Dollar turns into consolidation in Asian session but it’s able to maintain most of this week’s gain. The greenback’s fate remains heavily dependent on whether Fed will cut interest rates later in the month. Strong economic data so far argue against a move. Yet, it seems they’re not strong enough to convince FOMC members to dismiss the chance of a move. On the other hand, European majors are staying as the worst performing ones. Euro is weighed down by poor data that reaffirm ECB’s easing stance. Sterling is pressured by renewed no-deal Brexit fear.

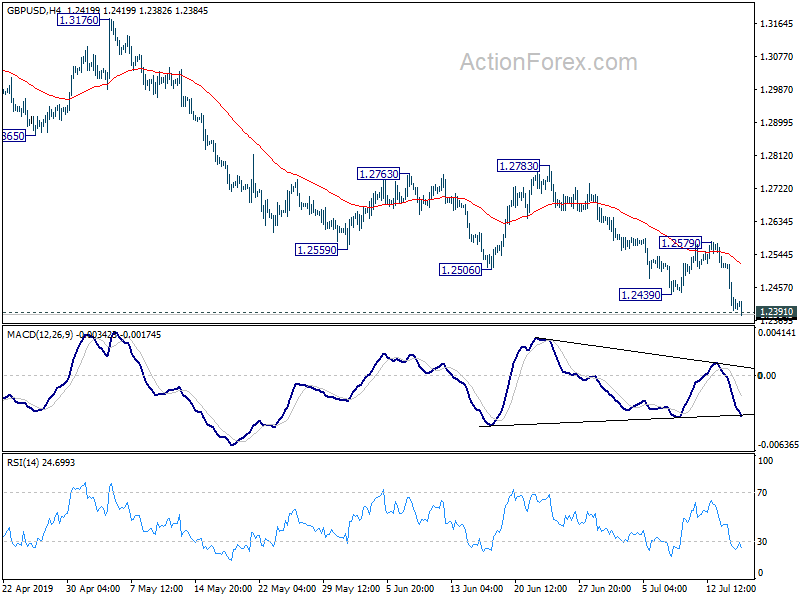

Technically, GBP/USD is in proximity to 1.2391 key support (2019 low). Firm break there will resume down rend from 1.4376 (2018 high). EUR/USD is also eyeing 1.1193 temporary low. Break will bring 1.1107 (2019 low) into focus. USD/CAD is stuck in tight range for now. Canadian CPI would be the trigger for the Loonie to finally confirm medium term bearish reversal in USD/CAD.

In Asia, Nikkei closed down -0.31%. Hong Kong HSI is down -0.27%. China Shanghai SSE is down -0.26%. Singapore Strait Times is up 0.01%. Japan 10-year JGB yield is down -0.0012 at -0.121. Overnight, DOW dropped -0.09%. S&P 500 dropped -0.34%. NASDAQ dropped -0.43%. 10-yer yield rose 0.030 to 2.122.

Fed Powell reiterates pledge to act as appropriate

Fed Chair Jerome Powell’s speech in Paris on Tuesday was largely similar to what he’s said recently. He reiterated the pledged to “act as appropriate to sustain the expansion, with a strong labor market and inflation near its symmetric 2 percent objective.”

In the baseline outlook, Fed expected growth to “remain solid, labor markets to stay strong, and inflation to move back up and run near 2 percent”. However, “uncertainties about this outlook have increased”, particularly regarding “trade developments and global growth”.

Powell also noted the influences between monetary policies in different countries, “financial markets, trade, and confidence channels”. And he noted, “pursuing our domestic mandates in this new world requires that we understand the anticipated effects of these interconnections and incorporate them into our policy decision making.

Fed Evans: On basis of inflation alone, a couple of rate cuts could be needed

Chicago Fed President Charles Evans, probably most dovish FOMC member, said “on the basis of inflation alone, I could feel confident in arguing for a couple of rate cuts before the end of the year.”

