Canadian Dollar rises strongly entering into US session, as boosted by much stronger than expected job data. On the other hand, Dollar is struggling to react to mixed non-farm payroll data. As for today, the Loonie is the strongest one, followed by Swiss Franc and Euro. Aussie and Kiwi are so far the worst. But, the picture may change before weekly close.

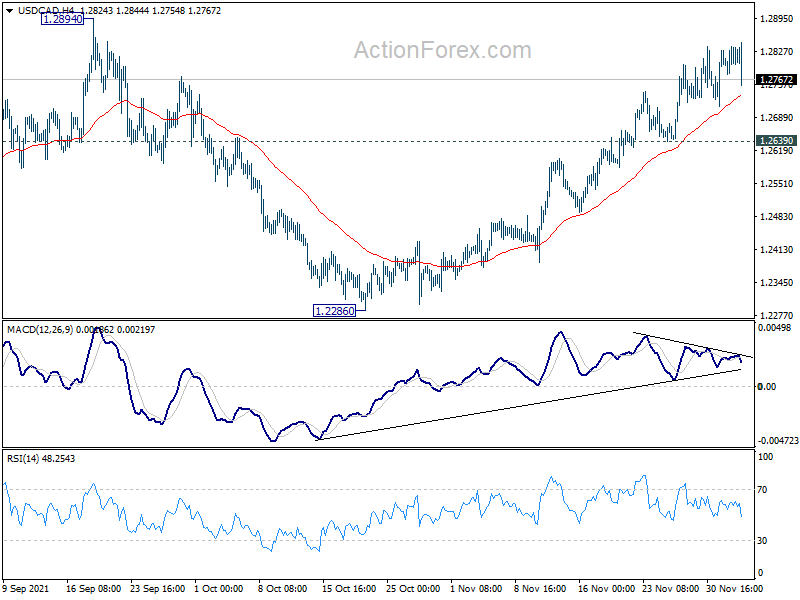

Technically, while USD/CAD retreats, further rise will remain in favor as long as 1.2639 support holds. At the same time, AUD/USD resumes near term down trend by breaking through 0.7061 support. We’ll see if there is any pre-weekend wild moves in the stock markets to drive further moves in commodity currencies.

In Europe, at the time of writing, FTSE is up 0.43%. DAX is up 0.44%. CAC is up 0.45%. Germany 10-year yield is flat at -0.368. Earlier in Asia, Nikkei rose 1.00%. Hong Kong HSI dropped -0.09%. China Shanghai SSE rose 0.94%. Singapore Strait Times rose 0.32%. Japan 10-year JGB yield dropped -0.0023 to 0.057.

US NFP grew only 210k, but unemployment rate dropped to 4.2%

US non-farm payroll employment grew only 210k in November, well below expectation of 525k. So far this year, monthly job growth has averaged 555k. Overall employment remained down by -3.9m, or -2.6%, from its pre pandemic level in February 2020.

Unemployment rate dropped sharply by -0.4% to 4.2%, better than expectation of 4.5%. Labor force participation rate edged up to 61.8%. Average hourly earnings rose 0.3% mom, below expectation of 0.4% mom.

Canada employment rose 154k in Nov, unemployment rate dropped to 6.0%

Canada employment grew 154k in November, well above expectation of 37k. It’s now 1% higher than its pre-COVID February 2020 level. Unemployment rate dropped sharply from 6.7% to 6.0%, much better than expectation of 6.6%.

Full time jobs grew 80k while part-time jobs rose 74k. Services-producing sector added 127k jobs, while goods-producing sectors rose 26k. Total hours worked rose 0.7% mom.

ECB Lagarde: Inflation will decline in 2022

ECB President Christine Lagarde said in a conference, “We are firmly of the view, and I’m confident, that inflation will decline in 2022.” She described the inflation profile as a “hump”, and while it’s now at a high level of the hump for Eurozone, ” a hump eventually declines.”

Lagarde also said that energy prices will have declined significantly by the end of 2022. But supply bottlenecks will take until mid-2022 or end 2022 to end.

Separately, Governing Council member Klaas Knot said the central bank could decide to raise interest rates by 2023 if inflation continues to exceed expectations next year.

Eurozone retail sales rose 0.2% mom in Oct, EU up 0.3% mom

Eurozone retail sales rose 0.2% mom in October, below expectation of 0.3% mom. Volume of retail trade increased by 1.3% for automotive fuels and by 0.4% non-food products, while it fell for food, drinks and tobacco by 0.1%.

EU retail sales rose 0.3% mom. Among Member States for which data are available, the highest monthly increases in the total retail trade volume were registered in Slovenia (+13.0%), Portugal (+2.3%) and Denmark (+2.2%). The largest decreases were observed in Latvia (-5.4%), Austria (-2.8%) and Estonia (-2.6%).

