While the US stock extended the near term steep pull back overnight, Asian markets are relatively steady and are just mixed. Major currency pairs and crosses are also stuck in tight range for consolidation. As for the week, Swiss Franc and Yen are the stronger ones on risk off sentiment, on both Omicron and talk of Fed’s quicker tapering. Sterling is currently the worst performing, followed by Aussie. Dollar is mixed as it’s partly weighed down by weakness in treasury yields.

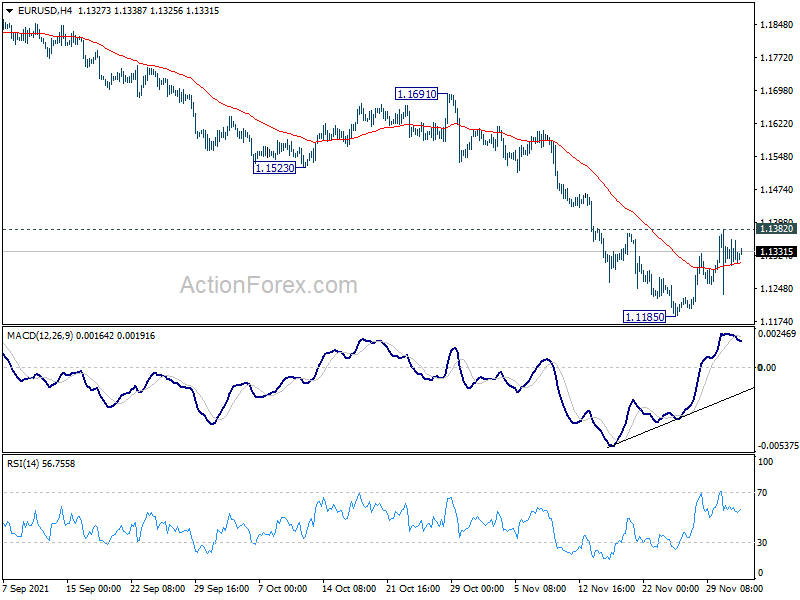

Technically, we’re still looking at breakthroughs in both EUR/USD and USD/JPY. Break of 1.1382 minor resistance in EUR/USD will confirm short term bottoming and bring stronger rebound. On the other hand, firm break of 112.71 support in USD/JPY will extend the correction from 115.51 to 110.57 fibonacci level. Both developments, if happen, will at least confirm near term weakness in the greenback.

In Asia, at the time of writing, Nikkei is down -0.66%. Hong Kong HSI is up 0.39%. China Shanghai SSE is down -0.02%. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield is down -0.0022 at 0.064. Overnight, DOW dropped -1.34%. S&P 500 dropped -1.18%. NASDAQ dropped -1.83%. 10-year yield dropped -0.009 to 1.434.

Fed Williams: To complete tapering earlier is a decisive to grapple with

New York Fed President John Williams said in an FT interview that Omicron “adds a lot of uncertainty to the outlook”. It will “will continue that excess demand in the areas that don’t have capacity, and will stall the recovery in the areas where we actually have the capacity.” That would mean a “somewhat slower rebound overall” and “increase those inflationary pressures, in those areas that are in high demand.”

As for monetary policy, “the question is: Would it make sense to end those purchases somewhat earlier, by maybe a few months, given how strong the economy is?” he said. “That’s a decision, discussion, I expect we’ll have to grapple with.”

Fed Mester very open to consider faster tapering

Cleveland Fed President Loretta Mester told Bloomberg TV, “making the taper faster is definitely buying insurance and optionality so that if inflation doesn’t move back down significantly next year we’re in a position to be able hike if we have to.”

She said that recent data “have come in supportive of that case, so I’m very open to considering a faster pace of tapering.”

“Right now, with the inflation data the way it is and with the job market as strong as it is, I do think that we have to be in a position that if we need to raise rates a couple of times next year we’re able to do that,” said Mester.

BoJ Suzuki: Effective and sustainable monetary easing to persistently continue

BoJ board member Hitoshi Suzuki said in a speech, “to achieve the price stability target of 2 percent, the Bank is expected — even after COVID-19 subsides — to persistently continue with further effective and sustainable monetary easing”.

