Yen and Swiss Franc extends last week’s strong rally as risk aversion dominates Asian markets. A key trigger is the free fall in the Chinese Yuan, which dives through psychologically important 7 level against Dollar, in response to trade war escalations. Major Asian indices are all in deep red while treasury yields also tumble. In the currency markets, Australian Dollar is the second weakest, followed by New Zealand and then Canadian. Dollar is mixed for now.

technically, downside momentum in Yen crosses is generally strong. USD/JPY breaches 105.83 projection level and is on track to retest 104.69 low. EUR/JPY also breaks 118.07 projection and is on track to 114.84 low. Similarly, though a bit far, GBP/JPY is on track to 122.36 low. EUR/GBP could be a focus today as buying picks up momentum. Focus is on 0.9190 temporary top and break will resume recent rally.

In Asia, Nikkei closed down -1.95%. Hong Kong HSI is down -2.74%. China Shanghai SSE is down -0.92%. Singapore Strait Times is down -1.85%. Japan 10-year JGB yield is down -0.0231 at -0.188.

Chinese Yuan dives through 7 as China seen as weaponizing it in trade war

Chinese Yuan dropped sharply in Asian session partly in response to trade war escalation with US. The PBoC set its daily reference rate at just a slightly weaker level than 6.9 for the first time since December. By USD/CNH (offshore Yuan) then surged to a new low at 7.111, break through the psychological level of 7 decisively. In the stock markets, Nikkei is currently down -2.30%. Hong Kong HSI down -2.89%. China Shanghai SSE down -0.81%. Singapore Strait Times down -1.83%.

Last week, Trump announced to impose 10% tariffs on USD 300B of effectively all untaxed Chinese imports, starting September 1. China responded with hard-line rhetorics. Also, Bloomberg reported that the government has asked its state-owned enterprises to suspend imports of US agricultural products. The developments suggested a return to ti-for-tax retaliations and suspension of trade talks.

Meanwhile, today’s free fall in Yuan argues firstly that the Chinese government is seeing no need to keep Yuan exchange rate stable. Further, it’s a sign that Beijing is weaponizing the Yuan as a tool to offset the impact of tariffs in trade war.

China Caixin PMI services dropped to 51.8, economic slowdown under control

China Caixin PMI Services dropped to 51.8 in July, down from 52.0 and missed expectation of 52.0. PMI Composite rose slightly from 50.6 to 50.9. Markit noted that manufacturing sector stabilized but service sector growth weakened further. Total new work expanded at a slightly faster pace. Also, optimism regarding future output improved to three- month high.

Dr. Zhengsheng Zhong, Director of Macroeconomic Analysis at CEBM Group said: “In general, China’s economy showed signs of recovery in July, thanks to large-scale tax and fee cuts, as well as ongoing support from monetary policy and government-driven infrastructure investment. It remains to be seen if the economic recovery can continue amid trade fictions with the U.S. and rigid regulations on the financial sector and debt levels. The recovery in July suggests that China’s economic slowdown is under control.”

Australia AiG Performance of Services dropped sharply to 43.9, largest monthly decline since 2018

Australia AiG Performance of Services dropped sharply to 43.9 in July, down from 52.2. The -8.3 pts fall is the largest monthly decline since July 2018. Reading below 50 signaled a return to contraction, as trading conditions for many businesses dived again.

Looking at some details, among the business-oriented sectors, only wholesale trade reported positive results. Among the consumer-oriented segments, the large ‘health, education & community services’ sector was strongest. The retail trade sector continued to perform very weakly.

Also from Australian, TD securities inflation gauge rose 0.3% mom in July.

The week ahead: RBNZ to cut, RBA to hold

Two central banks will meet this week. RBNZ is generally expected to cut OCR by -25bps to 1.25%. RBA, on the other hand, is expected to stand pat after two back-to-back rate cuts in June and July. Both central banks are expected to ease monetary policies further in the latter part of the year. Thus, their statements and economic outlook will be watched to affirm such expectations. In addition, BoJ will release summary of opinions while ECB will release monthly economic bulletin.

On the data front, US ISM services; UK PMI services, GDP and productions; Canada employment; New Zealand employment; Australia trade balance; China trade balance will be closely watched. But the tone of the markets are already set, global slowdown, trade war escalation and increasing risks of no-deal Brexit. Those data are unlikely to turn around bearish sentiments. Instead, downside surprises in the data could trigger more bearish sentiments towards respective currency.

Some highlights for the week again.

