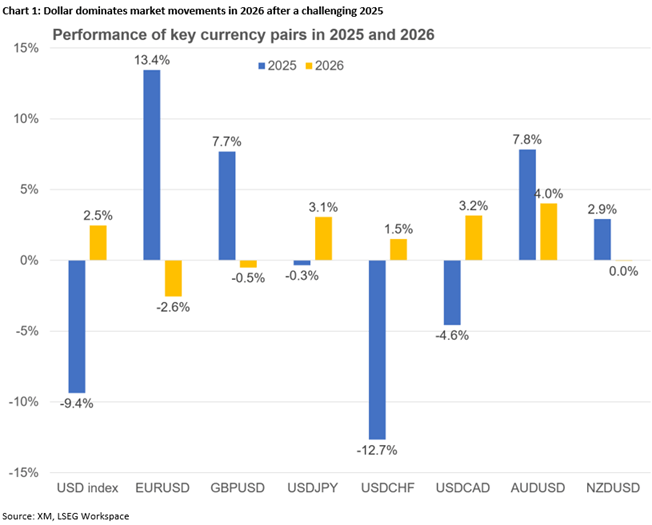

The US dollar has been one of the main protagonists of 2026, with the arrival of newcomer Fed Chair Warsh adding to the plethora of bullish catalysts. The dollar index climbed in late June to the highest level since May 2025, when the greenback was trying to recover from the reciprocal tariff announcements.

Busy data calendar – CPI in the spotlight

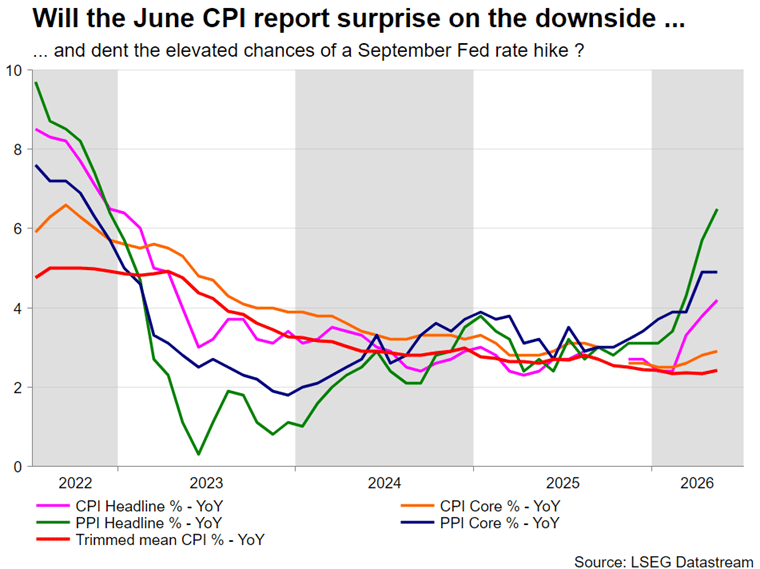

Next week’s calendar will be exceptionally busy with a series of data prints and the first Humphrey-Hawkins testimony from Fed Chair Warsh. Specifically, the last CPI report ahead of the July 29 Fed meeting will be released on Tuesday at 12:30 GMT.

Following the solid May print, given the 20% monthly drop in oil prices in June and despite the World Cup boosting spending, there is a strong probability of the headline CPI decelerating below the 4% level again, largely erasing the May jump. Similarly, core CPI should also follow suit with a smaller drop. Both are expected to remain above the 2% inflation target.

PPI and retail sales data releases will follow on Wednesday and Thursday respectively, while Friday’s University of Michigan Consumer Sentiment index will complete the picture. Following the strong PPI report from China, chances of another solid PPI print cannot be underestimated, while both retail sales and UoM survey could climb on the back of the lower energy prices and the World Cup impact, especially as these data releases cover a period when the US soccer team was advancing in the tournament.

Warsh’s testimony stands out

Fed Chair Warsh will appear before the House Financial Services Committee on Tuesday and before the Senate Banking Committee on Wednesday. Both have a starting time of 14:00 GMT with the latter usually being less market-moving.

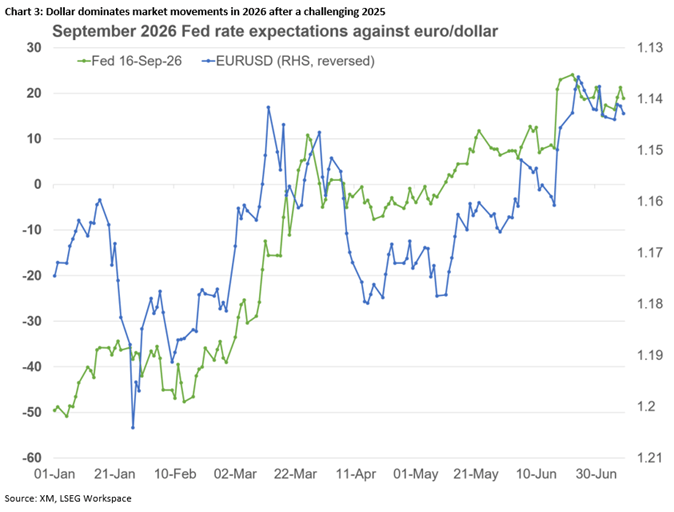

Since taking office, Fed rate hike expectations have jumped, with Warsh’s post-FOMC meeting press conference, the panel discussion at the ECB Forum in Sintra, Portugal and the June 17 meeting minutes justifying these hawkish expectations.

