Canadian Dollar is trading as the strongest one for today, as helped by resilience in oil price and solid consumer inflation data. Dollar is currently following closely as the second strongest. On the other hand, European majors are the weakest ones so far, including Swiss Franc. Though, while Sterling is leading the decline, it’s pull back is starting to slow ahead of near term support against both Dollar and Yen. The Pound shows little reaction to CPI and is now awaiting tomorrow’s BoE rate decision. Euro shrugs off better than expected Germany Ifo.

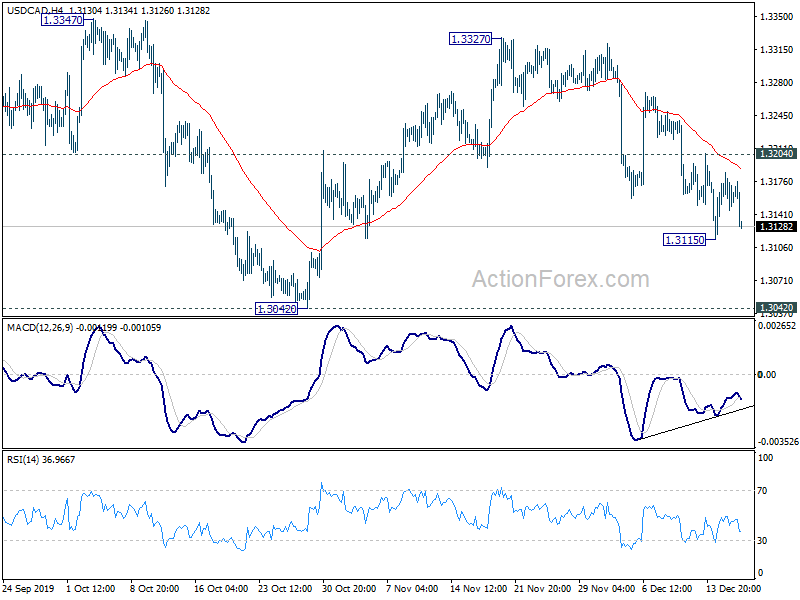

Technically, 109.72 resistance in USD/JPY remains a focus. Break there will resume recent rebound from 104.45. USD/CAD’s focus is now back on 1.3115 temporary low. break will resume the fall from 1.3327 to 1.3042 key support. Outlook is unchanged elsewhere. EUR/USD and AUD/USD are both staying in consolidations. We’d also continue to expect strong support in 1.3050 in GBP/USD and 142.47 in GBP/JPY to complete current retreats and bring rebound.

In Europe, currently, FTSE is up 0.08%. DAX is down -0.31%. CAC is down -0.10%. German 10-yaer yield is up 0.025 at -0.266. Earlier in Asia, Nikkei dropped -0.55%. Hong Kong HSI rose 0.15%. China Shanghai SSE dropped -0.18%. Singapore Strait Times rose 0.2%. Japan 10-year JGB yield dropped -0.0019 to -0.015.

Canada CPI jumped to 2.2% in Nov, ex-gasoline unchanged at 2.3%

Canada CPI accelerated to 2.2% in November, up from 1.9% yoy, matched expectations. Excluding gasoline, CPI rose 2.3%, unchanged from October’s reading. CPI common was unchanged at 1.9% yoy, matched expectations. CPI median rose to 2.4%, up from 2.2%, beat expectation of 2.2% yoy. CPI trimmed accelerated to 2.2% yoy, up from 2.1% yoy, matched expectations.

German Ifo rose to 96.3, more confident into new year

German Ifo Business Climate rose to 96.3 in December, up from 95.0, beat expectation of 95.5. Current Assessment Index rose to 98.8, up from 97.9, beat expectation of 98.1. Expectation Index rose to 93.8, up from 92.1, beat expectation of 93.1. “The German economy is heading into the New Year with more confidence,” Ifo President Clemens Fuest said.

Looking at some details, manufacturing improved from -5.8 to -5.0. Service rose from 17.4 to 21.3. However, trade dropped from 0.9 to 0. Construction also dropped from 20.3 to 17.9.

