Dollar is staying largely in range after mixed retail sales data from the US. Today’s focus turns to selloff in Sterling, in particular against Swiss Franc and Euro. Yen weakens mildly after yesterday’s rebound quickly lost momentum. Commodity currencies are trading on the soft side. In other markets, major European indexes are mixed while US futures are nearly flat. Gold is back pressing key support level at around 1680. WTI crude oil is range bound.

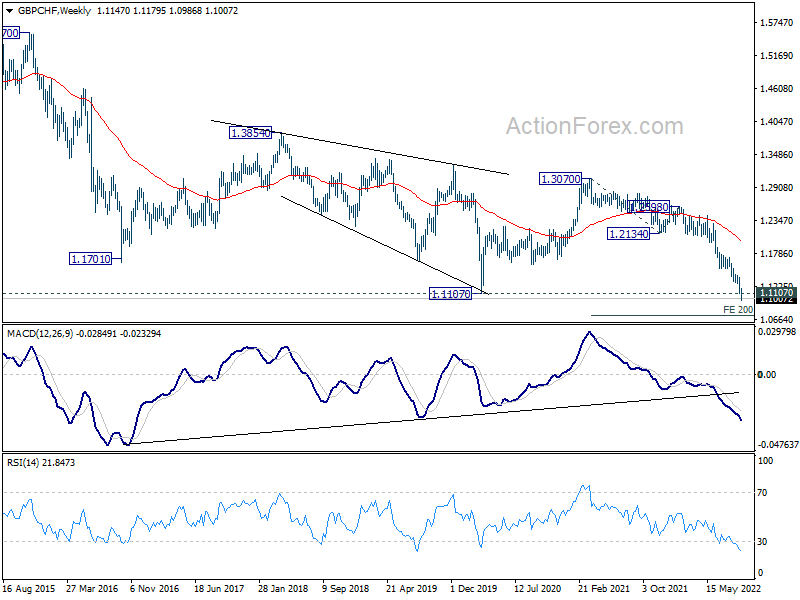

Technically, GBP/CHF break through pandemic low at 1.1107 this week and it’s accelerating slightly. Next target is 200% projection of 1.3070 to 1.2134 from 1.2598 at 1.0726. The question is whether EUR/CHF would accelerate downward below 0.9550 low as down trend resumes. Or, EUR/GBP would finally break through 0.8721 resistance will strength to resume the rally from 0.8201.

In Europe, at the time of writing, FTSE is up 0.30%. DAX is down -0.17%. CAC is down -0.64%. Germany 10-year yield is down -0.007 at 1.709. Earlier in Asia, Nikkei rose 0.21%. Hong Kong HSI rose 0.44%. China Shanghai SSE dropped -1.16%. Singapore Strait Times rose 0.31%. Japan 10-year JGB yield dropped -0.0008 to 0.257.

US retail sales rose 0.3% mom in Aug, ex-auto sales down -0.3% mom

US retail sales rose 0.3% mom to USD 683.3B in August, above expectation of 0.0% mom. Ex-auto sales dropped -0.3% mom, below expectation of 0.0% mom. Ex-gasoline sales rose 0.8% mom. Ex-auto, ex-gasoline sales rose 0.3% mom.

Comparing with a year ago, total sales rose 9.1% yoy. Total sales for June through August were up 9.3% from the same period a year ago.

US initial jobless claims dropped to 213k

US initial jobless claims dropped -5k to 213k in the week ending September 10, below expectation of 227k. Four-week moving average of initial claims dropped -8k to 224k. Continuing claims rose 2k to 1403k in the week ending September 3. Four-week moving average of continuing claims dropped -7.75k to 1413k.

Also released, import price index dropped -1.0% mom in August. Empire State manufacturing index improved from -31.3 to -1.5. Philly Fed survey dropped from 6.2 to -9.9.

ECB de Guindos: Determined action essential to keep inflation expectations anchored

ECB Vice-President Luis de Guindos said in a speech, “monetary policy needs to be focused on price stability and on delivering our inflation target over the medium term. Determined action is essential to keep inflation expectations anchored, which in itself contributes to delivering price stability and avoids second-round effects in inflation. The main asset that central banks have is credibility, and this asset becomes even more important in times of high uncertainty.”

