After much volatility this week, Yen and Dollar are staying as the weakest one for the week. Receding concerns over US-China trade war boosted risk appetite in the US and Asia in general. It seems that Trump’s administration and Republicans are feeling heavy pressure from business to stop any trade tension escalation, even though Trump may like the opposite way. As long as Trump refrain from starting the new 25% tariff on USD 200B in Chinese goods, Dollar and Yen could stay soft for a while. Focus will turn to US retail sales today first.

On the other hand, Sterling is so far the strongest for the week. Looking through all the noises, it’s rather clear that both Prime Minister Theresa May’s government and the EU want to make a deal. The biggest risks actually come from within the Conservative Party. The Pound will likely be supported even though it will remain headline sensitive.

In other markets, DOW closed up 0.57% overnight at 26145.99. S&P 500 gained 0.53% to 2904.18. NASDAQ added 0.75% to 8013.71. S&P 500 has realistic chance of challenging record high at 2016.50 soon. Treasury yields were mixed with 10 year yield closed flat at 2.963. 3.000 level is so close yet so far. Asian markets trade higher today with Nikkei up 0.93% at the time of writing. Hong Hong HSI is up 0.81%. Singapore Strait Times up 0.71%. However, China Shanghai SSE is fluctuating in gain and loss, down -0.13% currently. Gold failed 1214.30 resistance yesterday but may have another take on this level if Dollar suffers another round of selling today.

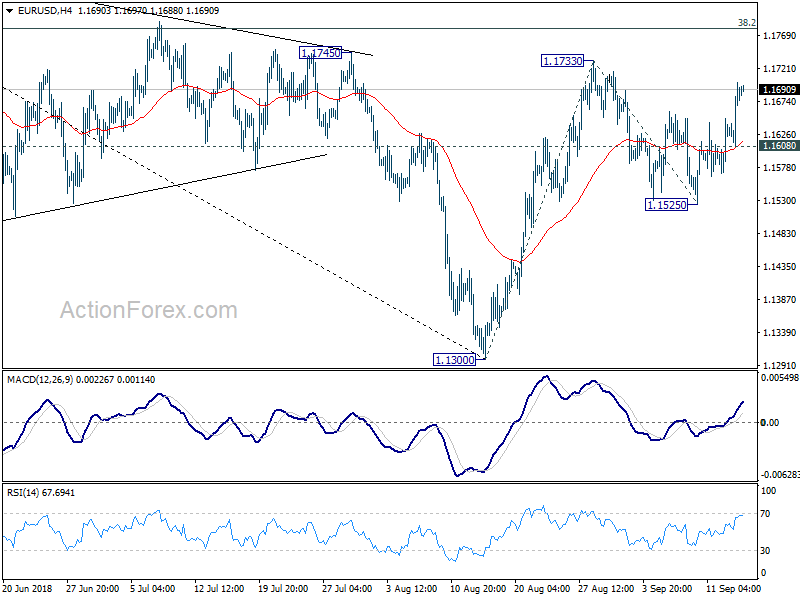

Technically, GBP/USD took the lead in rise resumption earlier this week. But EUR/USD is held below 1.1733. USD/CHF is kept above 0.9640. These two levels will now be in focus today. USD/JPY broke 111.82 resistance yesterday to resume the rebound from 109.76. Further rise is expected for 113.17 resistance. But as both Dollar and Yen are soft, the process could be “gradual”.

Atlanta Fed Bostic: Rate hikes to continue over next few quarters, but unsure on Q4

Atlanta Fed President Raphael Bostic said in a speech yesterday that the economy is “doing well and standing on its own”. He supported monetary to move towards a neutral stance. And that means “a gradual increase in nominal interest rates over the next handful of quarters.” However, later he clarified that there is still “some uncertainty” to whether US is “really at full employment”. If there is “not a risk of overheating then we have the possibility to be more patient.”

Bostic is taking a “wait and see” approach to the fourth hike in 2018 in December. That is, to several rate hikes in the coming quarters doesn’t mean rate hikes in every quarter. While it may sounds a bit confusing, his comments have been consistent. Bostic is one of those who are more cautiously on the outlook. In particular, just a few weeks ago, he vowed not to vote for anything that knowingly inverts yield curve.

On trade tensions, Bostic said “an uncertain outlook can cause firms to delay investments while they wait to see how the situation unfolds. Such a development could grow to have macroeconomic ramifications the longer the uncertainty remains.” But he also noted that a recent survey shows trade war fears have had “only a small negative effect on US business investment so far.”

BoE Carney: House price could fall 25-35% on no-deal Brexit

BoE Governor Mark Carney gave some “chilling” warnings in Prime Minister Theresa May’s cabinet meeting on no-deal Brexit preparation yesterday. There he compared a disorderly effort to 2008 financial prices. And more importantly, BoE wouldn’t be able to avert the crisis by cutting interest rates. Inflation and unemployment are expected to surge according to Carney’s expectation. And, in the worst case scenario, house price could fall be 25-35% over three years. On the other hand, Carney noted that if a deal is struck based on May’s Chequers plan, the economy could overshoot current forecasts as it’s an outcome that’s better than BoE assumed.

However, it should be noted that Carney has been constantly accused by Brexiteers as being part of the “Remain” camp, together with Chancellor of Exchequer Philip Hammond. And, both have been inaccurate in prediction Brexit economic consequences. Leader of the Brexit camp European Research Group Jacob Rees-Mogg called Carney “the high priest of Project Fear” last month.