Eurozone CPI finalized at 1.0%, core CPI at 1.3%

Eurozone CPI was finalized at 1.0% yoy in November, up from October’s 0.7% yoy. Core CPI was finalized at 1.3% yoy, up from October’s 1.1%. The highest contribution came from services (+0.82%), followed by food, alcohol & tobacco (+0.37%), non-energy industrial goods (+0.10%) and energy (-0.33%).

EU28 CPI was finalized at 1.3%, core CPI at The lowest annual rates were registered in Italy, Portugal (both 0.2%) and Belgium (0.4%). The highest annual rates were recorded in Romania (3.8%), Hungary (3.4%), Slovakia (3.2%) and Czechia (3.0%).

Coeure: ECB could communicate the range of inflation outcomes as target

Outgoing ECB Executive Board Member Benoit Coeure said in farewell event today that the central bank should be more flexible with its inflation target. He said, “the ECB should clarify that it aims to deliver inflation of 2% over the medium term. And it could communicate the range of inflation outcomes that can be considered acceptable in normal times.”

A band around the target wouldn’t weaken the central bank’s resolve. He added, “research shows that central banks have a strong incentive to already respond to inflation deviations within the tolerance zone, rather than waiting until inflation has crossed the edges.”

UK CPI unchanged at 1.5%, core CPI at 1.7%

UK CPI was unchanged at 1.5% yoy in November. Core CPI was also unchanged at 1.70%. Both matched expectations. RPI accelerated to 2.2% yoy, up from 2.1% yoy, beat expectation of 2.1% yoy.

PPI input came in at -0.3% mom, -2.7% yoy, versus expectation of -1.2% mom, -4.9% yoy. PPI output was at -0.2% mom, 0.5% yoy, versus expectation of 0.0% mom, 0.9% yoy. PPI output core was at -0.1% mom, 1.1% yoy, versus expectation of 0.1% mom, 1.5% yoy.

Japan export contracted for 12-straight months

In non-seasonally adjusted terms, Japan’s exports dropped -7.9% yoy to JPY 6.38T in November. Even though that’s a smaller than expected decline, it still marked the 12-month straight month of contraction. Exports were dragged down by cars and construction equipment to the US, as well as shipment of chemical production to China. Imports dropped -15.7% yoy to JPY 6.46T. Trade surplus dropped sharply by -88.9% yoy to JPY 0.082T.

In seasonally adjusted terms, exports dropped -0.3% mom to JPY 6.28T. Imports dropped -0.1% mom to JPY 6.35T. Trade deficit came in at JPY -0.06T.

Asian business sentiment swung from decade low to 18-month high

Thomson Reuters/INSEAD Asian Business Sentiment jumped to 71 in Q4. That was a large swing from Q3’s 58, which was close a decade low, to the highest since June last year. The change was also a noticeable shift from neutral to optimistic even though majority of firms are not yet confident enough to plan hiring.

Antonio Fatas, economics professor at INSEAD, said, “conditions, expectations and some of the uncertainty has improved over the last quarter. But I don’t see this uncertainty disappearing, I think some of these tensions are going to stay with us maybe for years or decades.”

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3144; (P) 1.3164; (R1) 1.3183; More….

USD/CAD dips notably in early US session but stays above 1.3115 temporary low. Intraday bias remains neutral first. Further fall is expected as long as 1.3204 holds. Below 1.3115 will resume the decline from 1.3327 and target 1.3042 key support. Decisive break there will carry larger bearish implication. On the upside, above 1.3204 minor resistance will turn bias back to the upside for 1.3327 resistance instead.