He said in a CNBC interview yesterday that “in order to get inflation up to 2.25% over the next three years, I need 50 basis points of more accommodation.” And, “maybe that’s not quite enough”.

Though, he also acknowledged that the economy is “doing well” and “we are ten years into an expansion.” But after missing the inflation target for a decade, “two and a quarter or a little bit more would be about appropriate.”

Fed Kaplan: Tactical rate cut could address risks seen in bond markets

Dallas Fed President Robert Kaplan said yesterday that “the best argument” for him to support rate cut is the “shape” of the yield curve. And, a “tactical” reduction of a quarter point could address the risks seen by bond investors.

He also said that inflation is likely to remain low because of the change in the economy and the link between wages and prices. He added businesses are not able to pass on higher costs to customers because of stiff competition. They have to absorb lower profits so they don’t lose market share.

Separately, San Francisco Fed President Mary Daly said she’s not leaning one way or the other on July interest rate decision. And, she will learn a lot in the next two months regarding whether rates would be lower by year end.

On the one hand, she noted it’s too early to tell if additional stimulus was needed. And she saw no clouds looming on consumer spending and labor market. On the other hand, Daly noted business felt uncertain. She saw potpourri of headwinds, including trade, mood, uncertainty, global slowdown.

Fitch affirmed Japan’s A rating, expects grow to lose steam after robust Q1

Fitch Ratings has affirmed Japan’s Long-Term Foreign Currency Issuer Default Rating (IDR) at ‘A’ with a stable outlook. In the statement, Fitch noted that the ratings ” balance the strengths of an advanced and wealthy economy, with high governance standards and strong public institutions, against weak medium-term growth prospects and high public debt.”

The rating agency projects GDP growth of 0.8% in 2019 despite an unexpectedly robust 2.1% in Q1. And, GDP growth is expected to lose steam through early 2020 from “weakening exports and industrial production.” Japan and other countries in the region are reeling from the effects of the “global trade downturn” associated with the escalation in the US-China trade dispute. And, a further escalation of global trade tensions could pose a “significant risk” to the outlook for Japan. Also, “recent imposition of export restrictions on Korea has increased geopolitical tensions”.

BoE Cunliffe: Could see stockpiling cycle build up again in Q3 on Brexit

In an interview with Newcastle Journal yesterday, BoE Deputy Governor Jon Cunliffe said “I haven’t picked up a strong sense that the economy is contracting and people are seeing big drops in demand”.

Q2 will likely be weak due to unwinding of stocks. But he added “with Q1 and the second quarter of this year, you won’t get a very accurate read on the underlying nature of the economy”.

Additionally, there is a Brexit “decision point” coming up on October 31. And, “we don’t know whether we’ll leave, or stay, or whether there’ll be an extension”. He added “we could see that stockpiling cycle build up again”.

Looking ahead

Inflation data will be major focus today. UK will release CPI, RPI, PPI and house price index. Eurozone will release June CPI final. Later in the day, Canada will release CPI and manufacturing sales. US will release housing starts and building permits. Fed will also release Beige Book economic report.

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2361; (P) 1.2441; (R1) 1.2486; More….

Intraday bias in GBP/USD remains on the downside as recent decline is in progress. Sustained break of 1.2391 low will confirm resume larger down trend for 61.8% projection of 1.4376 to 1.2391 from 1.3381 at 1.2154 next. On the upside, break of 1.2579 resistance is needed to indicate short term bottoming. Otherwise, outlook remains bearish in case of recovery.