- Monday: China Caixin PMI services; Swiss SECO consumer climate, retail sales; Eurozone PMI services final, Sentix investor confidence; UK PMI services; US ISM non-manufacturing.

- Tuesday: New Zealand employment, labor cost, RBNZ inflation expectations; Japan average cash earnings, household spending, leading indicators; Australia trade balance, RBA rate decision; Germany factory orders.

- Wednesday: Australia, home loans, AiG construction index; RBNZ rate decision; BoJ summary of opinions; German industrial production; Swiss foreign currency reserves; Canada Ivey PMI.

- Thursday: UK RICS house price balance; Japan current account; China trade balance; ECB monthly bulletin; Canada new housing price index; US jobless claims.

- Friday: Japan GDP; RBA monetary policy statement; China CPI, PPI; Swiss unemployment rate; Germany trade balance; UK GDP, productions, trade balance; Canada housing starts, building permits, employment; US PPI.

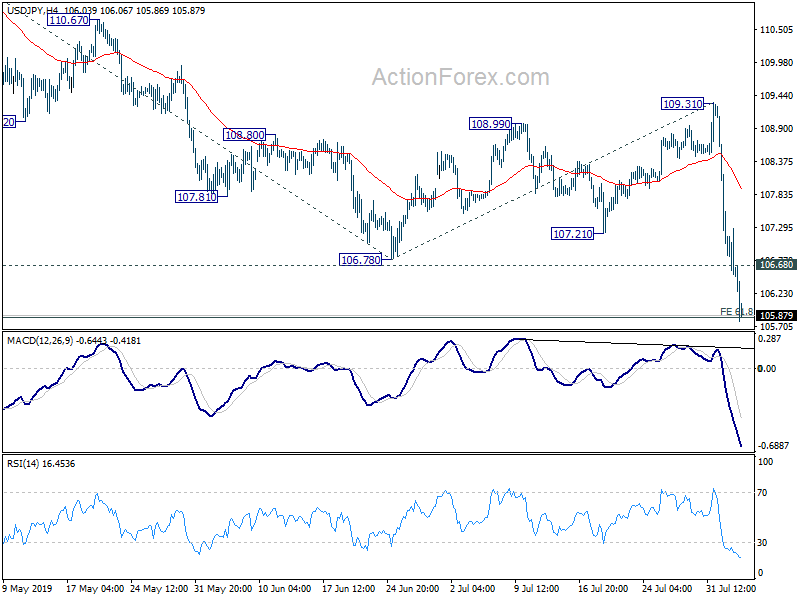

USD/JPY Daily Outlook

Daily Pivots: (S1) 106.22; (P) 106.89; (R1) 107.28; More…

USD/JPY’s decline continues today and reaches as low as 105.78 so far. 61.8% projection of 112.40 to 106.78 from 109.31 at 105.83 is breached but there is no sign of bottoming yet. Intraday bias stays on the downside at this point. Sustained break of 105.83 will pave the way to retest 104.69 low. On the upside, break of 106.68 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, decline from 118.65 (Dec 2016) not completed yet, with the pair staying inside long term falling channel. Break of 104.62 will target 100% projection of 118.65 to 104.62 from 114.54 at 100.51. For now, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. In any case, break of 112.40 is needed to the first serious sign of medium term bullishness. Otherwise, further decline will remain in favor in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | AUD | AiG Performance of Service Index Jul | 43.9 | 52.2 | ||

| 1:00 | AUD | TD Securities Inflation M/M Jul | 0.30% | 0.00% | ||

| 1:45 | CNY | Caixin PMI Services Jul | 51.8 | 52 | 52 | |

| 5:45 | CHF | SECO Consumer Confidence Jul | -8 | -6 | ||

| 6:30 | CHF | Retail Sales Real Y/Y Jun | -1.70% | |||

| 7:45 | EUR | Italy Services PMI Jul | 50.6 | 50.5 | ||

| 7:50 | EUR | France Services PMI Jul F | 52.2 | 52.2 | ||

| 7:55 | EUR | Germany Services PMI Jul F | 55.4 | 55.4 | ||

| 8:00 | EUR | Eurozone Services PMI Jul F | 53.3 | 53.3 | ||

| 8:30 | EUR | Eurozone Sentix Investor Confidence Aug | -7 | -5.8 | ||

| 8:30 | GBP | Services PMI Jul | 50.4 | 50.2 | ||

| 13:45 | USD | US Services PMI Jul F | 52.2 | |||

| 14:00 | USD | ISM Non-Manufacturing/Services Composite Jul | 55.5 | 55.1 |

{kind=link}