Sterling weakness remains the unified theme in the markets this week. The Pound remain under pressure in Asian session today while recovery attempt was brief and weak. As for the week, Canadian Dollar is currently the second weakest, in tandem with the sharp decline in oil price. Swiss Franc and Yen are the strongest so far, with help from risk aversion. Dollar and Euro are markets. There is no follow through buying in Euro after that post ECB bounce. Dollar is also hesitating to take a clear direction.

Technically, US stocks could be the main focus before weekly close. NASDAQ’s 01.99% decline overnight dragging it back to key support zone between 55 day EMA and 23.6% retracement of 6631 to 120734. A firm break there would confirm that fall from 12074 is actually corrective the whole rise from 6631. Deeper fall could then be seen to 38.2% retracement at 9994.97 at least. In that case, risk aversion should stay for a longer while, providing some extra lift to Yen and Dollar.

In Asia, Nikkei closed up 0.74%. Hong Kong HSI is up 0.70%. China Shanghai SSE is up 0.79%. Singapore Strait Time is down -0.39%. Japan 10-year JGB yield is down -0.0025 at 0.027. Overnight, DOW dropped -1.45%. S&P 500 dropped -1.76%. NASDAQ dropped -1.99%. 10-year yield dropped -0.018 to 0.685.

ECB Lane: Recent appreciation of euro exchange rate dampens inflation outlook

In a blog post, ECB Chief Economist Philip Lane said “recent appreciation of the euro exchange rate dampens the inflation outlook.” “Headline inflation is expected to remain persistently low over the medium term, notwithstanding a gradual pick-up over the projection horizon.”

“Inflation remains far below the aim and there has been only partial progress in combating the negative impact of the pandemic on projected inflation dynamics,” he added. “Moreover, the outlook remains subject to high uncertainty and the balance of risks continues to be tilted to the downside.”

UK GDP grew 6.6% in July, still -11.7% lower than pre-pandemic levels

UK GDP grew 6.6% mom in July, just slightly below expectation of 6.7% mom. It’s the third consecutive of increase in GDP. But only around half of the pandemic loss was recovered so far. Also, monthly GDP in July was -11.7% lower than the pre-pandemic levels seen in February.

ONS director of economic statistics Darren Morgan said: “While it has continued steadily on the path towards recovery, the UK economy still has to make up nearly half of the GDP lost since the start of the pandemic…. All areas of manufacturing, particularly distillers and car makers, saw improvements, while housebuilding also continued to recover. However, both production and construction remain well below previous levels.”

Looking at some details, index of services rose 6.1% mom in July. Index of production rose 5.2% mom. Manufacturing rose 6.3% mom. Construction rose 17.6% mom. Agriculture rose 1.1% mom.

Japan Motegi to conclude trade deal with UK today

Japan Foreign Minister Toshimitsu Motegi indicated he will speak to UK Trade Minister Liz Truss today to conclude the post-Brexit trade agreement. That, if agreed, would come just before Prime Minister Shinzo Abe steps down on September 15 for health reason.

The bilateral trade agreement is expected to largely replicate the Japan-EU agreement. UK expects to deal to increase trade with Japan by around GBP 15B a year in the long run.

Released from Japan, BSI large manufacturing conditions index rose to 0.1 in Q3, much improvement from -52.3. PPI picked up to -0.5% yoy in August, from -0.9% yoy.

New Zealand BusinessNZ manufacturing dropped back to 50.7 on lockdown return

New Zealand BusinessNZ Manufacturing PMI dropped sharply to 50.7 in August, down from 59.0. Looking at some details, productions dropped form 61.8 to 51.1. Employment improved from 46.9 to 49.0. New orders tumbled from 67.5 to 54.0.

BusinessNZ’s executive director for manufacturing Catherine Beard said, “After two months of playing catch-up, the level 3 lockdown placed on New Zealand’s largest population and economic region meant the sector would experience another hit. While results in other parts of the country led to the national result keeping its head above water, the latest results show how fragile and short the recovery can be.”

BNZ Senior Economist, Doug Steel said that “an outcome above the 50 breakeven mark – indicating a modicum of growth occurred in the month – is arguably a commendable result given more than a third of the country moved into alert level 3 for more than half of the month.”

Elsewhere

Germany CPI was finalized at -0.1% mom, 0.0% yoy in August. US CPI will be a major focus for today. Canada will release capacity utilization.

