Risk sentiments generally stabilized after the late rebound in US stocks overnight. DOW hit as low as 24242.22 but closed at 24947.67. Down just -0.32%. S&P 500 also hit as low as 2621.53 but closed at 2695.95, down only -0.15%. NASDAQ even reversed and closed up 0.42% at 7188.26. Treasury yield, however, closed deeper lower with 10-year yield losing -0.048 to 2.876. In Asian, all major indices are trading in black at the time of writing. Nikkei is up 0.48%, Singapore Strait Times up 0.41%, Hong Kong HSI up 0.27%. China Shanghai SSE lags behind and is up 0.08% only. 10 year JGB yield also recovers and is back at 0.059.

In the currency markets, Yen is trading as the weakest one for today, followed by Sterling and the Canadian. New Zealand Dollar is the strongest one for today, followed by Swiss Franc and then Australian. But for the week, Swiss Franc and Yen are overwhelmingly the strongest ones. Australian and Canadian are the weakest. The weekly picture is unlikely to change at close. Though, US non-farm payroll has the prospects to lift Dollar from the third weakest for the week to something better.

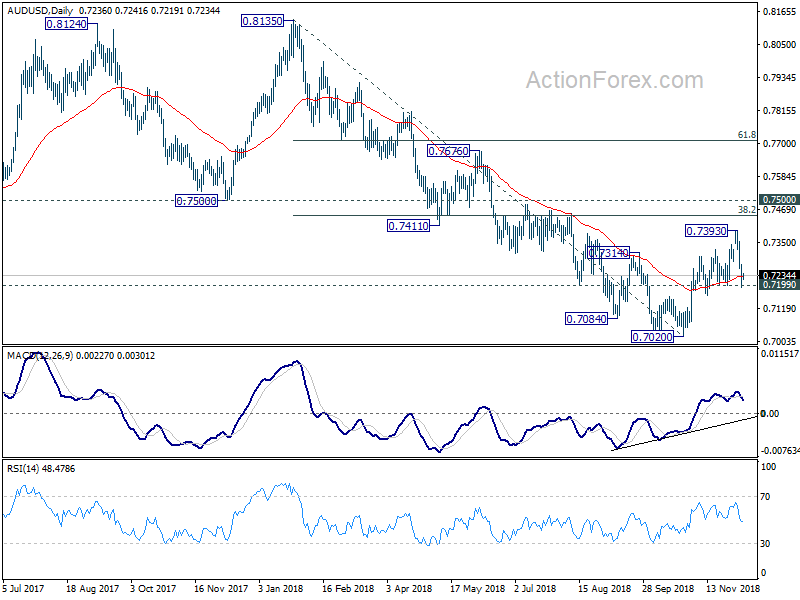

Technically, EUR/USD and GBP/USD are still bounded in familiar range. USD/CHF breached 0.9908 support overnight but recovered quickly. USD/JPY also breached 112.30 but then recovered. USD/JPY is indeed recovering further in Asian session. Thus, overall, there is no clear weakness in Dollar yet. Traders are just cautious ahead of NFP. Australian Dollar is digesting this week’s sharp losses. AUD/USD recovers after touching 0.7199. EUR/AUD retreats after touching 1.5871. These two levels will remain the focus for today.

Fed Powell: Some communities yet to feel full benefits of strong economy

Fed Chair Jerome Powell said in a speech yesterday that “by many national-level measures, our labor market is very strong.” However, he also noted that “aggregate statistics can mask important variations between different demographic and income groups, as well as significant regional differences.” He pointed to statistics indicating unemployment rates in some persistently poor rural counties remain much higher than the national figures.

And, “while the economy is strong overall, we recognize that some communities have yet to feel the full benefits of the ongoing expansion.” Fed is “conducting research, collaborating with communities, and assessing financial regulations so that our nation’s current prosperity will benefit small towns and cities alike.”

Fed Williams: Tariff is a negative for jobs

New York Fed John Williams said in a forum yesterday that the Trump’s tariff war with other countries have “relatively small effect on the economy. But they created higher uncertainty for businesses.

Williams said “at least so far the tariffs that have been put in place, by the United States and other countries, when you roll that up into a $20-trillion economy it doesn’t have a big effect overall on economic growth or inflation”. And, the “much more important and larger” effect is higher uncertainty for businesses. As companies put off investments due to the uncertainties, “that’s a negative for jobs in the short run…and a factor that slows the economy relative to what it could be.”

