Canadian Dollar surges broadly today as the an agreement, the USMCA is finally reached with the US to replace NAFTA. Riding on the last week’s post GDP rally, the Loonie is enjoying strong bullish momentum. The USMCA news further seal the case for an October BoC rate hike. At the time of writing, Swiss Franc is following as the second strongest, and then Dollar. Yen is the weakest one as Nikkei extends recent rise, followed by Australian Dollar and then Euro.

In other markets, Nikkei is currently up 0.56% at the time of writing,confirming medium term up trend resumption. Singapore Strait Times is up 0.12%. China and Hong Kong are on holiday. WTI crude oil is up 0.31 at 73.56 and it’s on track for 75.27 key resistance level. Gold is back below 1190 as Friday’s recovery faded.

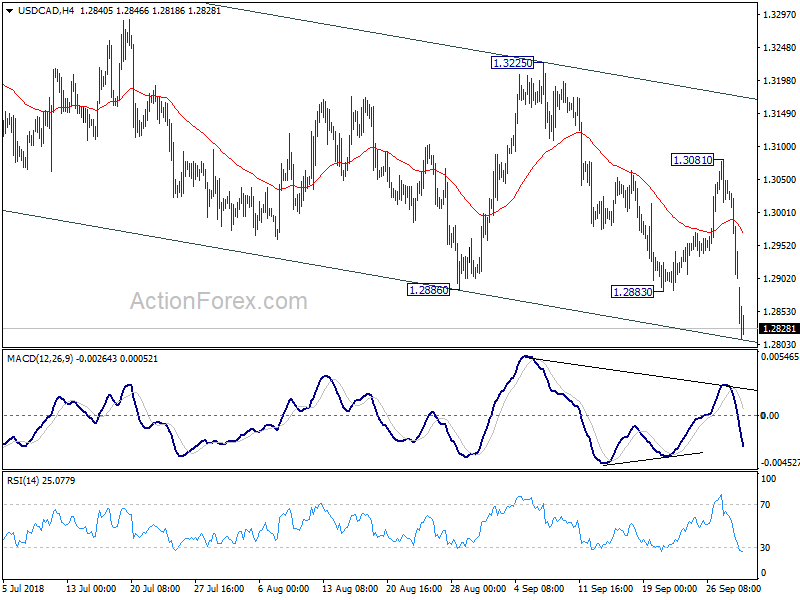

Technically, USD/CAD has taken out 1.2883 key support level today. It’s still a bit early to confirm medium term reversal and that will very much depends on downside momentum ahead. But Canadian Dollar’s strength is rather overwhelming. And it’s rightly so given expectation of October BoC hike, a trade deal with US and strong oil price. EUR/CAD should now be targeting 1.4798 support to confirm resumption of down trend from 1.6151. CAD/JPY’s rally is also on track to test 91.62 key resistance.

USMCA agreed to replace NAFTA, but not everyone’s happy

An agreement is finally reached between the US and Canada after US imposed deadline. The trilateral trade deal is now called the United States-Mexico-Canada Agreement (USMCA), replacing NAFTA. There should be enough time to go through legal work before Mexico’s outgoing President Enrique Pena Nieto leaves office at the end of November.

In short, it’s reported that the agreement would incentivize more auto production in the US. Canada also opens more access for US farmers on its dairy market, and agreed to eliminate the so called Class 7 milk system. There is no substantial change in the chapter 19 dispute resolution mechanism. If the US impose auto tariffs, both Mexcio and Canada will be accommodated in “side letters”. But the deal doesn’t affect the current steel and aluminum tariffs imposed.

While the deal is welcomed by the financial markets, not everyone is happy with it. President of Dairy Farmers of Canada Pierre Lampron warned that “Granting an additional market access of 3.59% to our domestic dairy market, eliminating competitive dairy classes and extraordinary measures to limit our ability to export dairy products will have a dramatic impact not only for dairy farmers but for the whole sector.”

Lampron also criticized` “this has happened, despite assurances that our government would not sign a bad deal for Canadians. We fail to see how this deal can be good for the 220,000 Canadian families that depend on dairy for their livelihood.”

American Federation of Labor and Congress of Industrial Organizations President Richard Trumka also warned that “Our history of witnessing unfair trade deals destroy the lives of working families demands the highest level of scrutiny before receiving our endorsement.” And, “Added protections for working people and some reductions in special privileges for global companies is a good start, but we still don’t know whether this new deal will reverse the outsourcing incentives present in the original NAFTA.”

Japan Tankan large manufacturing dropped to 19 in Q3

Japan Tankan large manufacturing index dropped to 19 in Q3, down from 21 and missed expectation of 22. Large manufacturing outlook dropped to 19, down form 21 and matched expectations.