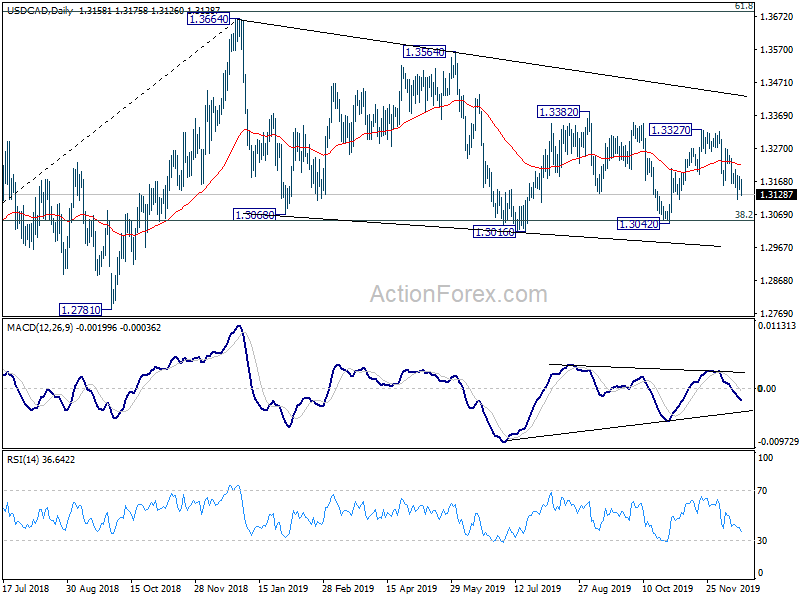

In the bigger picture, 38.2% retracement of 1.2061 to 1.364 at 1.3052 remains intact. Medium term rise from 1.2061 low is in favor to resume sooner or later. Firm break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 will confirm and target 1.4689 high. However, sustained break of 1.3052 will confirm completion of up trend from 1.2061 (2017 low). Further fall should be seen to 61.8% retracement at 1.2673 next.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Current Account (NZD) Q3 | -6.35B | -6.32B | -1.11B | -1.04B |

| 23:50 | JPY | Trade Balance (JPY) Nov | -0.06T | -0.06T | -0.03T | -0.05T |

| 00:30 | AUD | Westpac Leading Index M/M Nov | -0.09% | -0.08% | -0.15% | |

| 07:00 | EUR | Germany PPI M/M Nov | 0.00% | 0.10% | -0.20% | |

| 07:00 | EUR | Germany PPI Y/Y Nov | -0.70% | -1.10% | -0.60% | |

| 09:00 | EUR | Germany IFO – Business Climate Dec | 96.3 | 95.5 | 95 | |

| 09:00 | EUR | Germany IFO – Current Assessment Dec | 98.8 | 98.1 | 97.9 | |

| 09:00 | EUR | Germany IFO – Expectations Dec | 93.8 | 93.1 | 92.1 | |

| 09:30 | GBP | DCLG House Price Index Y/Y Oct | 0.70% | 1.60% | 1.30% | |

| 09:30 | GBP | CPI M/M Nov | 0.20% | 0.20% | -0.20% | |

| 09:30 | GBP | CPI Y/Y Nov | 1.50% | 1.50% | 1.50% | |

| 09:30 | GBP | Core CPI Y/Y Nov | 1.70% | 1.70% | 1.70% | |

| 09:30 | GBP | RPI M/M Nov | 0.20% | 0.10% | -0.20% | |

| 09:30 | GBP | RPI Y/Y Nov | 2.20% | 2.10% | 2.10% | |

| 09:30 | GBP | PPI – Input M/M Nov | -0.30% | -1.20% | -1.30% | -1.10% |

| 09:30 | GBP | PPI – Input Y/Y Nov | -2.70% | -4.90% | -5.10% | -5.00% |

| 09:30 | GBP | PPI – Output M/M Nov | -0.20% | 0.00% | -0.10% | |

| 09:30 | GBP | PPI – Output Y/Y Nov | 0.50% | 0.90% | 0.80% | |

| 09:30 | GBP | PPI – Core Output M/M Nov | -0.10% | 0.10% | -0.10% | |

| 09:30 | GBP | PPI – Core Output Y/Y Nov | 1.10% | 1.50% | 1.30% | |

| 10:00 | EUR | Eurozone CPI Y/Y Nov F | 1.00% | 1.00% | 1.00% | |

| 10:00 | EUR | Eurozone CPI – Core Y/Y Nov F | 1.30% | 1.30% | 1.30% | |

| 13:30 | CAD | CPI M/M Nov | -0.10% | -0.10% | 0.30% | |

| 13:30 | CAD | CPI Y/Y Nov | 2.20% | 2.20% | 1.90% | |

| 13:30 | CAD | CPI Common Y/Y Nov | 1.90% | 1.90% | 1.90% | |

| 13:30 | CAD | CPI Media Y/Y Nov | 2.40% | 2.20% | 2.20% | |

| 13:30 | CAD | CPI Trimmed Y/Y Nov | 2.20% | 2.20% | 2.10% | |

| 16:00 | USD | Crude Oil Inventories | -1.5M | 0.8M |

{kind=link}