Risk aversion on fear of Wuhan coronavirus pandemic continues to be the main theme in the financial markets. DOW lost over -1000 pts overnight as it’s suffering one of the worst weeks in history. 10-year and 30-year yield hit new record lows. Asian markets naturally follow with all major indices in deep red. Oil price is suggesting its biggest weekly loss since 2014, could prompt counter measures from OPEC+.

In the currency markets, Canadian Dollar is the worst performing one for the week so far, thanks to free fall in oil prices. New Zealand and Australian Dollars are not too far away. Yen is currently the strongest, as risk aversion overshadows worries over Japan’s economy. Euro is following as the second strongest, with help from strong rally against Dollar and Sterling. The greenback is mixed as expectation of March Fed cut soared.

In Asia, currently, Nikkei is down -3.48%. Hong Kong HSI is down -2.52%. China Shanghai SSE is down -2.74%. Singapore Strait Times is down -2.28%. Japan 10-year JGB yield is down -0.0297 at -0.l132. Overnight, DOW dropped -4.42%. S&P 500 dropped -4.42%. NASDAQ dropped -4.61%. 10-year yield dropped to -0.011 to 1.299, new record low.

Global coronavirus spread intensifies as WHO called for swift and aggressive actions

While new Wuhan coronavirus cases appeared to have slowed to the lowest pace since January, global spread is intensifying. In China, there were 327 new confirmed cases of the coronavirus on Thursday, as reported by the National Health Commission, bringing the total to 78824. Death toll rose 44 to 2788.

umber of cases in South Korea broke 2000 level to 2022, with 13 deaths. Italy’s number of cases spiked by more than 50% in just 24 hours, hitting 650, with 17 deaths. Iran’s number rose to 245, with 26 deaths. An Iranian vice president is infected with six other officials. Iran’s former ambassador to the Vatican died of the coronavirus In Japan, total cases reached 210, with 4 deaths, prompted the government to close all schools for a month.

World Health Organization director-general Tedros Adhanom Ghebreyesus warned that “every country must be ready for its first case.” “We’re at a decisive point,” he said. “The epidemics in the Islamic Republic of Iran, Italy and the Republic of Korea demonstrate what this virus is capable of.” He also urged swift and aggressive actions and the preparations will be “the difference between one case and 100 cases in the coming days and weeks.”

Less than a month ago, when the outbreak was mostly confined within China, Tedros urged countries not to impose travel restrictions on people coming out of China. He called the global spread “minimal and slow” back then. over 420k people have signed a petition to call for resignation of Tedros for breaking political neutrality in his handling of the outbreak.

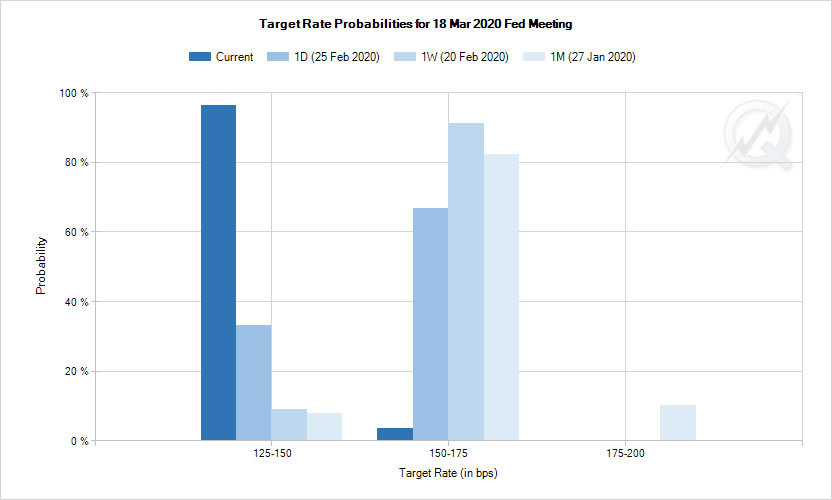

March Fed cut odds jumped to 96%, Dollar index pressure

Expectation of a Fed policy easing surged this week, as it could be forced to prepare for global recession, including the US, while Wuhan coronavirus pandemic worsen. Fed funds futures are currently pricing in 96.3% of a 25bps cut to 1.25-1.50% at March FOMC meeting. A month ago, that was less than 9% chance.

Dollar index’s pull back from 99.91 is deeper than expected, with 38.2% retracement of 96.35 to 99.91 at 98.55. That’s a natural result as the greenback is being sold off against both Euro and yen. While further fall is likely for the near term, strong support is now expected between 61.8% retracement at 97.71 and 55 day EMA at 98.26 to contain downside to bring rebound. That should happen at least for the first downside attempt in the area.

DOW selloff extended, heading to 24175 fibonacci level

DOW selloff was way worse than we initially thought. 55 week EMA was taken out without any hesitation. Bearish divergence condition in weekly MACD suggests that it’s set up for further correction. From pure technically point of view, current fall could extend to 38.2% retracement of 15450.56 to 29568.57 at 24175.49, which is close to long tem trend line support, before have enough support for sustainable rebound.

