The forex markets are generally locked in tight range today. Canadian Dollar is supported by largely expected consumer inflation data. While Loonie is the second strongest for today so far, USD/CAD is stuck in familiar range. The markets are indeed rather mixed, as seen in New Zealand Dollar being the strongest and Australian being weakest. Euro is mixed after upward revision in June’s CPI reading. Sterling continues to shrug off economic data, but stays pressured on no-deal Brexit fear.

Technically, GBP/USD breached 1.2391 low but recovered quickly sustained break will confirm medium term down trend resumption. 0.6983 minor support in AUD/USD will be watched and break will confirm rejection by 0.7047 resistance. USD/CAD could finally breakout from range of 1.3018/3143 with today’s oil inventory data.

In other markets, DOW opens nearly flat while 10-year yield is down -0.0114 at 2.093. In Europe, FTSE is down -0.18%. DAX is down -0.18%. CAC is down -0.17%. German 10-year yield is down -0.042 at -0.289, staying comfortably above -0.3 handle. Earlier in Asia, Nikkei dropped -0.31%. Hong Kong HSI dropped -0.09%. China Shanghai SSE dropped -0.20%. Singapore Strait Times rose 0.14%. Japan 10-year JGB yield dropped -0.0052 to -0.125.

Canada CPI slowed to 2.0%, manufacturing sales rose 1.6%

In June, Canada headline CPI slowed to 2.0% yoy, down from 2.4% and matched expectations. CPI core -common was unchanged at 1.8% yoy, matched expectations. CPI core -median was unchanged at 2.2% yoy, above expectation of 2.1% yoy. CPI core – trim slowed to 2.1% yoy, down from 2.3% yoy , miss expectation of 2.2% yoy.

Manufacturing sales rose 1.6% mom to CAD 58.9B in May, missed expectation of 2.0% mom. The increase was mainly due to higher sales in the transportation equipment industry. Sales were up in 12 of 21 industries, representing 66.2% of total Canadian manufacturing.

From US, housing starts dropped to 1.25m annualized in June. Building permits dropped to 1.22m annualized.

UK Barclay: No-deal Brexit underpriced, House won’t approve current deal

UK Brexit Minister Stephen Barclay warned today that no-deal Brexit is underpriced. He also told EU chief Brexit negotiator Michel Barnier that the current withdrawal agreement would not be approved by the UK parliament without any change.

Barclay said “I think a no deal is underpriced. It is still this government’s intention and both leadership candidates’ intention to seek a deal and I think it is the will of many members of parliament for there to be a deal”. However, “the question then will be is there a deal that is palatable to parliament and if not will parliament vote to revoke or will we leave with no deal?”

Regarding his conversation with Barnier, Barclay clarified “What I said was the House had rejected it three times … that the European election results in my view had further hardened attitudes across the House and that the text unchanged, I did not envisage going through the House.”

UK CPI unchanged at 2.0%, core CPI rose to 1.8%

In June, UK headline CPI was unchanged at 2.0% yoy, matched expectations. Core CPI accelerated to 1.8% yoy, up from 1.7% yoy, matched expectations. RPI slowed to 2.9% yoy, down from 3.0% yoy, matched expectations. PPI input was at -1.4% mom, -0.3% yoy, versus expectation of -0.5% mom, 0.3% yoy. PPI output was at -0.1% mom, 1.6% yoy, versus expectation of 0.1% mom, 1.7% yoy. PPI output core was at 0.1% mom, 1.7% yoy, matched expectations. In May, house price index rose 1.2% yoy, slowed from 1.5% yoy, versus expectation of 1.3% yoy.

ECB Coeure: Determined to act in case of adverse contingencies

ECB Executive Board member Benoit Coeure said the central banks “determined to act in case of adverse contingencies and also stands ready to adjust all of its instruments, as appropriate, to ensure that inflation continues to move toward the Governing Council’s inflation aim in a sustained manner”.

He said today that Eurozone economy was showing signs of “somewhat weaker growth” in Q2 and Q3. Risks are also tilted to the downside. Underlying inflation remained generally muted even though it’s seen increasing over the medium term.