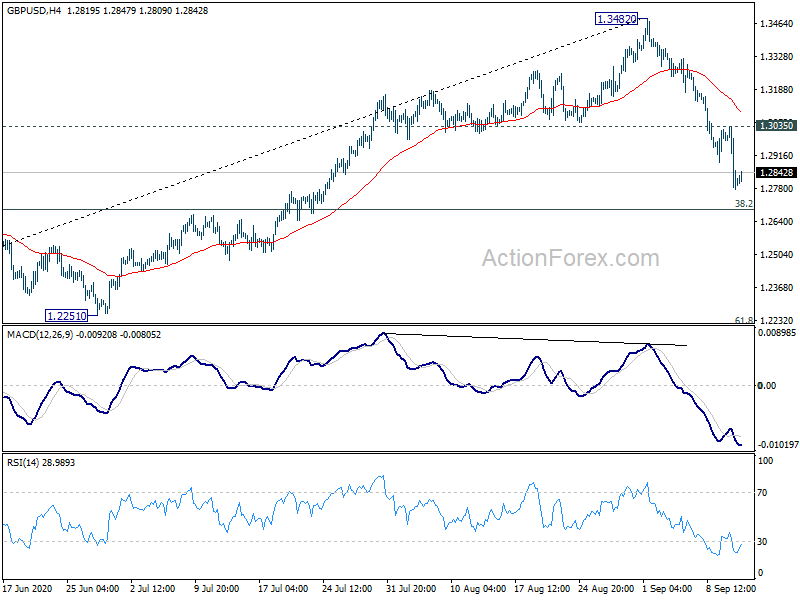

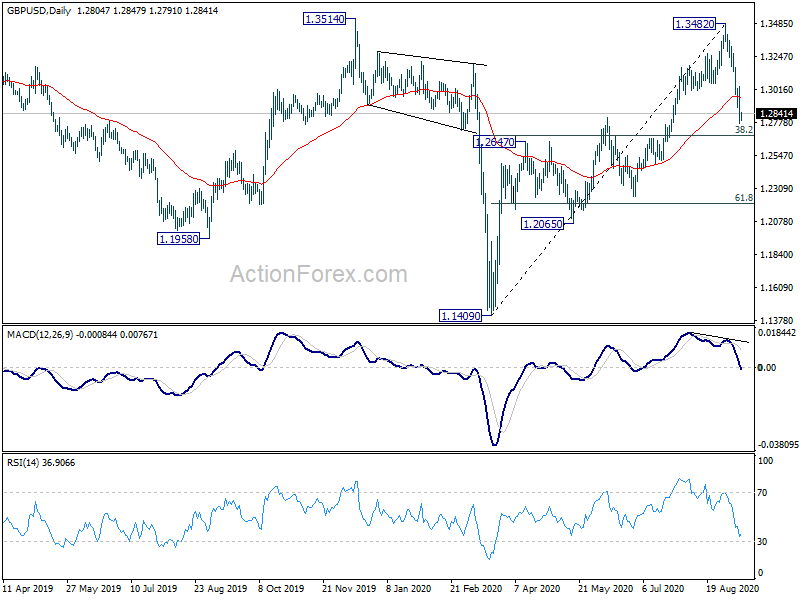

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2715; (P) 1.2875; (R1) 1.2976; More….

GBP/USD’s fall from 1.3482 resumed after brief recovery and hits as low as 1.2773 so far. Intraday bias is back on the downside for 38.2% retracement of 1.1409 to 1.3482 at 1.2690. Strong rebound from there will suggest that such decline is merely a corrective move. Break of 1.3035 minor resistance will turn bias back to the upside for rebound. However, sustained break of 1.2690 will argue that the rise from 1.1409 might be completed, and bring deeper fall to 61.8% retracement at 1.2201.

In the bigger picture, immediate focus is still on 1.3514 resistance. Decisive break there should at least confirm medium term bottoming at 1.1409. Further rise should be seen to 1.4376 resistance first. Though, rejection by 1.3514 will retain bearishness for resuming the down trend from 2.1161 (2007 high) at a later stage.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PMI Aug | 50.7 | 66.8 | 58.8 | 59 |

| 23:50 | JPY | PPI Y/Y Aug | -0.50% | -0.50% | -0.90% | |

| 23:50 | JPY | BSI Large Manufacturing Conditions Index Q3 | 0.1 | -52.3 | ||

| 6:00 | EUR | Germany CPI M/M Aug F | -0.10% | -0.10% | -0.10% | |

| 6:00 | EUR | Germany CPI Y/Y Aug F | 0.00% | 0.00% | 0.00% | |

| 6:00 | GBP | GDP M/M Jul | 6.60% | 6.70% | 8.70% | |

| 6:00 | GBP | Manufacturing Production M/M Jul | 6.30% | 5.00% | 11.00% | |

| 6:00 | GBP | Manufacturing Production Y/Y Jul | -9.40% | -10.50% | -14.60% | |

| 6:00 | GBP | Industrial Production Y/Y Jul | -7.80% | -8.70% | -12.50% | |

| 6:00 | GBP | Industrial Production M/M Jul | 5.20% | 4.10% | 9.30% | |

| 6:00 | GBP | Index of Services 3M/3M Jul | -8.10% | -19.20% | -19.90% | |

| 6:00 | GBP | Goods Trade Balance (GBP) Jul | -8.6B | -7.4B | -5.1B | -6.6B |

| 12:30 | USD | CPI M/M Aug | 0.30% | 0.60% | ||

| 12:30 | USD | CPI Y/Y Aug | 1.20% | 1.00% | ||

| 12:30 | USD | CPI Core M/M Aug | 0.20% | 0.60% | ||

| 12:30 | USD | CPI Core Y/Y Aug | 1.60% | 1.60% | ||

| 13:00 | GBP | NIESR GDP Estimate | -7.90% | |||

| 14:30 | CAD | Capacity Utilization Q2 | 81.10% | 79.80% |

{kind=link}