On the economy, de Guindos said, “A period of heightened uncertainty is here to stay for a while, rendering decision-making more complex. Output growth is slowing down substantially and is expected to stagnate around year-end and remain low next year at less than 1%, while risks have intensified on the downside. This is set against a deteriorating inflation outlook with record-high inflation rates expected to stay elevated, well above our target, with risks primarily on the upside.”

Eurozone exports rose 13.3% yoy in Jul, imports surged 44.0% yoy

Eurozone exports of goods rose 13.3% yoy to EUR 235.5B in July. Imports rose 44.0% yoy to EUR 269.5B. Trade deficit with the rest of the world came in at EUR -34B. Intra-Eurozone trade rose 24.0% yoy to EUR 224.8B.

In seasonally adjusted term, Eurozone exports dropped -1.7% mom to EUR 236.7B. Imports rose 1.5% mom to EUR 277.0B. Trade deficit widened to EUR -40.3B, larger than expectation of EUR -32.5B. Intra-Eurozone trade rose from EUR 225.1B to EUR 229.3B.

Japan reports record monthly trade deficit, on record increase in imports

Japan exports rose 22.1% yoy to JPY 8062B in August, driven by shipments of auto and chip-related equipment. Imports rose 49.9% yoy to JPY 10879B. That’s the largest increase by value on record, since data became available back in 1979. The rise was driven by higher prices for energy including crude oil, coal, and LNG.

Trade deficit came in at JPY -2817B. That’s the largest monthly trade deficit on record. That’s also the 13th straight month of year-on-year trade shortfalls.

In seasonally adjusted term, exports dropped -0.7% mom to JPY 8379B. Imports rose 1.5% to JPY 10750B. Trade deficit came in at JPY -2371B.

Australia employment rose 33.5k in Aug, unemployment rate ticked up to 3.5%

Australia employment rose 33.5k in August, slightly smaller than expectation of 35.5k. Full-time jobs rose 58.8k while part-time jobs decreased -25.3k.

Unemployment rate ticked up from 3.4% to 3.5%, above expectation of 3.4%. Participation rate rose 0.2% from 66.4% to 66.6%. Monthly hours worked rose 0.8% mom.

New Zealand GDP grew 1.7% qoq in Q2, driven by services

New Zealand GDP grew 1.7% qoq in Q2, above expectation of 1.0% qoq, following a -0.2% qoq decline in Q1. Service industries rose 2.7% but goods producing industries dropped -3.8%. Primary industries rose 0.2%.

“The reopening of borders, easing of both domestic and international travel restrictions, and fewer domestic restrictions under the Orange traffic light setting supported growth in industries that had been most affected by the COVID-19 response measures,” national accounts – industry and production senior manager Ruvani Ratnayake said.

“In the June 2022 quarter, households and international visitors spent more on transport, accommodation, eating out, and sports and recreational activities.”

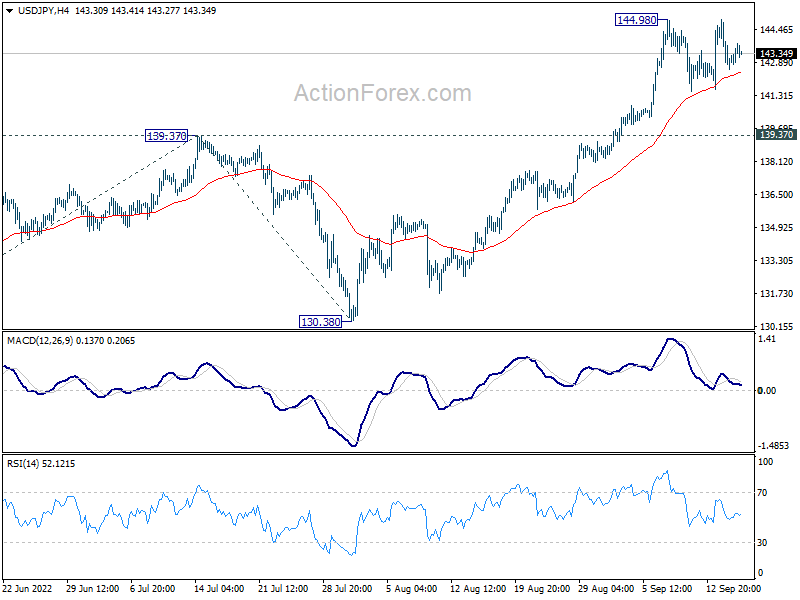

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.17; (P) 143.56; (R1) 144.57; More…