Eurozone CPI finalized at 1.3%, revised up, core CPI at 1.1%

Eurozone CPI was finalized at 1.3% yoy in June, revised up from 1.2%, up from May’s 1.2% yoy. Core CPI was finalized at 1.1% yoy, unrevised, up from May’s 0.8% yoy. EU 28 CPI was finalized at 1.6% yoy, stable compared to May.

The lowest annual rates were registered in Greece (0.2%), Cyprus (0.3%), Denmark and Croatia (both 0.5%). The highest annual rates were recorded in Romania (3.9%), Hungary (3.4%) and Latvia (3.1%). Compared with May, annual inflation fell in seventeen Member States, remained stable in one and rose in nine.

In June, the highest contribution to the annual euro area inflation rate came from services (0.73%), followed by food, alcohol & tobacco (0.30%), energy (0.17%) and non-energy industrial goods (0.07%).

BoJ Kuroda: Economy growing moderately despite some weakness in exports and output

BoJ Governor Haruhiko Kuroda reiterated his view that the economy is “growing moderately” even though policymakers were “seeing some weakness in exports and output”. He said today in France that capital expenditure remained “very firm” and the global economy was still sustaining moderate growth despite various risks.

He added, “the board will debate policy this month based on this view”. But he also emphasized we will swiftly consider additional monetary easing steps if the economy loses momentum for hitting our inflation target.”

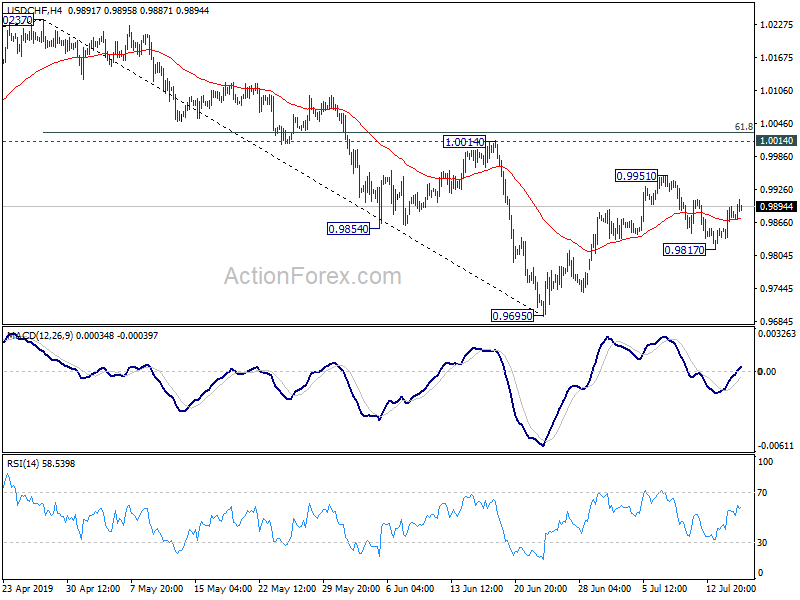

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9845; (P) 0.9870; (R1) 0.9903; More…

USD/CHF is staying in range of 0.9817/9951 and intraday bias remains neutral first. On the downside, below 0.9817 will resume the decline from 0.9951 to retest 0.9695 low first. On the upside, above 0.9951 will extend the rebound from 0.9695. In that case, upside should be limited by 61.8% retracement of 1.0237 to 0.9695 at 1.0030.

