Dollar remains the weakest one for the week as markets head towards weekly close. The greenback was weighed down by a string of weaker than expected economic data. Additionally, as December 15 natural deadline looms, it’s still uncertain whether US and China could complete the phase one trade deal to avert next round of tariffs. The greenback will need some very solid job data from non-farm payrolls to reverse this week’s decline.

Staying in the currency markets, Euro and Yen are currently among the weakest for the week. Canadian Dollar staged a strong rebound as BoC comments lowered the chance of rate cut. But the Loonie is still trading lower for the week against all but Dollar. On the other hand, Sterling and New Zealand Dollars are the strongest ones, followed by Swiss Franc.

In Asia, Nikkei closed up 0.23%. Hong Kong HSI is up 0.98%. China Shanghai SSE is up 0.43%. Singapore Strait Times is up 0.23%. Japan 10-year JGB yield is up 0.0274 at -0.012, very close to 0%. Overnight, DO rose 0.10%. S&P 500 rose 0.15%. NASDAQ rose 0.05%. 10-year yield rose 0.016 to 1.797, failed to regain 1.8 handle.

Dollar index’s medium term outlook depends on non-farm payrolls today

US Non-Farm Payrolls report will be the major focus today. Markets are expecting 183k job growth in November. Unemployment rate is expected to be unchanged at 3.6%. Average hourly earnings growth is expected to pick up to 0.3% mom. Dollar dropped sharply this week as poor ISMs pointed to weaker outlook ahead, and revived speculation of Fed cut next year. A strong set of NFP data today is needed to reverse the greenback’s fortune. Otherwise, selloff might accelerate further.

Other job related data released have been mixed to slightly negative. ISM manufacturing employment dropped from 47.7 to 46.6, suggesting deeper contraction in manufacturing jobs. ISM services employment rose to 55.5, up from 53.7. ADP private sector jobs grew just 67k. The details were also in-line with ISMs’, with goods-producing jobs contracted -18k. Service-providing jobs rose 85k. Four-week moving average of initial claims rose 3k to 217.75k.

Current development now raised the chance that Dollar index’s recovery from 97.10 was only a corrective rise, and has completed at 98.39. Next focus will be 97.10 support. Break there will also have 55 week EMA firmly taken out. In that case, a medium term should be confirmed at 99.66. And, a medium term correction should at least be started towards 38.2% retracement of 88.30 to 99.66 at 95.32.

Japan household spending dropped -5.1%, due to sales tax hike

A batch of economic data is released from Japan today. Overall household spending dropped -5.1% yoy in October, worse than expectation of -3.0% yoy. The decline in spending was the first time in 11 month, and biggest fall since March 2016. It’s also a sharp reversal from the 9.5% rise in September, fastest growth on record.

Apparently, the September and October figures were results of the sales tax hike in October, from 8% to 10%. Additionally, impacts from typhoon also accelerated the decline in spending. Overall spending might contract as a whole Q4, before some moderate pick up in Q1.

Also released, labor cash earnings rose 0.5% yoy in October, above expectation of 0.2% yoy. Leading indicator dropped -0.1 to 91.8, below expectation of 92.0.

Australia AiG construction dropped to 40, 15th straight month of contraction

Australia AiG Performance of Construction Index dropped to 40.0 in November, down from 43.9. The result indicates sharper decline in the construction industry on aggregate. It’s also the 15th straight month of contractionary reading. As AiG said, “this on-going weakness in business conditions was associated with a steeper fall in employment and a continued reduction in deliveries from suppliers.”

Elsewhere

Germany will release industrial production. France will release trade balance. Italy will release retail sales. Swiss will release foreign currency reserves. Later in the day, in addition to US NFP, Canada will also release job data.