BoC Poloz admits economy loss momentum going into Q4

BoC Governor Stephen Poloz admitted yesterday that “data released since our October Monetary Policy Report have been on the disappointing side “. And, “the economy has less momentum going into the fourth quarter than we believed it would.”

Also, regarding recent oil price slump, Poloz added “it is already clear that a painful adjustment is developing for Western Canada and there will be a meaningful impact on the Canadian macroeconomy.”

The comments echo BoC’s cautious statement earlier this week and solidify the chance for BoC to pause its rate hikes if things don’t improve.

BoJ Kuroda: No need for additional easing

BoJ Governor Haruhiko Kuroda told the parliament today that “the economy is sustaining its momentum for achieving our 2 percent target. But that momentum lacks strength, so we will carefully watch developments.” For now, though, Kuroda added ” I don’t see the need to take additional monetary easing steps”. And BoJ has no preset idea of what tools to use if more easing is needed, but policy makers will “carefully weigh the cost and benefit of any step we take.”

Released from Japan, household spending dropped -0.3% yoy in October, much worse than expectation of 1.2% yoy rise. Labor cash earnings rose 1.5% yoy, higher than expectation of 1.0% yoy. The weak spending data highlights the fact that there is no condition for consumption to strengthen yet. It still take time for the rise in wages to pass though to consumption and then inflation.

Separately, according to a Reuters poll, 55% of Japanese companies expect 2019 growth to be around the same as 1% in 2018. 31% see it slowing and only 14% see it accelerating. Among the concerns of business, the planned sales tax hike in October and US-China trade war top. US-Japan trade negotiations, emerging markets and Middle East tensions are also seen as risks to growth.

Looking ahead

Germany will release industrial production in European session. Eurozone will release GDP revision. Swiss will release foreign currency reserves.

But US non-farm payroll will be the main focus. Fed’s rate hike beyond December and March hike is highly data dependent. And strong jobs and wage data are needed to convince policy makers to raise interest rate, at least, to upper bound of estimated neutral. Canada will also release job data today.

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7193; (P) 0.7233; (R1) 0.7275; More…

While the fall from 0.7393 was steep, AUD/USD drew support from 0.7199 and recovered. There is no confirmation on reversal yet and intraday bias is neutral for now. On the downside, firm break of 0.7199 will suggest that the corrective rebound from 0.7020 has completed earlier than expected. Deeper fall should then be seen back to retest 0.7020 low. On the upside, above 0.7300 minor resistance will turn bias back to the upside. In that case, corrective rise from 0.7020 would extend to 38.2% retracement of 0.8135 to 0.7020 at 0.7446 before completion.

In the bigger picture, a medium term bottom is in place at 0.7020 ahead of 0.6826 key support (2016 low). Stronger rebound would be seen to corrective the whole fall from 0.8135 high. But we’d expect strong resistance from 0.7500 support turned resistance to limit upside. Medium term fall from 0.8135 should resume and extend to take on 0.6826 low at a later stage, after the correction from 0.7020 completes.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Overall Household Spending Y/Y Oct | -0.30% | 1.20% | -1.60% | |

| 0:00 | JPY | Labor Cash Earnings Y/Y Oct | 1.50% | 1.00% | 1.10% | 0.80% |

| 5:00 | JPY | Leading Index CI Oct P | 104.8 | 104.3 | ||

| 7:00 | EUR | German Industrial Production M/M Oct | 0.30% | 0.20% | ||

| 8:00 | CHF | Foreign Currency Reserves Nov | 753B | |||

| 10:00 | EUR | Eurozone GDP Q/Q | 0.20% | 0.20% | ||

| 13:30 | CAD | Net Change in Employment Nov | 10.0K | 11.2K | ||

| 13:30 | CAD | Unemployment Rate Nov | 5.80% | |||

| 13:30 | USD | Change in Non-farm Payrolls Nov | 200K | 250K | ||

| 13:30 | USD | Unemployment Rate Nov | 3.70% | 3.70% | ||

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.30% | 0.20% | ||

| 15:00 | USD | Wholesale Inventories M/M Oct F | 0.70% | 0.70% | ||

| 15:00 | USD | U. of Mich. Sentiment Dec P | 97 | 97.5 |