Euro and Sterling recover mildly in Asian session but they remain the weakest two for the week. Brexit impasse and Italian budget continued to weigh down both currencies, which also drags down Swiss Franc. Dollar’s rally extended lower night as helped by hawkish comments from a top Fed official. There are tentative signs of more Dollar strength but it’s yet to be confirmed. Meanwhile, Australian and New Zealand Dollar are the strongest ones despite weakness in global equities, in particular China. And weaker than expected Chinese GDP was shrugged off by both Aussie and Kiwi.

Technically, EUR/USD is on track to 1.1431 support and break will confirm resumption of fall from 1.1814. USD/CHF stays firm as recent rally has resumed, even though there is no acceleration yet. GBP/USD’s break of 1.3081 overnight should now send the pair back to 1.2921 support. USD/CAD’s break of 1.3081 resistance also argue that rebound fro 1.2781 is resuming and carries near term bullish implications. It should also be noted that EUR/JPY resumed recent fall from 129.11 and should target 127.85 support next. GBP/JPY will likely test 145.67 resistance turned support. Break there will turn outlook bearish and re-align the outlook with EUR/JPY.

In other markets, DOW closed own 1.27% overnight, S&P 500 down -1.44% and NASDAQ dropped -2.06%. But all three indices are kept well above last week’s lows. US 30-year yield closed up 0.013 at 3.359, 10 year yield down -0.004 at 3.175, five-year yield down -0.017 at 3.024. Strength continues to be seen at the long end.

In Asia, Nikkei is down -1.06% at the time of writing, Singapore Strait Times down -0.24%, Hong Kong HSI down -0.34%. China Shanghai SSE hit as low as 2449.20 earlier today as down trend extended. Subsequent recovery is capped by 2500 handle as well as weaker than expected China GDP. Another round of selloff could be seen before weekly close.

Fed Quarles: Right strategy is to maintain the gradual course

Fed Governor Randal Quarles said in a speech yesterday that monetary policy shouldn’t “drift” because of the uncertainties around many macroeconomic inputs Instead, Fed policymakers should “chart a course that is stable, gradual, and predictable; communicate it clearly; and then follow that course through the temporarily shifting and sometimes conflicting signs from the economy”. And, to him, given that “the economy has performed fundamentally as I expected”, the “right strategy is to maintain the gradual course”.

On the one hand, the “productive capacity” of the US might be increasing so there is no need to “accelerate our pace”. On the other hand, there there is enough doubt that “current inflation as an infallibly reliable measure of current resource constraints”. Hence, “continued gradual removal of accommodation is appropriate.”

EU: Italy’s budget an obvious significant deviation of Stability and Growth Pact

EU Commissioners Valdis Dombrovskis and Pierre Moscovici wrote a joint letter to warn Italy of its budget plan. Handing the letter directly to Italian Economy Minister Giovanni Tria, the EU started the first formal step to reject the budget which will lead to direct clash between Rome and Brussels. Italy will now have until October 22 to respond to the letter.

EU said in the letter that Italy’s plan is an “obvious significant deviation” of the recommendations adopted by the European Council under the 2019 Stability and Growth Pact. Also, while the Council suggested fiscal adjustment, the Italy plans fiscal expansion of close to 1% of GDP, and the “size of the deviation (a gap of around 1.5% of GDP) are unprecedented”.

EU also criticized that the macroeconomic forecasts under the plan has not been endorsed by the Parliamentary Budget Office. And this appears “not to respect” the rules of having forecasts produced or endorsed by an “independent body”.

Italian Prime Minister Giuseppe Conte said they’re ready to reply to EU’s concern and he’s not worried.

China Q3 GDP slowed to 6.5%, Shanghai SSE recovery capped by 2500

China’s Shanghai SSE Composite dived to as low as 2449.20 in initial trading, following the steep selloff in the US. The index recovered after the China Banking and Insurance Regulatory Commission (CBRC) announced measures to encourage private equity funds to buy public traded shares. However, weaker than expected Q3 GDP data appears to cap SSE’s recovery as it fails to get hold of 2500 handle.

Released from China, Q3 GDP growth slowed to 6.5% yoy, down from 6.7% yoy in Q2 and missed expectation of 6.6 yoy. That’s also the weakest reading since Q2 of 2009. On quarterly basis, growth slowed to 1.6% qoq, down from Q2’s 1.8% qoq. Also release, industrial production grew 5.8% yoy in September, down from 6.1% and missed expectation of 6.0% yoy. But retail sales rose 9.2% yoy, up from 9.0% yoy and beat expectation of 9.0% yoy. Fixed asset investment rose 5.4% ytd yoy, up from 5.3% ytd yoy and beat expectation of 5.3% ytd yoy.

Statistics bureau spokesman Mao Shengyong said China is still able to reach the full-year growth target of around 6.5% in 2018 even though downward pressure increases. He added that infrastructure investment growth will stabilize and “consumption upgrade” will continue. Nonetheless, Mao also admitted that external environment will pose uncertainties on stabilizing growth.

Elsewhere, Canadian retail sales and CPI to take center stage

Japan national CPI core accelerated to 1.0% yoy in September, up from 0.9% yoy and matched expectations. Eurozone currency account and UK public sector net borrowing are the only notable feature in European session. Canadian data will take center stage later today with retail sales and CPI. US will release existing home sales.

