Yen rebounds notably as US futures take a dive just ahead of North American session, while European index also reverse earlier gains. While Dollar is dragged down by Yen, it’s somewhat still resilient against others. Selling is mainly seen in Swiss Franc and, to a lesser extent, Euro. Commodity currencies are mixed. We’ll have to see how the overall risk sentiment plays out. Yet, more volatility is anticipated ahead with Fed chair Jerome Powell’s testimony, and US inflation data featured later in the week.

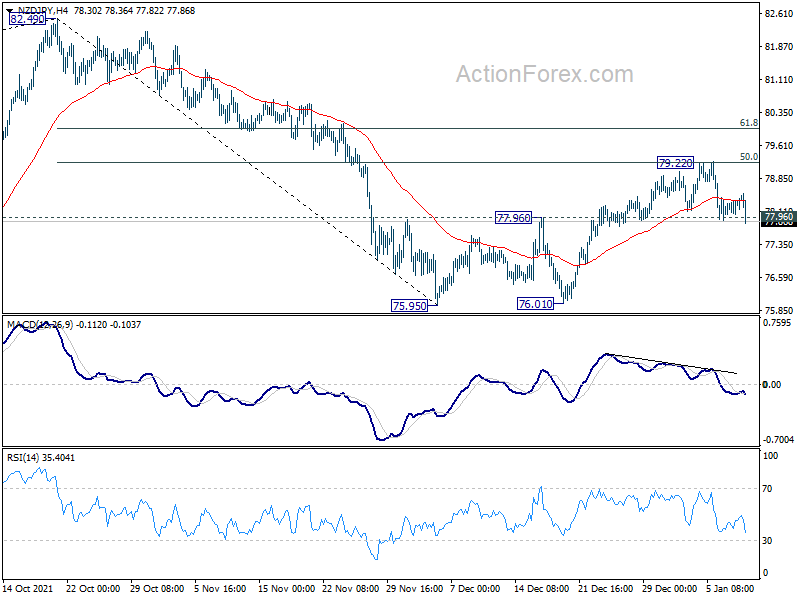

Technically, it’s too early to claim that Yen is reversing. But we’ll keep an eye on some commodity Yen crosses. NZD/JPY’s break of 77.96 resistance turned support argues that corrective pattern from 75.95 has completed with three waves up to 79.22. Deeper fall would be seen back to retest 75.95/76.01 zone.

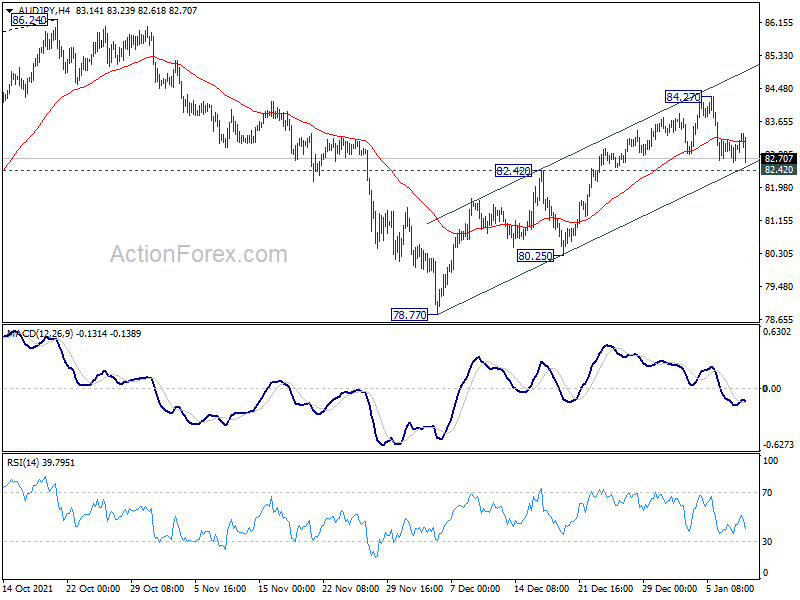

We’ll also keep on eye on 82.42 resistance turned support in AUD/JPY. Break there will argue that the rebound from 78.77 is over, and bring deeper fall back to 80.25 support and possibly below.

In Europe, at the time of writing, FTSE is down -0.29%. DAX is down -0.65%. CAC is down -0.74%. Germany 10-year yield is down -0.0087 at -0.048. Earlier in Asia, Hong Kong HSI rose 1.08%. China Shanghai SSE rose 0.39%. Singapore Strait Times rose 0.68%. Japan was on holiday.

Eurozone Sentix rose to 14.9 in Jan, fundamentally constructive outlook with an Achilles’ heel

Eurozone Sentix Investor Confidence rose from 13.5 to 14.9 in January, above expectation of 12.0. Current Situation Index rose from 13.3 to 16.3. Expectations Index dropped slightly from 13.8 to 13.5.

Sentix said, “our fundamentally constructive outlook for the economy in 2022 (especially the first half of the year) has an Achilles’ heel: The support of expansive central banks is threatening to run out faster than expected.

“The sentix topic barometer ‘Central Bank Policy’ indicates an increasing burden for the bond market and thus for the real economy. The burden on this is estimated to be greater than in 2018, when the monetary guardians also adopted a more restrictive course.

“Fiscal balancing impulses must therefore be put in place swiftly to cushion the weakening monetary impetus from the central banks.”

Eurozone unemployment rate dropped to 7.2% in Nov, EU down to 6.5%

Eurozone unemployment rate dropped from 7.3% to 7.2% in November, matched expectations. EU unemployment rate dropped from 6.7% to 6.5%.