Eurozone PMI composite finalized at 55.4, downside growth risk, upside inflation risk

Eurozone PMI Services was finalized at 55.9 in November, up from October;s 54.6. PMI Composite was finalized at 55.4, up from October’s 54.2. Looking at some member states, Ireland PMI composite dropped to 7-month low at 59.3. Spain rose to 3-month high at 58.3. Italy rose to 3-month high at 57.6. France rose to 4-month high at 56.1. Germany rose to 2-month high at 52.2.

Chris Williamson, Chief Business Economist at IHS Markit said:

“An improvement in the rate of economic growth signalled by the eurozone PMI looks likely to be short-lived. Not only did demand growth weaken, but firms’ expectations of future growth also sank lower as worries about the pandemic intensified again. With the data collected prior to news of the Omicron variant, sentiment about near-term prospects will inevitably have been knocked even further….

“While growth risks have shifted to the downside, risks to the inflation outlook seem tiled to the upside if virus case numbers continue to rise and new restrictions are introduced. Supply chains will be further hit, staff availability will deteriorate and spending could shift from services to goods again, further exacerbating the imbalance of supply and demand.”

Germany PMI Services was finalized to 52.7 in November, up from October’s 52.4. PMI Composite was finalized at 52.2, up slightly from October’s 52.0. Markit said new business fell as fourth COVID wave took hold. Firms’ expectation slipped to 12-month low. Rate of input cost and output price accelerated to new highs.

France PMI Services was finalized at 57.4 in November, up from 56.6 in October, signalling the strongest growth since June. PMI Composite was finalized at 56.1, up from October’s 54.7. Markit said strong jobs growth sustained as business activity continued to grow. Firms reported still-strong demand pressures. output prices rose at fastest rate since June 2011.

BoE hawk Saunders: Omicron a key considering for December meeting

BoE MPC member Michael Saunders, a known hawk, said in a speech that “policy is not on auto pilot”. He added. “the pace, and scale, of any monetary policy changes will depend on economic developments and the outlook”.

“In particular, at the December meeting, a key consideration for me will be the possible economic effects of the new Omicron Covid variant, and the potential costs and benefits of waiting to see more data on this before – if necessary – adjusting policy,” he said.

“It is likely that any rise in Bank Rate will be limited given that the neutral level of interest rates remains low. Provided we do not delay too long, it should be a case of easing off the accelerator rather than applying the brakes,” he noted.

UK PMI services finalized at 58.5, recovery accelerated from Q3

UK PMI Services was finalized at 58.5 in November, down from October’s 59.1. PMI Composite was finalized at 57.6, down from October’s 57.8. Markit also said there was the strongest increase in new work since June. Output growth eased slightly. Input costs and prices charged rose at record rates.

Tim Moore, Economics Director at IHS Markit:

“Surging price pressures have done little to dent business and consumer spending across the UK economy… The overall speed of recovery looks to have accelerated in comparison to the third quarter of 2021, with output growth mostly driven by services as manufacturers struggle with severe shortages of raw materials and critical components.

“The vast majority of survey responses in November were received prior to the news of the Omicron variant, however, which has the potential to derail near-term growth prospects and add to international supply chain disruption.

China Caixin PMI composite dropped to 51.2, inflationary pressure remained

China Caixin PMI Services dropped from 53.8 to 52.1 in November, above expectation of 51.2. PMI Composite dropped from 51.5 to 51.2.

Wang Zhe, Senior Economist at Caixin Insight Group said: “Overall, conditions in the manufacturing sector remained stable in November, while for the service sector, expansion occurred at a slightly slower pace. The downward pressure to the economy grew, and inflationary pressure was partly eased….

“The government’s measures to stabilize commodity supplies and prices significantly eased cost pressures on manufacturing enterprises, but had a limited impact on the reduction of costs to service enterprises. Overall, inflationary pressure remained.”

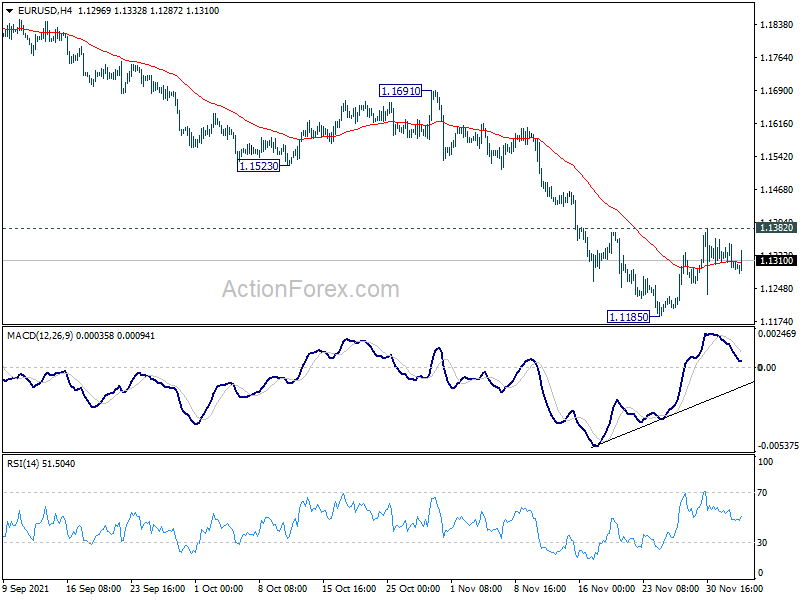

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1281; (P) 1.1314; (R1) 1.1334; More…