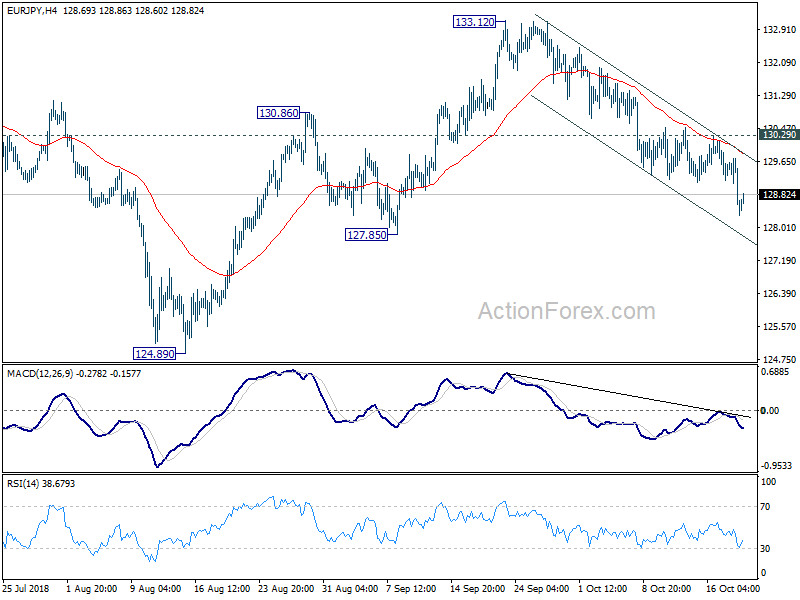

EUR/JPY Daily Outlook

Daily Pivots: (S1) 127.93; (P) 128.84; (R1) 129.36; More….

EUR/JPY’s fall from 133.12 resumed by taking out 129.11 temporary low. Intraday bias is back on the downside for 127.85 support first. Decisive break there will confirm completion of rebound from 124.89 at 133.12. In that case, deeper decline would be seen back to 124.61.89 support zone. On the upside, break of 130.29 resistance is needed to indicate completion of the fall. Otherwise, near term outlook will stay mildly bearish in case of recovery.

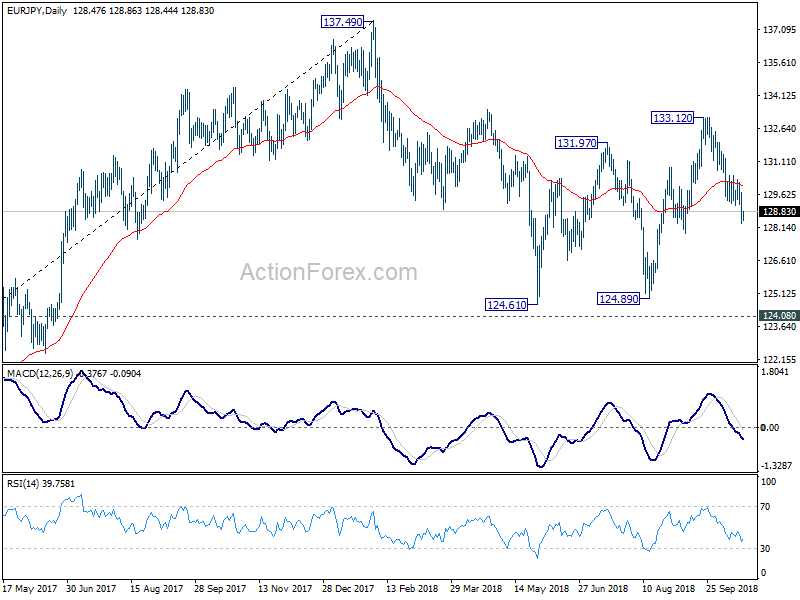

In the bigger picture, current development suggests that EUR/JPY could have defended key support level of 124.08 key resistance turned support. And, the larger up trend from 109.03 (2016 low) is still in progress. Firm break of 137.49 structural resistance will target 141.04/149.76 resistance zone next. This will be the preferred case as long as 127.85 near term support holds. However, break of 127.85 will turn focus back to 124.08 key support level.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Sep | 1.00% | 1.00% | 0.90% | |

| 2:00 | CNY | GDP Y/Y Q3 | 6.50% | 6.60% | 6.70% | |

| 2:00 | CNY | Retail Sales Y/Y Sep | 9.20% | 9.00% | 9.00% | |

| 2:00 | CNY | Industrial Production Y/Y Sep | 5.80% | 6.00% | 6.10% | |

| 2:00 | CNY | Fixed Assets Ex Rural YTD Y/Y Sep | 5.40% | 5.30% | 5.30% | |

| 8:00 | EUR | Eurozone Current Account (EUR) Aug | 21.4B | 21.3B | ||

| 8:30 | GBP | Public Sector Net Borrowing Sep | 4.6B | 5.9B | ||

| 12:30 | CAD | Retail Sales M/M Aug | 0.40% | 0.30% | ||

| 12:30 | CAD | Retail Sales Ex Auto M/M Aug | -0.20% | 0.90% | ||

| 12:30 | CAD | CPI M/M Sep | -0.10% | -0.10% | ||

| 12:30 | CAD | CPI Y/Y Sep | 2.90% | 2.80% | ||

| 12:30 | CAD | CPI Core – Common Y/Y Sep | 2.00% | |||

| 12:30 | CAD | CPI Core – Median Y/Y Sep | 2.10% | |||

| 12:30 | CAD | CPI Core – Trim Y/Y Sep | 2.20% | |||

| 14:00 | USD | Existing Home Sales Sep | 5.31M | 5.34M |

{kind=link}