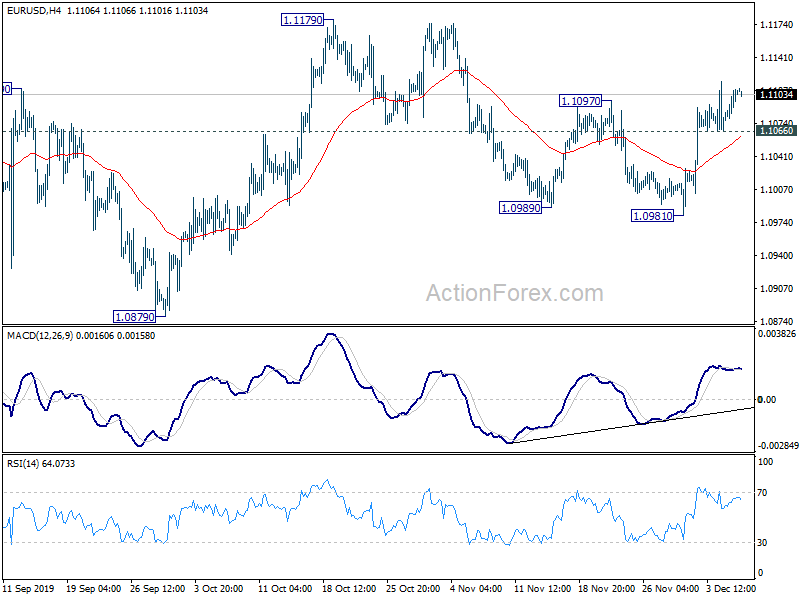

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1085; (P) 1.1097; (R1) 1.1115; More…

Outlook in EUR/USD remains unchanged at this point. With 1.1066 minor support intact, further rise is still in favor. Corrective decline form 1.1179 could have completed at 1.0981. Rise from there would target a test on 1.1179 first. Break will resume whole rally form 1.0879. However, break of 1.1066 will turn bias back to the downside for 1.0981 instead.

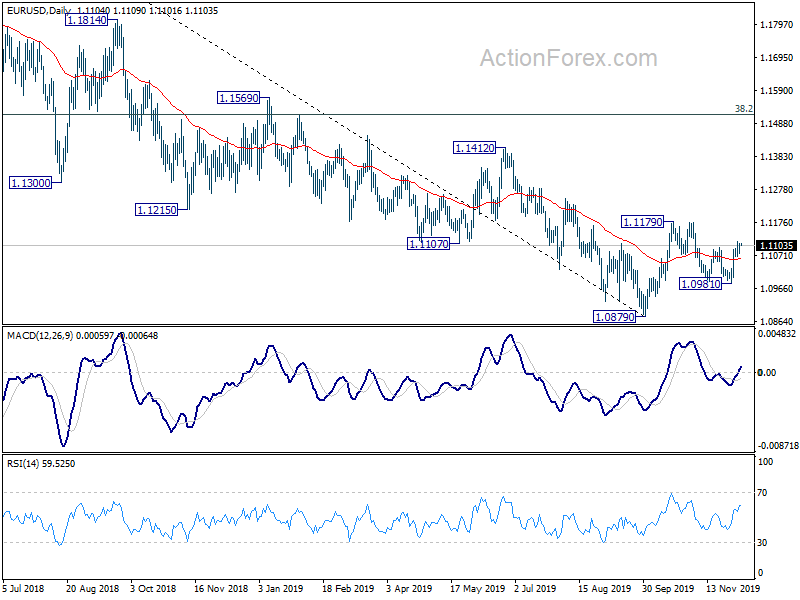

In the bigger picture, rebound from 1.0879 is seen as a corrective move first. In case of another rise, upside should be limited by 38.2% retracement of 1.2555 to 1.0879 at 1.1519. And, down trend from 1.2555 (2018 high) would resume at a later stage. However, sustained break of 1.1519 will dampen this bearish view and bring stronger rise to 61.8% retracement at 1.1915 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Nov | 40 | 43.9 | ||

| 23:30 | JPY | Labor Cash Earnings Y/Y Oct | 0.50% | 0.20% | 0.50% | 0.30% |

| 23:30 | JPY | Overall Household Spending Y/Y Oct | -5.10% | -3.00% | 9.50% | |

| 5:00 | JPY | Leading Economic Index Oct P | 91.8 | 92 | 91.9 | |

| 7:00 | EUR | Germany Industrial Production M/M Oct | 0.20% | -0.60% | ||

| 7:45 | EUR | France Trade Balance (EUR) Oct | -4.8B | -5.6B | ||

| 8:00 | CHF | Foreign Currency Reserves (CHF) Nov | 779B | |||

| 9:00 | EUR | Italy Retail Sales M/M Oct | 0.50% | 0.70% | ||

| 13:30 | USD | Nonfarm Payrolls Nov | 183K | 128K | ||

| 13:30 | USD | Unemployment Rate Nov | 3.60% | 3.60% | ||

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.30% | 0.20% | ||

| 13:30 | CAD | Net Change in Employment Nov | 10.0K | -1.8K | ||

| 13:30 | CAD | Unemployment Rate Nov | 5.50% | 5.50% | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Dec P | 97 | 96.8 | ||

| 15:00 | USD | Wholesale Inventories Oct | 0.20% | 0.20% |

{kind=link}