Dollar and Sterling firm up mildly in overall quiet markets today. Commodity currencies are, on the other hand, trading lower. Investors are turning cautious ahead of the wave of central bank meetings later this week, in particular on Fed’s decision to faster the tapering pace. Oil prices also dip mildly even though OPEC upgraded demand forecasts and maintained an upbeat tone. Gold is mildly higher together with Silver.

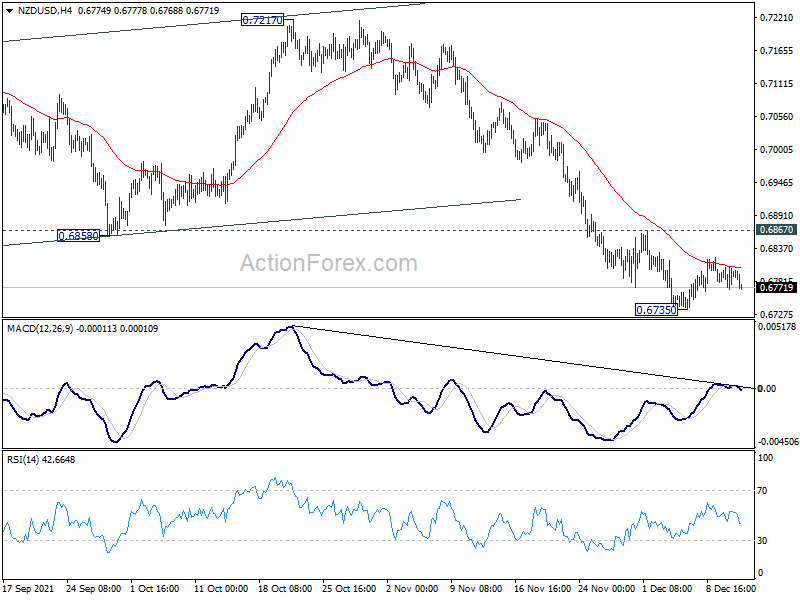

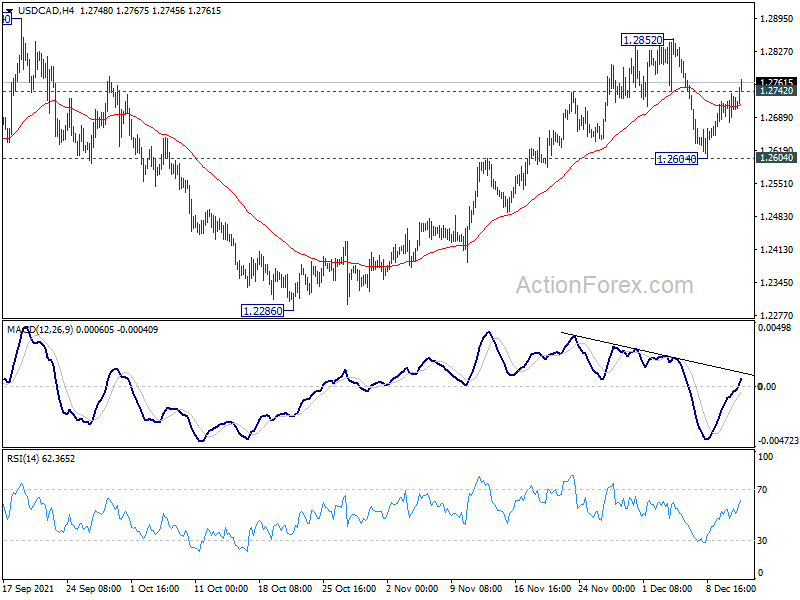

Technically, USD/CAD’s break of 1.2742 minor resistance suggests that pull back from 1.2852 has completed and rise from 1.2286 is ready to resume. We’ll also pay attention to NZD/USD and break of 0.6735 temporary low will resume the fall from 0.7217, as part of the larger pattern from 0.7463.

In Europe, at the time of writing, FTSE is down -0.18%. DAX is up 0.87%. CAC is up 0.10%. Germany 10-year yield is down -0.0089 at -0.354. Earlier in Asia, Nikkei rose 0.71%. Hong Kong HSI dropped -0.17%. China Shanghai SSE rose 0.40%. Singapore Strait Times dropped -0.50%. Japan 10-year JGB yield dropped -0.0061 to 0.050.