Range trading continues in USD/JPY and intraday bias stays neutral first. While deeper retreat cannot be ruled out, downside should be contained by 139.37 resistance turned support. On the upside, break of 144.98 will resume larger up trend to 147.68 long term resistance. Break there will target 161.8% projection of 126.35 to 139.37 from 130.38 at 151.44 next.

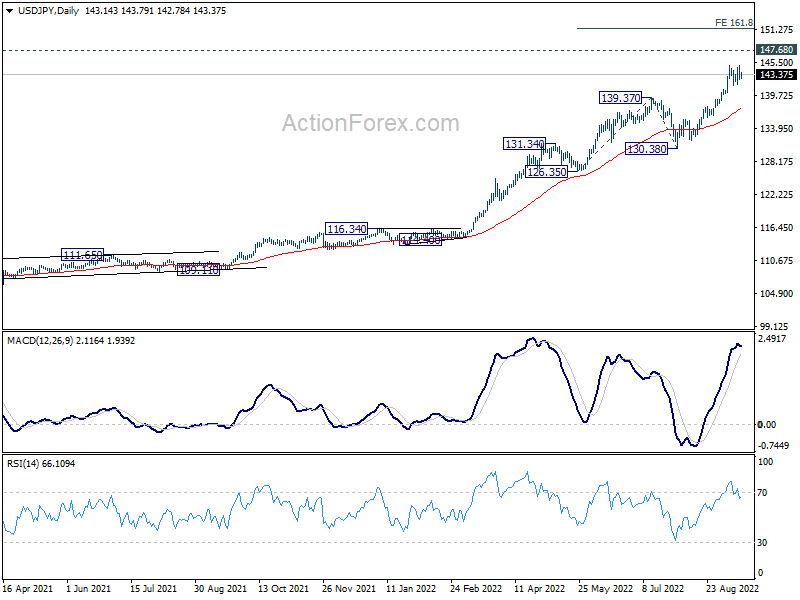

In the bigger picture, up trend from 101.18 is still in progress, as part of the whole up trend from 75.56 (2011 low). Further rise should be seen to 147.68 (1998 high). For now, break of 130.38 support is needed to be the first indication of medium term topping. Otherwise, outlook will stay bullish even in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | GDP Q/Q Q2 | 1.70% | 1.00% | -0.20% | |

| 23:50 | JPY | Trade Balance (JPY) Aug | -2.37T | -2.08T | -2.13T | -2.16T |

| 01:00 | AUD | Consumer Inflation Expectations Sep | 5.40% | 5.90% | ||

| 01:30 | AUD | Employment Change Aug | 33.5K | 35.5K | -40.9K | |

| 01:30 | AUD | Unemployment Rate Aug | 3.50% | 3.40% | 3.40% | |

| 04:30 | JPY | Tertiary Industry Index M/M Jul | -0.60% | -0.10% | -0.20% | |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jul | -32.5B | -30.8B | ||

| 12:30 | USD | Initial Jobless Claims (Sep 9) | 227K | 222K | ||

| 12:30 | USD | Retail Sales M/M Aug | 0.00% | 0.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 0.00% | 0.40% | ||

| 12:30 | USD | Import Price Index M/M Aug | -1.20% | -1.40% | ||

| 12:30 | USD | Empire State Manufacturing Index Sep | -15.25 | -31.3 | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Survey Sep | 2.5 | 6.2 | ||

| 13:15 | USD | Industrial Production M/M Aug | 0.20% | 0.60% | ||

| 14:00 | USD | Business Inventories Jul | 0.80% | 1.40% | ||

| 14:30 | USD | Natural Gas Storage | 71B | 54B |

{kind=link}