Warsh has made it quite clear that he dislikes forward guidance in normal periods and has emphasized the Committee’s unease about inflation running well above target, thus highlighting that there is work to be done on price stability. The minutes left little doubt about the hawks holding the upper hand in the FOMC.

Warsh is expected to move along these lines in his dual testimonies, potentially also highlighting the failures of his predecessor to get inflation under control and claiming that the Fed’s stance has been distorted by an inflated balance sheet and non-rate measures.

Barring a major hawkish surprise that puts a July rate hike on the table, investors will closely watch for any clues about the expected September rate hike and whether the recent soft labour market data has alarmed Warsh. If Warsh appears confident about the jobs market, expectations of a September hike could strengthen.

Dollar stabilizes after strong gains

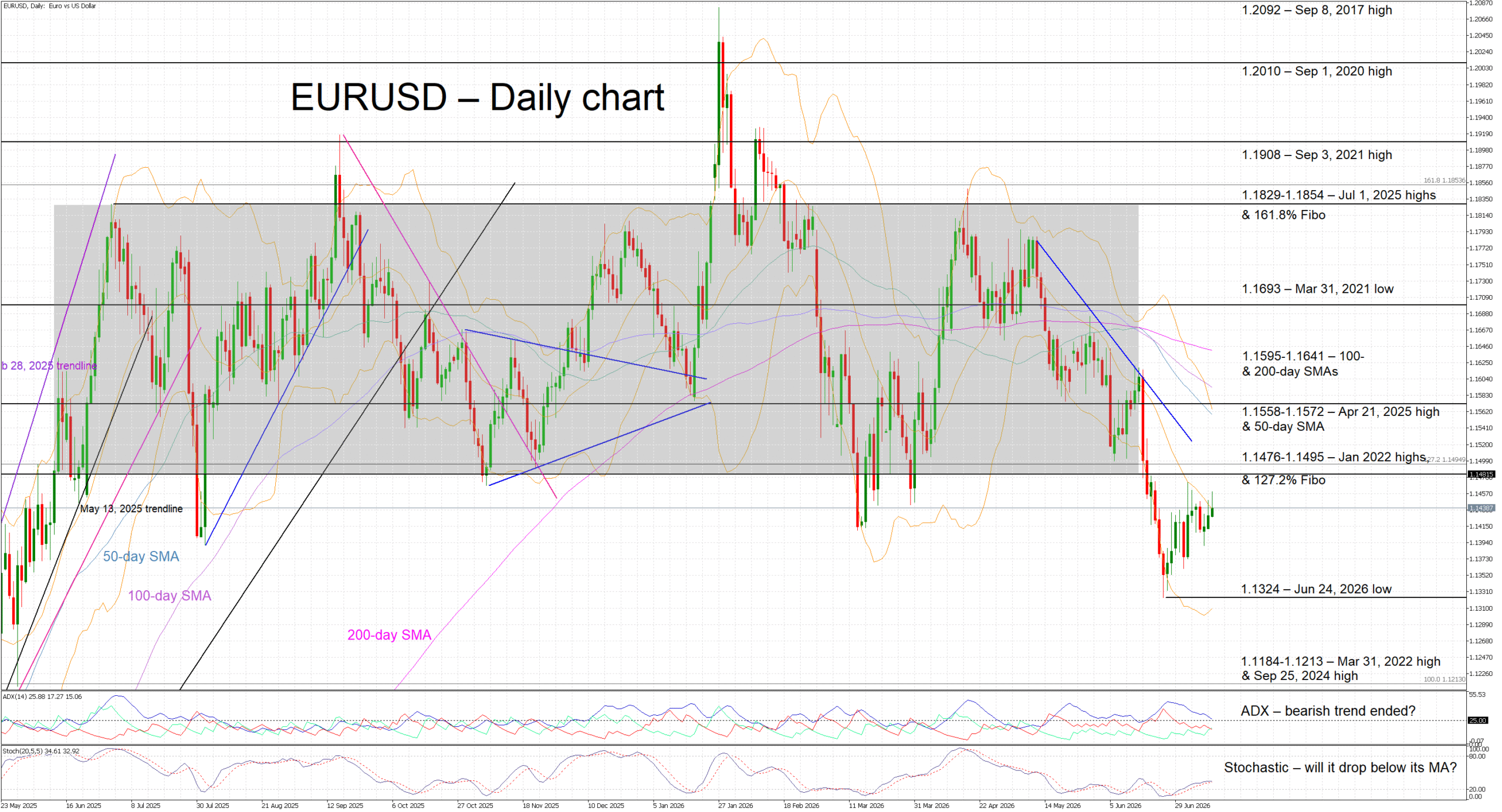

Following the June FOMC meeting, euro/dollar broke the one-year-long wide 1.1470-1.1829 range, dropping to the lowest level since May 30, 2025. With the ECB’s hawkish stance exerting little upside influence on this pair and the eurozone economy struggling, the greenback dictates movements.

A softer inflation print on Tuesday and Warsh largely repeating his recent comments could somewhat dent the dollar’s appeal. However, expectations for a September hike will most likely remain well supported. A test of the lower boundary of the recent range at 1.1470 could materialize but such a move might prove short-lived.

On the other hand, an inflation report that fails to show significant deceleration and a hawkish Warsh – for example, by repeating the Fed’s commitment to price stability while dismissing job market concerns – could push euro/dollar towards the recent trough of 1.1324.

{kind=link}