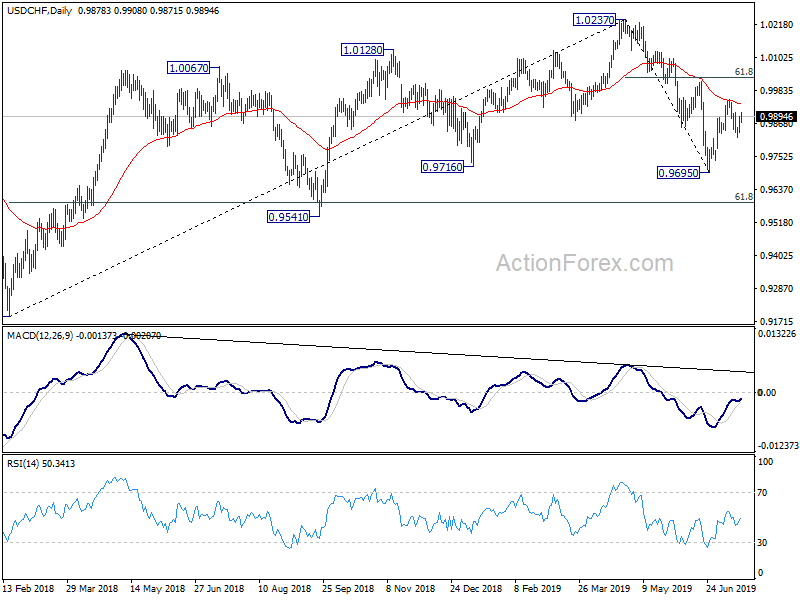

In the bigger picture, up trend from 0.9186 (2018 low) should have completed at 1.0237 already. Deeper decline would be seen to 61.8% retracement of 0.9186 to 1.0237 at 0.9587 and below. For now, USD/CHF is seen as in long term range pattern between 0.9186 and 1.0342. Hence, we’d pay attention to bottoming signal below 0.9587. However, sustained break of 1.0014 will revive medium term bullishness and turn focus back to 1.0237 high.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Westpac Leading Index M/M Jun | -0.08% | -0.10% | ||

| 08:30 | GBP | CPI M/M Jun | 0.00% | 0.00% | 0.30% | |

| 08:30 | GBP | CPI Y/Y Jun | 2.00% | 2.00% | 2.00% | |

| 08:30 | GBP | Core CPI Y/Y Jun | 1.80% | 1.80% | 1.70% | |

| 08:30 | GBP | RPI M/M Jun | 0.10% | 0.10% | 0.30% | |

| 08:30 | GBP | RPI Y/Y Jun | 2.90% | 2.90% | 3.00% | |

| 08:30 | GBP | PPI Input M/M Jun | -1.40% | -0.50% | 0.00% | |

| 08:30 | GBP | PPI Input Y/Y Jun | -0.30% | 0.30% | 1.30% | 1.40% |

| 08:30 | GBP | PPI Output M/M Jun | -0.10% | 0.10% | 0.30% | |

| 08:30 | GBP | PPI Output Y/Y Jun | 1.60% | 1.70% | 1.80% | 1.90% |

| 08:30 | GBP | PPI Output Core M/M Jun | 0.10% | 0.10% | 0.10% | |

| 08:30 | GBP | PPI Output Core Y/Y Jun | 1.70% | 1.70% | 2.00% | |

| 08:30 | GBP | House Price Index Y/Y May | 1.20% | 1.30% | 1.40% | 1.50% |

| 09:00 | EUR | Eurozone CPI M/M Jun | 0.20% | 0.10% | 0.10% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 1.30% | 1.20% | 1.20% | |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 1.10% | 1.10% | 1.10% | 0.80% |

| 12:30 | CAD | CPI M/M Jun | -0.20% | -0.30% | 0.40% | |

| 12:30 | CAD | CPI Y/Y Jun | 2.00% | 2.00% | 2.40% | |

| 12:30 | CAD | CPI Core – Common Y/Y Jun | 1.80% | 1.80% | 1.80% | |

| 12:30 | CAD | CPI Core – Median Y/Y Jun | 2.20% | 2.10% | 2.10% | 2.20% |

| 12:30 | CAD | CPI Core – Trim Y/Y Jun | 2.10% | 2.20% | 2.30% | |

| 12:30 | CAD | Manufacturing Sales M/M May | 1.60% | 2.00% | -0.60% | -0.40% |

| 12:30 | USD | Housing Starts Jun | 1.25M | 1.26M | 1.27M | |

| 12:30 | USD | Building Permits Jun | 1.22M | 1.30M | 1.29M | 1.30M |

| 14:30 | USD | Crude Oil Inventories | -3.6M | -9.5M | ||

| 18:00 | USD | Federal Reserve Beige Book |

{kind=link}