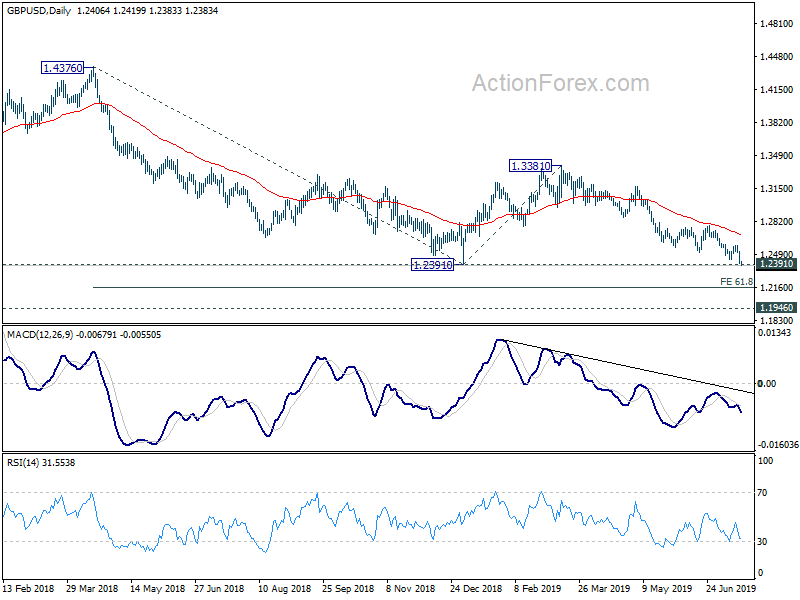

In the bigger picture, down trend from 1.4376 (2018 high) is still in progress. Break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence, focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:30 | AUD | Westpac Leading Index M/M Jun | -0.08% | -0.10% | ||

| 8:30 | GBP | CPI M/M Jun | 0.00% | 0.30% | ||

| 8:30 | GBP | CPI Y/Y Jun | 2.00% | 2.00% | ||

| 8:30 | GBP | Core CPI Y/Y Jun | 1.80% | 1.70% | ||

| 8:30 | GBP | RPI M/M Jun | 0.10% | 0.30% | ||

| 8:30 | GBP | RPI Y/Y Jun | 2.90% | 3.00% | ||

| 8:30 | GBP | PPI Input M/M Jun | -0.50% | 0.00% | ||

| 8:30 | GBP | PPI Input Y/Y Jun | 0.30% | 1.30% | ||

| 8:30 | GBP | PPI Output M/M Jun | 0.10% | 0.30% | ||

| 8:30 | GBP | PPI Output Y/Y Jun | 1.70% | 1.80% | ||

| 8:30 | GBP | PPI Output Core M/M Jun | 0.10% | 0.10% | ||

| 8:30 | GBP | PPI Output Core Y/Y Jun | 1.70% | 2.00% | ||

| 8:30 | GBP | House Price Index Y/Y May | 1.30% | 1.40% | ||

| 9:00 | EUR | Eurozone CPI M/M Jun | 0.10% | 0.10% | ||

| 9:00 | EUR | Eurozone CPI Y/Y Jun F | 1.20% | 1.20% | ||

| 9:00 | EUR | Eurozone CPI Core Y/Y Jun F | 1.10% | 1.10% | ||

| 12:30 | CAD | CPI M/M Jun | -0.30% | 0.40% | ||

| 12:30 | CAD | CPI Y/Y Jun | 2.00% | 2.40% | ||

| 12:30 | CAD | CPI Core – Common Y/Y Jun | 1.80% | 1.80% | ||

| 12:30 | CAD | CPI Core – Median Y/Y Jun | 2.10% | 2.10% | ||

| 12:30 | CAD | CPI Core – Trim Y/Y Jun | 2.20% | 2.30% | ||

| 12:30 | CAD | Manufacturing Sales M/M May | 2.00% | -0.60% | ||

| 12:30 | USD | Housing Starts Jun | 1.26M | 1.27M | ||

| 12:30 | USD | Building Permits Jun | 1.30M | 1.29M | ||

| 14:30 | USD | Crude Oil Inventories | -9.5M | |||

| 18:00 | USD | Federal Reserve Beige Book |

{kind=link}