However, it’s also necessary to “pay attention to the possibility that credit costs will increase due to a delay in economic recovery at home and abroad”. Also, “downward pressure on financial institutions’ core profitability is likely to persist as a trend even after COVID-19 subsides”.

“My view is that the Bank should pay due attention to the fact that side effects of monetary easing will accumulate over time,” he added. “The Bank will continue to conduct monetary policy in an appropriate manner so as to fulfill the two missions of achieving price stability and ensuring the stability of the financial system.”

From Japan too, monetary base rose 9.3% yoy in November, below expectation of 10.3% yoy.

Australia trade surplus narrowed to AUD 11.22B in Oct

Australia exports of goods and services dropped -3% mom to AUD 43.05B in October, driven by falls in iron ore prices. Goods and services imports dropped -3% mom to AUD 31.83B, by fall in imports of capital goods. Trade surplus narrowed to AUD 11.22B, slightly higher than expectation of AUD 11.00B.

Retail sales rose 4.9% mom, 5.9% yoy to AUD 31.13B.

Looking ahead

Swiss retail sales, Eurozone unemployment rate and PPI will be released in European session. US will release jobless claims and Challenger job cuts.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1295; (P) 1.1327; (R1) 1.1352; More…

Intraday bias in EUR/USD remains neutral for the moment and outlook is unchanged. On the upside, firm break of 1.1382 resistance should confirm short term bottoming at 1.1186. Intraday bias will be turned back to the upside for 55 day EMA (now at 1.1509). On the downside, break of 1.1185 will resume larger fall from 1.2348.

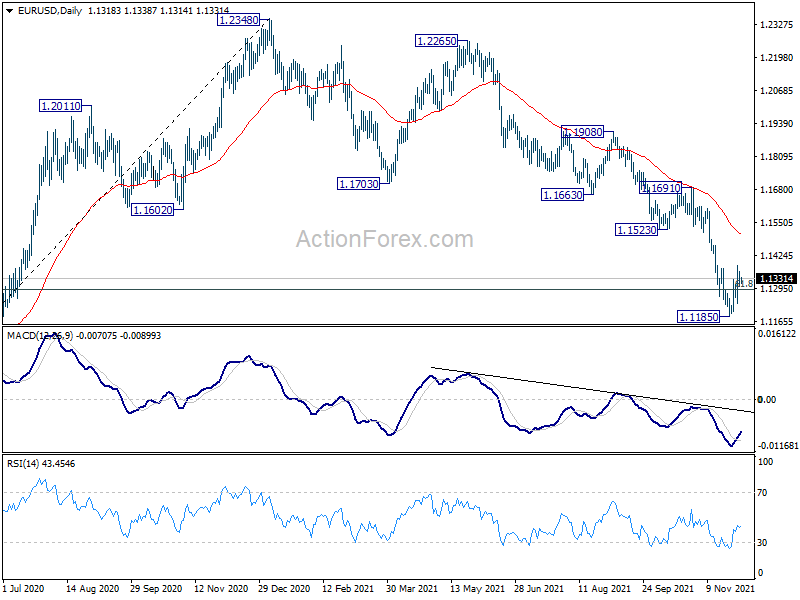

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 would pave the way back to 1.0635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Terms of Trade Index Q3 | 0.70% | 2.10% | 3.30% | 3.20% |

| 23:50 | JPY | Monetary Base Y/Y Nov | 9.30% | 10.30% | 9.90% | |

| 0:30 | AUD | Trade Balance (AUD) Oct | 11.22B | 11.00B | 12.24B | 11.82B |

| 5:00 | JPY | Consumer Confidence Nov | 40.3 | 39.2 | ||

| 7:30 | CHF | Real Retail Sales Y/Y Oct | 2.20% | 2.50% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Oct | 7.30% | 7.40% | ||

| 10:00 | EUR | Eurozone PPI M/M Oct | 3.20% | 2.70% | ||

| 10:00 | EUR | Eurozone PPI Y/Y Oct | 19% | 16% | ||

| 12:30 | USD | Challenger Job Cuts Nov | 22.822K | |||

| 13:30 | USD | Initial Jobless Claims (Nov 26) | 250K | 199K | ||

| 15:30 | USD | Natural Gas Storage | -21B |

{kind=link}