Dollar surged with stocks and yield overnight but momentum was unconvincing. Dollar index hit as high as 103.82 but failed to sustain above recent resistance at 103.65. The index is currently trading back at around 103.20. DJIA gained 119.16 pts, or 0.60% to close at 19881.76. However, that close to yesterday’s open at 19872.86 which indicates indecisiveness. S&P 500 performed slightly better as it closed up 19.00 pts, or 0.85% at 2257.83, comparing to the open at 2251.57. 10 year yield jumped to as high as 2.518 but closed at 2.450, sharply below the open at 2.511 even though it ended up 0.004. 30 year yield perform worse, opening at 3.123 but closed at 3.047, down -0.016 from prior close. In the currency market, EUR/USD breached 1.0351 near term support briefly but failed to stay below and is back at 1.0410. Markets are generally staying cautious ahead of employment data from US.

Nonetheless, focus will turn to minutes of December FOMC meeting first. Besides the discussion over the 25 bps rate hike decision made on the month, we are closely watching for the discussion of potential monetary policy changes as Trump takes office. The president-elect has been proposing pro-growth fiscal policy. We would also look for the rationale behind the more hawkish shift in the dot plot which signals 3 rate hikes in 2017. Currently, fed fund futures are pricing in around 70% chance of another rate hike by June this year.

Oil price will be another development to watch. WTI crude oil jumped to 18 month high at 55.24 but reversed since then. It’s currently trading at around 52.50 at the time of writing. WTI was initially lifted by news that Kuwait and Oman indicated that OPEC members are delivering the agreement of production cut. But it reversed as doubt re-surfaced as Libya is seen ramping up output again. The reversal in oil price was seen as a key factor in dragging down stocks yesterday.

On the data front, Eurozone will release PMI services in European session. Also, Eurozone will release December CPI flash. UK will release construction PMI, mortgage approvals and M4 money supply. No key economic data is scheduled for US and focus will be on FOMC minutes.

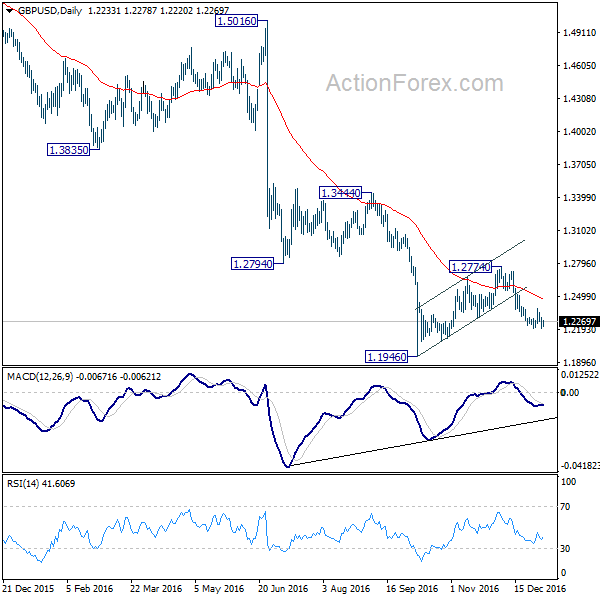

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2187; (P) 1.2247; (R1) 1.2296; More…

GBP/USD recovered ahead of 1.2200 and intraday bias stays neutral. Consolidation there could extend with another rise. But overall outlook is unchanged. That is, corrective rise from 1.1946 has completed at 1.2774. Recovery from 1.2200 should be limited 1.2509 resistance and bring fall resumption. Below 1.2200 will target a test on 1.1946 low. Decisive break there will confirm larger down trend resumption.

In the bigger picture, fall from 1.7190 is seen as part of the down trend from 2.1161. There is no sign of medium term bottoming yet. Sustained trading below 61.8% projection of 2.1161 to 1.3503 from 1.7190 at 1.2457 will target 100% projection at 0.9532. Overall, break of 1.3444 resistance is needed to confirm medium term bottoming. Otherwise, outlook will remain bearish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Consensus | Previous | Revised |

|---|---|---|---|---|---|---|

| 08:45 | EUR | Italy Services PMI Dec | 52.6 | 53.3 | ||

| 08:50 | EUR | France Services PMI Dec F | 52.6 | 52.6 | ||

| 08:55 | EUR | Germany Services PMI Dec F | 53.8 | 53.8 | ||

| 09:00 | EUR | Eurozone Services PMI Dec F | 53.1 | 53.1 | ||

| 09:30 | GBP | Construction PMI Dec | 52.6 | 52.8 | ||

| 09:30 | GBP | Mortgage Approvals Nov | 68.7k | 67.5k | ||

| 09:30 | GBP | M4 Money Supply M/M Nov | 1.40% | 1.10% | ||

| 10:00 | EUR | Eurozone CPI Estimate Y/Y Dec | 1.00% | 0.60% | ||

| 10:00 | EUR | Eurozone CPI – Core Y/Y Dec A | 0.80% | 0.80% | ||

| 19:00 | USD | FOMC Minutes |

Subscribe to our daily and mid-day newsletter to get this report delivered to your mail box