Asian markets are trading generally lower today as another weak starts. Though, weakness in stocks is relatively limited. Expectations on Fed and ECB easing remain generally firm. It looks like a matter of when and how much easing only. In the currency markets, Yen is trading mildly lower, followed by Swiss Franc. New Zealand Dollar is currently the strongest, but Dollar and Sterling are not too far away. The economic calendar is very light today but heavy weight events lie ahead.

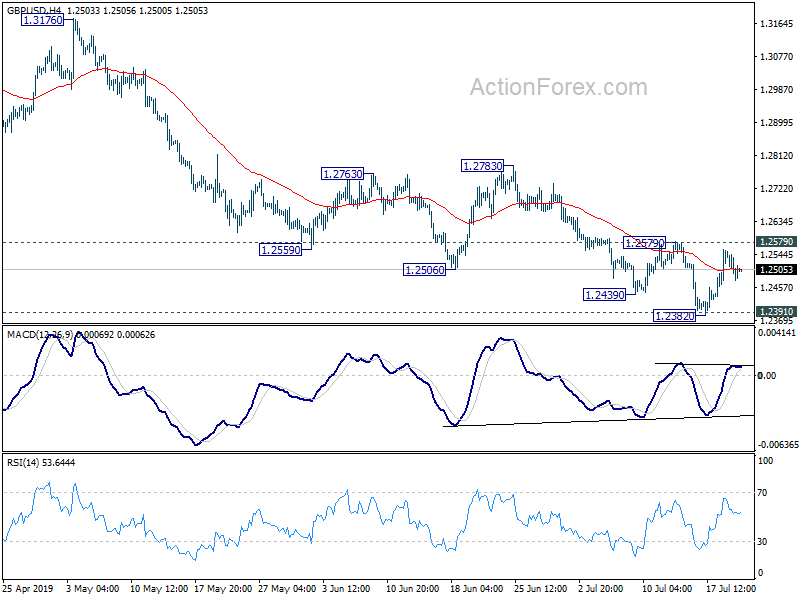

Technically, Sterling will be a major focus in the early part of the week, leading up to the announcement of the next UK Conservative leader. GBP/USD has been drawing support from 1.2391 and recovered. A break of 1.2579 minor resistance would indicate short term bullish reversal for stronger rebound ahead. EUR/GBP is also pressing 0.8954 minor support. Firm break there would also indicate short term bearish reversal for deeper decline.

In Asia, currently, Nikkei is down -0.35%. Hong Kong HSI is down -0.75%. China Shanghai SSE is down -0.75%. Singapore Strait Times is down -0.61%. Japan 10-year JGB yield is up 0.0016 at -0.134.

ECB, UK and US GDP ahead

ECB rate decision will be a major focus for the week. Despite recent dovish rhetorics, the central is expected to stand pat first, and set the stage for a September move instead, when new economic forecasts are published. The question is on what ECB would do, an interest cut only, or resuming quantitative easing? Also from Eurozone, PMIs and German Ifo business climate will be watched.

UK politics will also take center stage too. Ballot for UK Conservative Party leader will close today. Results will be announced on Tuesday. Boris Johnson is widely expected to win the race and become the next Prime Minister. The change in UK government then would shape the path to Brexit on October 31.

It’s a week of blackout for Fed speakers. Main focus will be on durables goods orders, goods trade balance and most important Q2 GDP in the US. Markets are still pricing in full chance of rate cut on July 31. We’ll see, after recent solid data, if another upside surprise in Q2 GDP could prompt a rethink.

Here are some highlights for the week:

- Monday: Bundesbank monthly report; Canada wholesale sales.

- Tuesday: UK CBI industrial order expectations; US house price index, existing home sales.

- Wednesday: New Zealand trade balance; Australia PMIs; Japan PMI manufacturing; Eurozone PMI manufacturing, M3 money supply; UK BBA mortgage approvals; US PMIs, new home sales.

- Thursday: Japan corporate service price index; German Ifo business climate; UK CBI realized sales; ECB rate decision; US durable goods orders, goods trade balance, wholesale inventories, unemployment claims.

- Friday: Tokyo CPI; German import prices; US GDP.

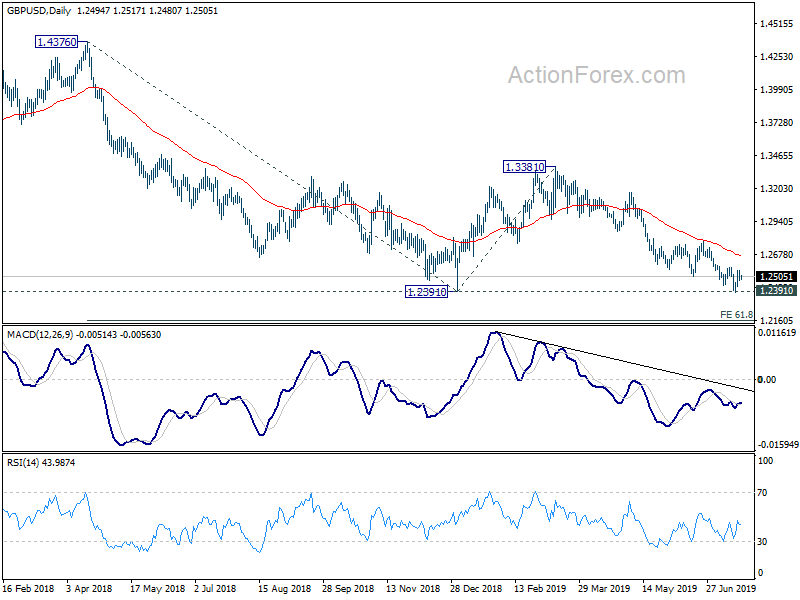

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2467; (P) 1.2512; (R1) 1.2548; More….

Intraday bias in GBP/USD remains neutral for the moment. Further fall is in favor as long as 1.2579 resistance holds. Sustained break of 1.2391 will resume larger down trend for 61.8% projection of 1.4376 to 1.2391 from 1.3381 at 1.2154 next. Though, break of 1.2579 will indicate short term bottoming and bring stronger rebound back to 1.2783 resistance. In this case, consolidation from 1.2391 would extend with another rise, towards 1.3381 resistance, before completion.

In the bigger picture, down trend from 1.4376 (2018 high) is still in progress. Break of 1.2391 would target a test on 1.1946 long term bottom (2016 low). For now, we don’t expect a firm break there yet. Hence, focus will be on bottoming signal as it approaches 1.1946. In any case, medium term outlook will stay bearish as long as 1.3381 resistance holds, in case of strong rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | Wholesale Trade Sales M/M May | 0.50% | 1.70% |

{kind=link}