Range trading continues in EUR/USD and intraday bias remains neutral first. On the upside, firm break of 1.1382 resistance should confirm short term bottoming at 1.1186. Intraday bias will be turned back to the upside for 55 day EMA (now at 1.1495). On the downside, break of 1.1185 will resume larger fall from 1.2348.

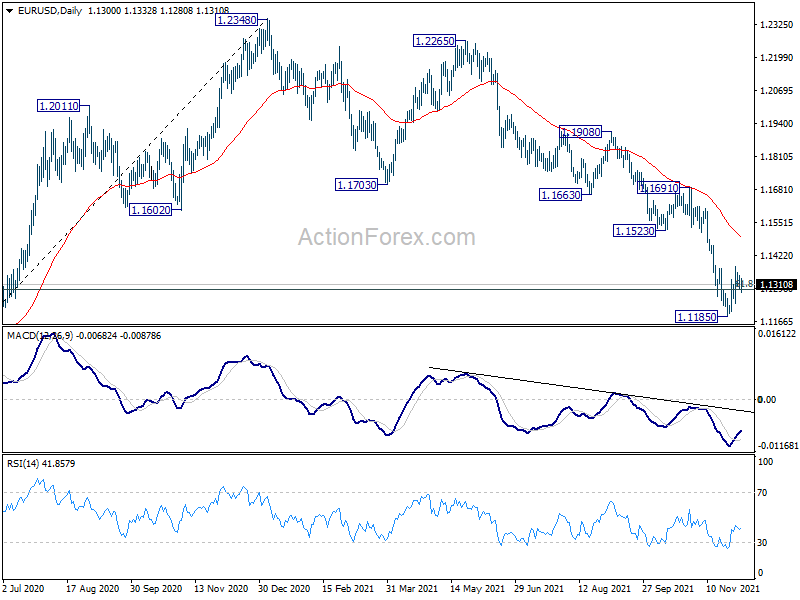

In the bigger picture, there are various ways of interpreting the fall from 1.2348 (2021 high). It could be a correction to rise from 1.0635 (2020 low), the fourth leg of a sideway pattern from 1.0339 (2017 low), or resuming long term down trend. In any case, outlook will now stay bearish as long as 1.1703 support turned resistance holds. Sustained break of 61.8% retracement of 1.0635 to 1.2348 at 1.1289 would pave the way back to 1.0635.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | AUD | AiG Performance of Construction Index Nov | 57 | 57.6 | ||

| 01:45 | CNY | Caixin Services PMI Nov | 52.1 | 51.2 | 53.8 | |

| 07:45 | EUR | France Industrial Output M/M Oct | 0.90% | 0.40% | -1.30% | -1.50% |

| 08:45 | EUR | Italy Services PMI Nov | 55.9 | 54.5 | 52.4 | |

| 08:45 | EUR | France Services PMI Nov F | 57.4 | 58.2 | 58.2 | |

| 08:55 | EUR | Germany Services PMI Nov F | 52.7 | 53.4 | 53.4 | |

| 09:00 | EUR | Eurozone Services PMI Nov F | 55.9 | 56.6 | 56.6 | |

| 09:30 | GBP | Services PMI Nov F | 58.5 | 58.6 | 58.6 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Oct | 0.20% | 0.30% | -0.30% | |

| 13:30 | CAD | Net Change in Employment Nov | 153.7K | 36.5K | 31.2K | |

| 13:30 | CAD | Unemployment Rate Nov | 6.00% | 6.60% | 6.70% | |

| 13:30 | CAD | Labor Productivity Q/Q Q3 | -1.50% | -0.70% | 0.60% | 0.00% |

| 13:30 | USD | Nonfarm Payrolls Nov | 210K | 525K | 531K | 546K |

| 13:30 | USD | Unemployment Rate Nov | 4.20% | 4.50% | 4.60% | |

| 13:30 | USD | Average Hourly Earnings M/M Nov | 0.30% | 0.40% | 0.40% | |

| 14:45 | USD | Services PMI Nov F | 57 | 57 | ||

| 15:00 | USD | ISM Services PMI Nov | 65.5 | 66.7 | ||

| 15:00 | USD | ISM Services Employment Index Nov | 51.6 | |||

| 15:00 | USD | Factory Orders M/M Oct | 0.50% | 0.20% |

{kind=link}