OPEC: Impact of Omicron to be mild and short-lived

In the December Monthly Oil Market Report, OPEC said the impact of Omicron is projected to be “:mild and short-lived, as the world becomes better equipped to manage COVID-19 and its related challenges.”

“Some of the recovery previously expected in the fourth quarter of 2021 has been shifted to the first quarter of 2022, followed by a more steady recovery throughout the second half of 2022,” OPEC said.

OPEC expects oil demand to average 99.13m bpd in Q2 of 2022, up 1.11m bpd from its forecast last month.

Germany wholesale price rose at record 16.6% yoy in Nov

Germany wholesale price index rose 1.3% mom, 16.6% yoy in November. The annual rate was the highest since record began back in 1962.

Destatis said: “The high rates of change for wholesale prices in annual comparison derive from increased prices for raw materials and intermediate products. The largest impact on the year-on-year price rate in wholesale trade had the increased prices for mineral oil products (+62.4%).”

Japan Tankan large manufacturing index unchanged a 18, outlook ticked down

According to the BoJ’s Tankan survey in Q4, large manufacturing index was unchanged at 18, below expectation of 19. Large manufacturing outlook dropped from 14 to 13, below expectation of 19.

Non-manufacturing index rose sharply from 2 to 9, well above expectation of 6. That’s the highest reading since December 2019. Non-manufacturing outlook also rose from 3 to 8, but missed expectation of 10.

Output price index for large enterprises jumped from 10 to 16, highest since the 1980s. Input prices index also rose from .37 to 49, highest since 2008.

Large firms are expecting to increased capital spending by 9.3% in the year ending in March 2022, lower than expectation of 9.8%.

Also released, machine orders rose 3.8% mom in October, above expectation of 2.1% mom. That’s the first rise in three months.

NZIER: NZ inflation to stay above RBNZ target mid-point through to 2025

NZIER lowered near-term economic outlook of New Zealand, reflecting the impact of pandemic restrictions, “which turned out to persist for longer than initially expected”. For the year to March 2022, GDP growth was revised down from 4.5% to 4.3%. But growth for 2023 was revised up from 4.5% to 4.6%.

Growing capacity pressures are contributing to a sharp rise in inflation. CPI is expected to 5.1% in 2022 (up from prior estimate of 3.0%), and remain elevated above RBNZ’s inflation target mid-point of 2% “through to 2025”.

NZD trade-weighted index forecast was revised lower “partly reflecting market disappointment at smaller than expected interest rate increased from the Reserve Bank in its November meeting.” NZD TWI is expected to peak at 74.5 for the year to March 2023 (revised down from 74.8), then ease to 72.7 in 2025.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2691; (P) 1.2714; (R1) 1.2749; More…

USD/CAD’s break of 1.2742 minor resistance suggests that pull back from 1.2852 has completed at 1.2604 already. Rise from 1.2286 might be ready to resume. Intraday bias is turned back to the upside for 1.2852 first. Break will confirm this case and target 1.2947 resistance. On the downside, however, firm break of 1.2604 will argue that rise from 1.2286 has completed. Deeper fall would be seen back to 1.2286 support.

In the bigger picture, medium term outlook remains neutral for now. The pair drew support from 1.2061 cluster and rebounded. Yet, upside was limited below 38.2% retracement of 1.4667 to 1.2005 at 1.3022. On the upside, firm break of 1.3022 should affirm the case of medium term bullish reversal. However, break of 1.2286 will turn focus back to 1.2005 low again.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q4 | 18 | 19 | 18 | |

| 23:50 | JPY | Tankan Non-Manufacturing Index Q4 | 9 | 6 | 2 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q4 | 13 | 19 | 14 | |

| 23:50 | JPY | Tankan Non – Manufacturing Outlook Q4 | 8 | 10 | 3 | |

| 23:50 | JPY | Tankan Large All Industry Capex Q4 | 9.30% | 9.80% | 10.10% | |

| 23:50 | JPY | Machinery Orders M/M Oct | 3.80% | 2.10% | 0.00% | |

| 17:00 | GBP | Financial Stability Report |

{kind=link}