Large non-manufacturing index dropped to 22, down from 24 and missed expectation of 22. Non-manufacturing outlook rose to 22, up from 21 and beat expectation of 20.

Large all industry capex rose 13.4%, missed expectation of 14.2%.

Japan PMI manufacturing: Q3 average notably lower than Q1 & Q2

Japan PMI manufacturing was finalized at 52.5 in September. The key points are “output growth sustained amid solid demand pressures”, meanwhile, “input delivery times continue to lengthen sharply”, and “business confidence drops further”.

Joe Hayes, Economist at IHS Markit, noted that “growth in the Japanese manufacturing sector was sustained in September, rounding off a fairly robust quarter of expansion”. However, Q3 average at 52.4 was “notably weaker” that Q1 and Q2, “suggesting weaker momentum”. “Slowing input delivery times reportedly weighed on output capabilities”. “The degree of confidence dipped to a 22-month low, with some panellists raising concern towards the demand outlook.”

Australia manufacturing PMI rose to 59.0, two years of uninterrupted expansions

Australian Industry Group Performance of Manufacturing index rose 2.3 to 59.0 in September, indicating faster growth across the sector. It’s now in two years of “uninterrupted expansions”, the longest run since 2005. All seven activity sub-indexes expanded, that is above 50. Five activity sub-indexes accelerated with the new orders sub-index reaching a six-month high.

AiG also noted that “the manufacturing sector has confounded doubters in recent years by lifting employment and production despite the exit of passenger car assembly from Australia. Australia’s manufacturing sector is diverse and comprised of multiple sub-sectors that are continuing to adapt to their operating environment. An improving economy, along with infrastructure, mining, renewable and defence projects continue to support demand for manufacturing products in 2018.”

Also from Australia, TD Securities Inflation rose 0.3% mom in September.

China Caixin PMI manufacturing dropped to 50, downward pressure significant

Released over the weekend, China Caixin PMI manufacturing dropped to 50.0, down from 50.6. That’s the fourth straight monthly drop and an acceleration in the index’s decline. The key points are, “production rises at weakest pace for nearly a year”, “total new business broadly stagnant, as export sales decline at faster rate”, “business confidence slips to nine-month low”.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said in the released that “expansion across the manufacturing sector weakened in September, as exports increasingly dragged down performance and continued softening demand began to have an impact on companies’ production. In addition, the employment situation worsened further. Downward pressure on China’s economy was significant.”

Also released, the official China PMI manufacturing dropped to 50.8 in September, down from 51.3. Official PMI non-manufacturing rose to 54.9, up from 54.2.

RBA to stand pat, UK PMIs and US NFP featured ahead

RBA rate decision will be a major focus of the week. The central is widely expected to keep interest rate unchanged at 1.50% and maintain a neutral stance. It’s also a big week in terms of Australian data with building approvals, trade balance and retail sales featured.

A lot batch of data will be featured this week too. UK PMIs will catch some attention. But the biggest events will be US non-farm payrolls and Canada employment. Fed is pretty much on auto-pilot but strong wage grow will raise the chance of extending the rate hike cycle beyond neutral rate. Also, BoC is widely expected to hike in October. BoC Governor Stephen Poloz has made himself clear that the cycle will continue gradually. Strong employment data from Canada will support the path the laid.

Here are some highlights for the week:

- Monday: Eurozone PMI manufacturing final, unemployment rate; Swiss retail sales, PMI; UK PMI manufacturing, M4 money supply, mortgage approvals; US ISM manufacturing

- Tuesday: Japan monetary base, consumer confidence; RBA rate decision; UK PMI construction; Eurozone PPI

- Wednesday: Australia building approvals; Eurozone PMI services final, retail sales; UK PMI services; US ADP employment, ISM services

- Thursday: Australia trade balance; US jobless claims, factory orders; Canada Ivey PMI

- Friday: Australia retail sales; Japan leading indicators; German factory orders, PPI; Swiss foreign currency reserves, CPI; Canada employment, trade balance; US non-farm payroll, trade balance.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2860; (P) 1.2954; (R1) 1.3003; More…