Canada Trudeau: Working on the right NAFTA deal as quickly as we can

September 30 is seen by some as the deadline for completing US-Canada NAFTA negotiation. The legal text has to be produced by October 1 so as for the current Mexican government to sign before leaving office on November 30. But Canadian Prime Minister Justin Trudeau brushed off the deadline.

He said yesterday that “we have seen various deadlines put forward as markers to work for.” And, “we’ll do the work and try and get there as quick as we can, but we’re going to make sure that we’re doing what is necessary to get the right deal for Canadians.”

Also, Trump appeared to have mused about renaming NAFTA to USMC, and said the “C” could be dropped if Canada didn’t sign on. Trudeau said there were “things that we’re working on very seriously, rolling up our sleeves on. I don’t think we’ve spent much time talking about what the name or potential name or renaming could be.”

On the data front

New Zealand Business NZ manufacturing PMI rose to 52 in August up from 51.2. China retail sales grew 9.0% yoy in August, beat expectation of 8.8%. However, industrial production grew 6.1% yoy, below expectation of 6.2% yoy. Fixed assets investment few 5.3% yoy, below expectation of 5.7% yoy.

Looking ahead, Eurozone trade balance will be featured in European session. But main focus will be US retail sales later in the day. US will also release import price index, industrial production, business inventories and U of Michigan consumer sentiment.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1632; (P) 1.1667; (R1) 1.1725; More…..

Intraday bias in EUR/USD remains on the upside for 1.1733 resistance and above. For now, we’d still expect strong resistance from 38.2% retracement of 1.2555 to 1.1300 at 1.1779 to limit upside. On the downside, break of 1.1608 minor support will turn bias to the downside for 1.1525 support. Break will indicate completion of whole rebound from 1.1300. However, firm break of 1.1779 will extend the rise to 100% projection of 1.1300 to 1.1733 from 1.1525 at 1.1958.

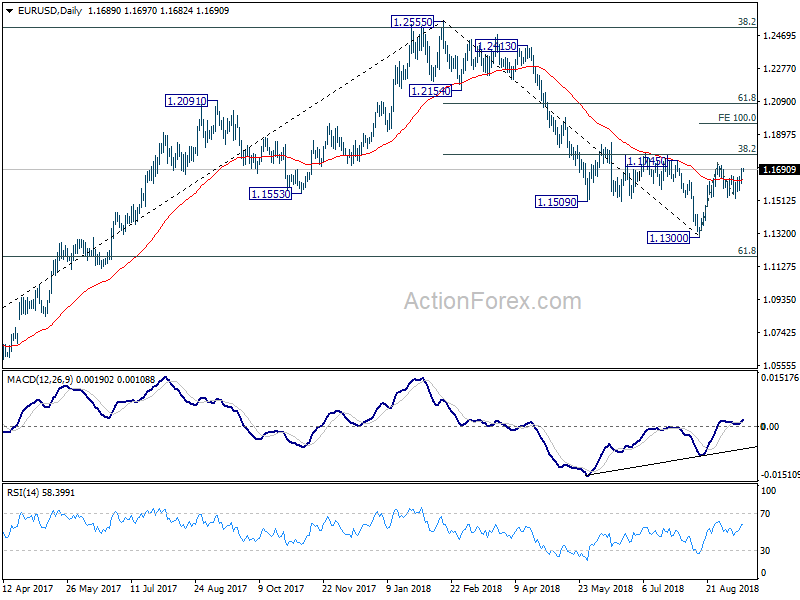

In the bigger picture, a medium term bottom should be in place at 1.1300, on bullish convergence condition in daily MACD and some consolidations would be seen. But still, note that EUR/USD was rejected by 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516. That carries some long term bearish implications. Thus, we’d expect fall from 1.2555 high to resume after consolidation completes. Below 1.1300 should send EUR/USD through 61.8% retracement of 1.0339 to 1.2555 at 1.1186. And, in that case, EUR/USD would head to retest 1.0339 (2017 low).

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | BusinessNZ Manufacturing PMI Aug | 52 | 51.2 | ||

| 2:00 | CNY | Retail Sales Y/Y Aug | 9.00% | 8.80% | 8.80% | |

| 2:00 | CNY | Industrial Production Y/Y Aug | 6.10% | 6.20% | 6.00% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Aug | 5.30% | 5.70% | 5.50% | |

| 4:30 | JPY | Industrial Production M/M Jul F | -0.10% | -0.10% | ||

| 9:00 | EUR | Eurozone Trade Balance (EUR) Jul | 16.3B | 16.7B | ||

| 12:30 | USD | Retail Sales Advance M/M Aug | 0.40% | 0.50% | ||

| 12:30 | USD | Retail Sales Ex Auto M/M Aug | 0.50% | 0.60% | ||

| 12:30 | USD | Import Price Index M/M Aug | -0.20% | 0.00% | ||

| 13:15 | USD | Industrial Production M/M Aug | 0.30% | 0.10% | ||

| 13:15 | USD | Capacity Utilization Aug | 78.40% | 78.10% | ||

| 14:00 | USD | Business Inventories Jul | 0.50% | 0.10% | ||

| 14:00 | USD | U. of Mich. Sentiment Sep P | 96.9 | 96.2 |

{kind=link}