While risk aversion continued in Asian session, volatility cooled mildly. Major pairs and crosses are staying in relatively tight range. Swiss Franc and Sterling are generally higher while commodity currencies are soft. But the picture for the day could easily change. For the week, dusts have little settled. Yen is trading as the strongest one on risk aversion. Euro, as second strongest, is supported by weakness in Dollar and Italy-EU budget deal. Australian Dollar is the weakest one, followed by Canadian and then New Zealand Dollar.

Technically, USD/CHF breached 0.9848 key support but quickly recovered. USD/JPY is close to 110.75 key fibonacci level. Meanwhile, EUR/JPY took out 127.61 support quite firmly yesterday. GBP/JPY also break 141.17 support. More downside is now favored in both Yen crosses.

We’ll see whether further decline in EUR/JPY and GBP/JPY would drag USD/JPY down. Or, selloff in EUR/JPY and GBP/JPY with rebound in USD/JPY and USD/CHF would drag down EUR/USD and GBP/USD.

DOW at critical fibonacci level, US yield curve flattened further

Risk aversion once again spread from US to Asian session. Nikkei closed down -1.11%, or 226.39 pts to 20166.19. That’s the lowest level since September 2017 and 20000 handle is now vulnerable. At the time of writing, China Shanghai SSE is down -1.11% at 2508. However, losses in Singapore Strait Times (-0.30%) and Hong Kong HSI (-0.03%) are relatively limited.

Overnight, DOW lost -1.99% or -464.06pts to 22859.60. S&P 500% dropped -1.58% and NASDAQ dropped -1.63%. DOW is now pressing key support level at 38.2% retracement of 15450.56 to 26951.81 at 22558.33. There is prospect of some recovery before yearly close. But it has to overcome near term resistance at around 23500 before declaring bottoming.

On important development to note is that acceleration in flattening of US yield curve. Overnight, 5-year yield closed up 0.026 to 2.653. 10-year yield rose 0.011 to 2.789. More importantly, 30-year yield breached 3% handle to 2.957, then closed at 3.012, down -0.003. Meanwhile, yield curve remains inverted between 2-year (2.675) and 3-year (2.652).

Japan cabinet approved record fiscal 2019 budget

Japan Prime Minister Shinzo Abe’s Cabinet approved budget for fiscal 2019. The general account budget would rise for the seventh straight years, to JPY 101.5T, comparing to current fiscal year’s initial estimate of JPY 97.7T.

Of the JPY 101.5T, around JPY 2T will be spent specifically to ease the impact from the planned sales tax hike in October 2019, from 8% to 10%. Measures will include shopping vouchers to help low income households.

However, stimulus measures will altogether hit JPY 6.5T, far exceeding the estimated increase in sale tax revenue. Some economists noted that Abe has now set the precedence that rise in tax would actually be delaying fiscal reform.

Nevertheless, Finance Minister Taro Aso emphasized that “we were able to manage both needs of economic revival and fiscal consolidation with this budget.”

On the data front

Japan national CPI core slowed to 0.9% yoy in November, down from 1.0% yoy and missed expectation of 1.0% yoy.

Germany will release Gfk consumer confidence in European session. UK will release Q3 GDP final, current account balance and public sector net following.

Later in the day, Canada will release October GDP and retail sales. US will release Q3 GDP final, durable goods orders and PCE inflation. Some more volatility could be seen before weekly close.

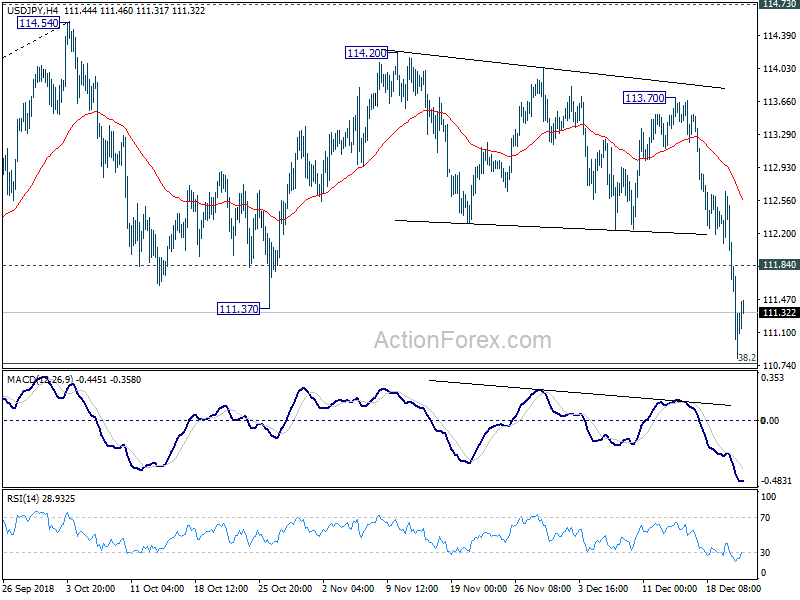

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.53; (P) 111.57; (R1) 112.33; More..