Mixed data from Japan while Abe pledges to “watch” coronavirus developments carefully

A batch of mixed economic data is released from Japan today. Industrial production rose 0.8% mom versus expectation of 0.4% mom. According to the survey by the Ministry of Economy, Trade and Industry, manufacturers expected output to growth 5.3% in February and than shrink sharply by -6.9% in March. However, unemployment rate jumped to 2.4% versus expectation of being unchanged at 2.2%. Tokyo CPI core slowed to 0.5% yoy in February, down from 0.7% yoy, missed expectation of 0.6% yoy.

Prime Minister Shinzo Abe pledged to take policy steps is needed to shield the economy from the impact of coronavirus outbreak. He said “if the virus spread, it could have a huge impact on the economy. And, “we’re therefore watching developments carefully.” He added, Japan has “reserves to tap for virus response”. But there is “no immediate need for additional funding” yet.

Elsewhere

UK Gfk consumer confidence improved to -7 in February, up form -9. Australia private sector credit rose more than expected by 0.3% mom in January. The economic calendar is buys today. Swiss will release KOF and retail sales. Germany will release import price, unemployment and CPI. US will release PCE inflation, goods trade balance, Chicago PMI, Michigan U sentiment and wholesale inventories. Canada will release GDP, RMPI and IPPI.

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3340; (P) 1.3367; (R1) 1.3416; More….

USD/CAD’s rally accelerates to as high as 1.3436 so far and intraday bias stays on the upside. Triangle consolidation from 1.3664 has completed at 1.2951. Break of 61.8% projection of 1.2951 to 1.3329 from 1.3202 at 1.3436 will pave the way to 100% projection at 1.3580 next. On the downside, below 1.3374 minor support will turn intraday bias neutral first. But retreat should be contained above 1.3202 support to bring rally resumption.

In the bigger picture, price actions from 1.3664 (2018 high) is seen as a corrective move that has likely completed. Rise from 1.2061 (2017 low) might be ready to resume. Decisive break of 61.8% retracement of 1.4689 (2016 high) to 1.2061 at 1.3685 will pave the way to retest 1.4689 high. However, break of 1.3202 support could extend the corrective with another fall through 1.2951 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Core Y/Y Feb | 0.50% | 0.60% | 0.70% | |

| 23:30 | JPY | Unemployment Rate Jan | 2.40% | 2.20% | 2.20% | |

| 23:50 | JPY | Industrial Production M/M Jan P | 0.80% | 0.40% | 1.20% | |

| 23:50 | JPY | Retail Trade Y/Y Jan | -0.40% | -1.10% | -2.60% | |

| 00:01 | GBP | GfK Consumer Confidence Feb | -7 | -8 | -9 | |

| 00:30 | AUD | Private Sector Credit M/M Jan | 0.30% | 0.20% | 0.20% | |

| 05:00 | JPY | Housing Starts Y/Y Jan | -6.10% | -7.90% | ||

| 07:00 | EUR | Germany Import Price Index M/M Jan | 0.20% | 0.20% | ||

| 07:30 | CHF | Real Retail Sales Y/Y Jan | 0.30% | 0.10% | ||

| 07:45 | EUR | France GDP Q/Q Q4 | -0.10% | -0.10% | ||

| 08:00 | CHF | KOF Leading Indicator Feb | 97 | 100.1 | ||

| 08:55 | EUR | Germany Unemployment Rate Feb | 5% | 5% | ||

| 08:55 | EUR | Germany Unemployment Change Feb | -3K | -2K | ||

| 13:00 | EUR | Germany CPI M/M Feb P | 0.30% | -0.60% | ||

| 13:00 | EUR | Germany CPI Y/Y Feb P | 1.70% | 1.70% | ||

| 13:30 | USD | Personal Income M/M Jan | 0.30% | 0.20% | ||

| 13:30 | USD | Personal Spending Jan | 0.30% | 0.30% | ||

| 13:30 | USD | PCE Price Index M/M Jan | 0.30% | |||

| 13:30 | USD | PCE Price Index Y/Y Jan | 1.60% | |||

| 13:30 | USD | Core PCE Price Index M/M Jan | 0.20% | 0.20% | ||

| 13:30 | USD | Core PCE Price Index Y/Y Jan | 1.70% | 1.60% | ||

| 13:30 | USD | Goods Trade Balance (USD) Jan | -68.5B | -68.3B | ||

| 13:30 | USD | Wholesale Inventories Jan P | -0.20% | |||

| 13:30 | CAD | GDP M/M Dec | 0.10% | 0.10% | ||

| 13:30 | CAD | Raw Material Price Index Jan | 2.80% | |||

| 13:30 | CAD | Industrial Product Price M/M Jan | 0.10% | |||

| 14:45 | USD | Chicago PMI Feb | 45.3 | 42.9 | ||

| 15:00 | USD | Michigan Consumer Sentiment Index Feb | 100.9 | 100.9 |