Swiss Franc and Yen weaken broadly again today as risk appetite returns to markets. In particular, US stocks are set to challenge record high, on trade optimism, as well as expectation of another Fed rate cut. European stocks, except FTSE, also rise mildly as EU agreed on a three-month Brexit flextension. Staying in the currency markets, Euro is currently the strongest for today, followed by Australian Dollar.

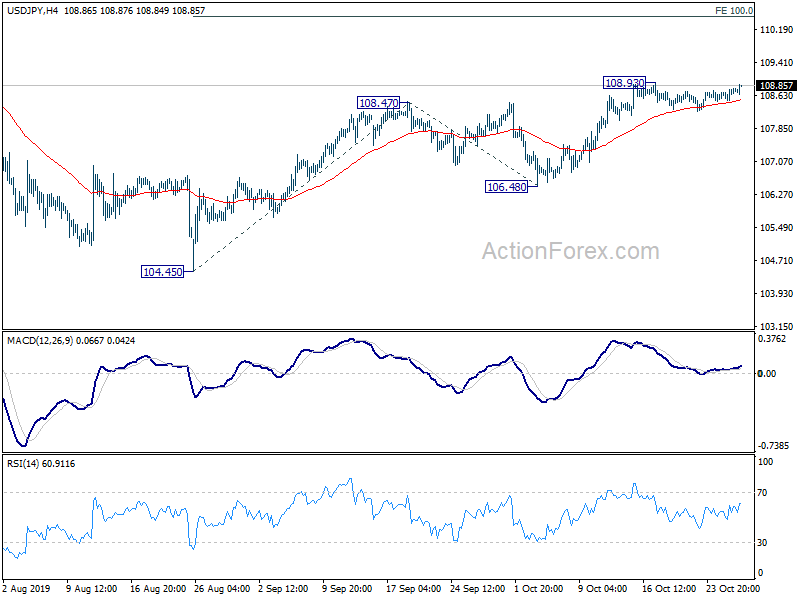

Technically, USD/JPY will likely challenge 108.93 temporary top. Break will resume recent rise from 104.45 to 109.31 key structural resistance next. USD/CHF is on track to retest 1.0027 resistance. EUR/CHF will be a pair to watch today. It’s staying below 1.1062 key cluster resistance so far, even though the choppy recovery form 1.0811 extended. Sustained break of 1.1062 will carry larger bullish implication and be an early sign of trend reversal. Focus will immediately be back on 1.1162 support turned resistance. That will be a strong sign of easing medium term risk aversion.

In Europe, FTSE is up 0.02%. DAX is up 0.47%. CAC is up 0.23%. German 10-year yield is up 0.022 at -0.34. Earlier in Asia, Nikkei rose 0.30%. Hong Kong HSI rose 0.84%. China Shanghai SSE rose 0.85%. Japan 10-year JGB yield rose 0.0136 to -0.132.

US goods trade deficit narrowed to USD 70.4B, down -3.6%

US goods trade deficit narrowed by -3.6% mom to USD -70.4B in September, down USD -2.7B from October’s 73.1B. Exports of goods were USD 135.9B, USD 2.2B less than August exports. Imports of goods were USD 206.3B, USD 4.9 than August imports. Advanced wholesale inventories dropped -0.3% mom in September, versus expectation of 0.3% mom.

EU Tusk confirmed approval of 3-month Brexit flextension

European Council President Donald Tusk announced that EU27 has agreed that it will accept UK’s request for Brexit “flextension” until January 31, 2020. He expected to formalize the decision through a written procedure. The decision was made after a 30-minutes meeting of European ambassadors. It’s reported that the conditions attached to the extension including the “non-renegotiability” of the deal agreed.

UK CBI retail sales rose to -10, retailers contend with looming Brexit deadline

UK CBI realized sales improved to -10 in October, but remained in decline for the sixth consecutive months. Rain Newton-Smith, CBI Chief Economist, said: “Retailers have now endured six months of falling sales, the longest period of decline since the financial crisis. The sector is struggling with ongoing digital disruption, layered on top of cost pressures from a weak pound and the cumulative burden of an outdated business rates regime.