Eurostat estimates that 13.984 million men and women in the EU, of whom 11.829 million in the euro area, were unemployed in November 2021. Compared with October 2021, the number of persons unemployed decreased by 247 000 in the EU and by 222 000 in the euro area. Compared with November 2020, unemployment decreased by 1.659 million in the EU and by 1.411 million in the euro area.

IMF Blog: Faster Fed hike could rattle financial markets

In an blog post, senior IMF officials said the continued to expect “robust US growth”. Inflation will “likely moderate” late this year as supply disruptions ease and fiscal contraction weighs on demand. Fed’s indication that it would raise interest rate more quickly “did not cause a substantial market reassessment of the economic outlook”.

“Should policy rates rise and inflation moderate as expected, history shows that the effects for emerging markets are likely benign if tightening is gradual, well telegraphed, and in response to a strengthening recovery,” the post noted.

However, “broad-based US wage inflation or sustained supply bottlenecks could boost prices more than anticipated and fuel expectations for more rapid inflation”.

“Faster Fed rate increases in response could rattle financial markets and tighten financial conditions globally. These developments could come with a slowing of US demand and trade and may lead to capital outflows and currency depreciation in emerging markets.”

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 115.39; (P) 115.71; (R1) 115.89; More…

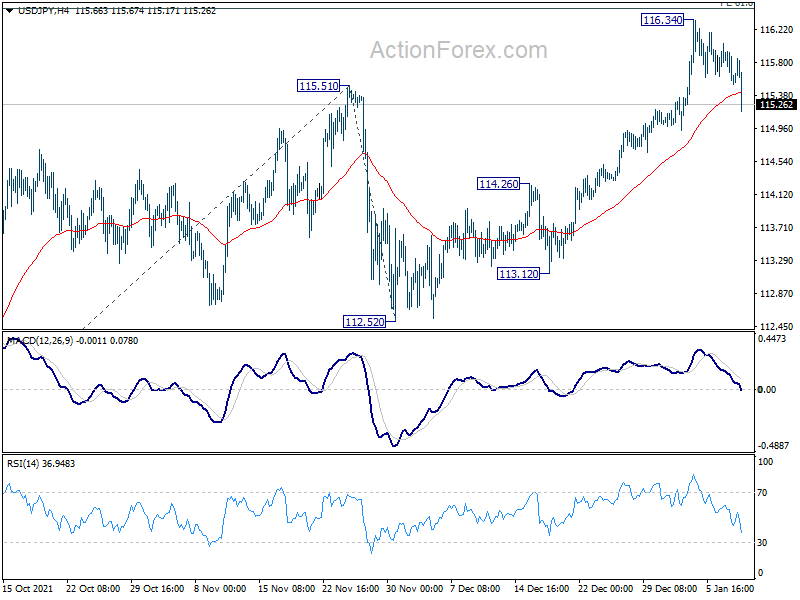

USD/JPY’s pull back from 116.34 extends lower today but outlook is unchanged. Downside of retreat should be contained well well above 114.26 resistance turned support to bring rally resumption. On the upside, firm break of 61.8% projection of 109.11 to 115.51 from 112.52 at 116.47 will pave the way to 100% projection at 118.90, which is close to 118.65 long term resistance.

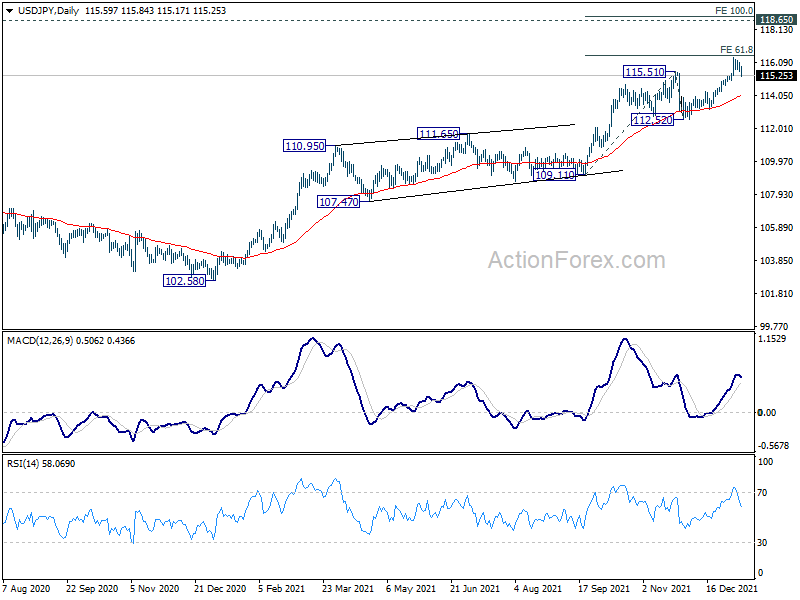

In the bigger picture, no change in the view that rise from 102.58 is the third leg of the up trend from 101.18 (2020 low). Such rally should target a test on 118.65 (2016 high). Sustained break there will pave the way to 120.85 (2015 high) and raise the chance of long term up trend resumption. For now, this will remain the favored case as long as 112.52 support holds, in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:00 | AUD | TD Securities Inflation M/M Dec | 0.20% | 0.30% | ||

| 00:30 | AUD | Building Permits M/M Nov | 3.60% | 3.20% | -12.90% | |

| 09:30 | EUR | Eurozone Sentix Investor Confidence Jan | 12 | 13.5 | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 7.20% | 7.30% | ||

| 15:00 | USD | Wholesale Inventories Nov F | 1.20% | 1.20% |

{kind=link}