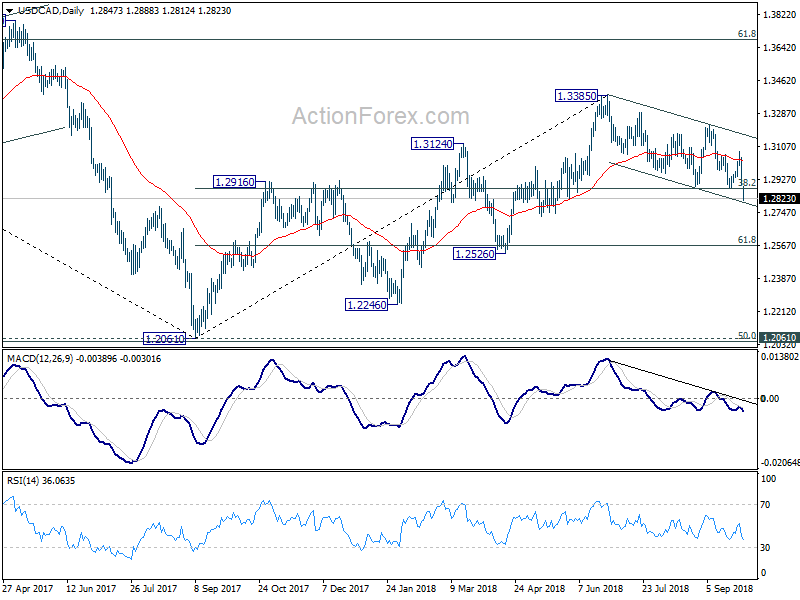

USD/CAD drops sharply to as low as 1.2812 so far today and fall from 1.3385 resumes. With 1.2879 key fibonacci level firmly taken out, such decline should now target next fibonacci level at 1.2567, which is close to 1.2526 support. On the upside, break of 1.3081 resistance is needed to indicate short term bottoming. Otherwise, outlook will remain bearish even in case of recovery.

In the bigger picture, the firm break of 38.2% retracement of 1.2061 to 1.3385 at 1.2879 key fibonacci level argues that whole choppy rebound from 1.2061 has completed at 1.3385 already. Deeper fall would be seen back to 61.8% retracement at 1.2567, which is close to 1.2526 support and possibly below. For now, we’re not seeing fall from 1.3385 as resuming larger down trend from 1.4689 (2015 high) yet. Thus, we’ll look for bottoming signal again below 1.2567 .

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Manufacturing Index Sep | 59 | 56.7 | ||

| 23:50 | JPY | Tankan Large Manufacturing Index Q3 | 19 | 22 | 21 | |

| 23:50 | JPY | Tankan Large Manufacturers Outlook Q3 | 19 | 19 | 21 | |

| 23:50 | JPY | Tankan Large Non-Manufacturing Index Q3 | 22 | 22 | 24 | |

| 23:50 | JPY | Tankan Non-Manufacturing Outlook Q3 | 22 | 20 | 21 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q3 | 13.40% | 14.20% | 13.60% | |

| 23:50 | JPY | Tankan Small Manufacturing Index Q3 | 14 | 13 | 14 | |

| 23:50 | JPY | Tankan Small Manufacturing Outlook Q3 | 11 | 12 | 12 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Index Q3 | 10 | 6 | 8 | |

| 23:50 | JPY | Tankan Small Non-Manufacturing Outlook Q3 | 5 | 4 | 5 | |

| 0:30 | JPY | PMI Manufacturing Sep F | 52.5 | 52.9 | 52.9 | |

| 1:00 | AUD | TD Securities Inflation M/M Sep | 0.30% | 0.10% | ||

| 7:15 | CHF | Retail Sales Real Y/Y Aug | 0.40% | -0.30% | ||

| 7:30 | CHF | PMI Manufacturing Sep | 60.8 | 64.8 | ||

| 7:45 | EUR | Italy Manufacturing PMI Sep | 51.1 | 50.1 | ||

| 7:50 | EUR | France Manufacturing PMI Sep F | 52.5 | 52.5 | ||

| 7:55 | EUR | Germany Manufacturing PMI Sep F | 53.7 | 53.7 | ||

| 8:00 | EUR | Eurozone Manufacturing PMI Sep F | 53.3 | 53.3 | ||

| 8:30 | GBP | Mortgage Approvals Aug | 65K | 65K | ||

| 8:30 | GBP | Money Supply M4 M/M Aug | 0.60% | 0.90% | ||

| 8:30 | GBP | PMI Manufacturing Sep | 53.8 | 52.8 | ||

| 9:00 | EUR | Eurozone Unemployment Rate Aug | 8.20% | 8.20% | ||

| 13:30 | CAD | Manufacturing PMI Sep | 56.6 | 56.8 | ||

| 13:45 | USD | Manufacturing PMI Sep F | 55.4 | 55.6 | ||

| 14:00 | USD | Construction Spending M/M Aug | 0.40% | 0.10% | ||

| 14:00 | USD | ISM Manufacturing Sep | 60 | 61.3 | ||

| 14:00 | USD | ISM Employment Sep | 58.5 | |||

| 14:00 | USD | ISM Prices Paid Sep | 70.8 | 72.1 |

{kind=link}