“Retailers have also had to contend with the looming Brexit deadline, which has partly driven a record spike in stocks. The timing could not be worse: the run-up to Christmas is a crucial time of year for the retail sector, and not knowing where we will be on November 1st is adding more strain to an already beleaguered sector.”

Also released, Eurozone M3 money supply rose 5.5% yoy in September, below expectation of 5.7% yoy. Germany import price rose 0.6% mom in September, much higher than expectation of 0.1% mom.

Former BoJ Shirakawa saw Japanification of policy in the world

Former BoJ Governor Masaaki Shirakawa said in a summit in Shanghai that there is a “Japanification” of monetary and fiscal policy in the world. And, “policy makers and mainstream academics are still obsessed with a specter of deflation.” He added that the goal of monetary and fiscal stimulus should only be to “bring future demand to the present”. But, “the capacity to front-load will be restrained by the country’s potential growth rate, which will be kept low as perpetual low interest rates keep inefficient firms alive.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.53; (P) 108.65; (R1) 108.79; More…

At this point, intraday bias in USD/JPY remains neutral first, with focus on 108.93 temporary top. Break there will resume recent rise from 104.45. Intraday bias will be turned back to the upside for 109.31 key resistance. Decisive break there will carry larger bullish implications next target will be 100% projection of 104.45 to 108.47 from 106.48 at 110.50. On the downside, in case of another retreat, downside should be contained by 55 day EMA (now at 107.85) to bring rebound.

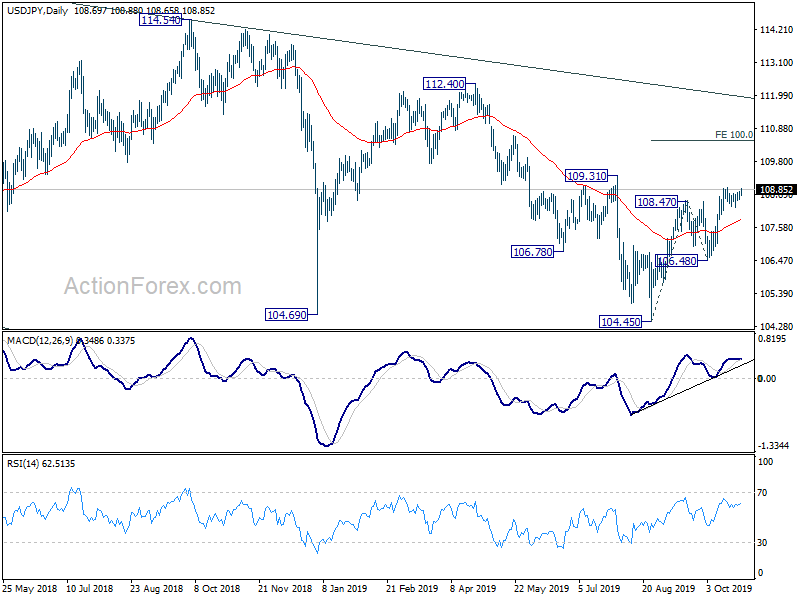

In the bigger picture, strong support was seen from 104.62 again. Yet, there is no confirmation of medium term reversal. Corrective decline from 118.65 (Dec. 2016) could still extend lower. But in that case, we’d expect strong support above 98.97 (2016 low) to contain downside to bring rebound. Meanwhile, on the upside, break of 112.40 key resistance will be a strong sign of start of medium term up trend.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Corporate Service Price Index Y/Y Sep | 0.50% | 0.50% | 0.60% | 0.50% |

| 07:00 | EUR | Germany Import Price Index M/M Sep | 0.60% | 0.10% | -0.60% | |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Sep | 5.50% | 5.70% | 5.70% | 5.80% |

| 11:00 | GBP | CBI Realized Sales M/M Oct | -10 | -20 | -16 | |

| 12:30 | USD | Wholesale Inventories Aug P | -0.30% | 0.30% | 0.20% | 0.00% |

| 12:30 | USD | Goods Trade Balance (USD) Sep | -70.4B | -73.5B | -72.8B | -73.1B |

{kind=link}