USD/JPY dropped to as low as 110.81 so far before recovery mildly. Outlooks is unchanged that price actions from 114.54 are viewed as a consolidation pattern. We’d continue to expect downside to be contained by 38.2% retracement of 104.62 to 114.54 at 110.75 to bring rebound. On the upside, break of 111.84 will turn bias back to the upside for rebound to 4 hour 55 EMA (now at 112.56). However, firm break of 110.75 will target 61.8% retracement at 108.40.

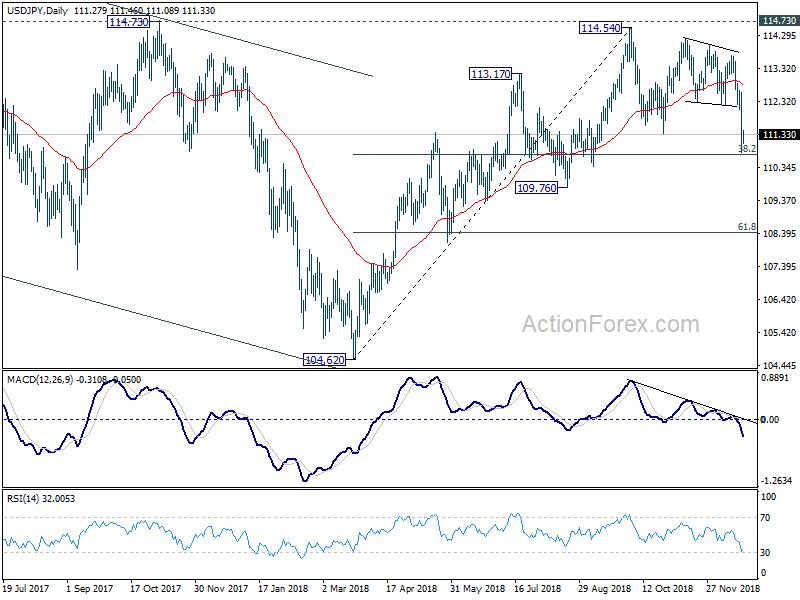

In the bigger picture, corrective fall from 118.65 (2016 high) should have completed with three waves down to 104.62. Decisive break of 114.73 resistance will likely resume whole rally from 98.97 (2016 low) to 100% projection of 98.97 to 118.65 from 104.62 at 124.30, which is reasonably close to 125.85 (2015 high). This will stay as the preferred case as long as 109.76 support holds. However, decisive break of 109.76 will dampen this bullish view and turns outlook mixed again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Nov | 0.90% | 1.00% | 1.00% | |

| 7:00 | EUR | German GfK Consumer Confidence Jan | 10.3 | 10.4 | ||

| 9:30 | GBP | Public Sector Net Borrowing Nov | 7.0B | 8.0B | ||

| 9:30 | GBP | Current Account Balance (GBP) Q3 | -22.2B | -20.3B | ||

| 9:30 | GBP | GDP Q/Q Q3 F | 0.60% | 0.60% | ||

| 9:30 | GBP | Total Business Investment Q/Q Q3 F | -1.20% | -1.20% | ||

| 13:30 | CAD | Retail Sales M/M Oct | 0.60% | 0.20% | ||

| 13:30 | CAD | Retail Sales Ex Auto M/M Oct | 0.30% | 0.10% | ||

| 13:30 | CAD | GDP M/M Oct | 0.20% | -0.10% | ||

| 13:30 | USD | GDP Annualized Q/Q Q3 T | 3.50% | 3.50% | ||

| 13:30 | USD | GDP Price Index Q3 T | 1.70% | 1.70% | ||

| 13:30 | USD | Durable Goods Orders Nov P | 1.80% | -4.30% | ||

| 13:30 | USD | Durables Ex Transportation Nov P | 0.30% | 0.20% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec A | -4 | -4 | ||

| 15:00 | CAD | BoC Business Outlook Survey | ||||

| 15:00 | USD | Personal Income Nov | 0.30% | 0.50% | ||

| 15:00 | USD | Personal Spending Nov | 0.30% | 0.60% | ||

| 15:00 | USD | PCE Deflator M/M Nov | 0.20% | |||

| 15:00 | USD | PCE Deflator Y/Y Nov | 2.00% | |||

| 15:00 | USD | PCE Core M/M Nov | 0.20% | 0.10% | ||

| 15:00 | USD | PCE Core Y/Y Nov | 1.90% | 1.80% | ||

| 15:00 | USD | U. of Mich. Sentiment Dec F | 97.6 | 97.5 |

{kind=link}